Advertisement

- Spain

- /

- Electric Utilities

- /

- BME:RED

Is Red Eléctrica Corporación, S.A.'s (BME:REE) High P/E Ratio A Problem For Investors?

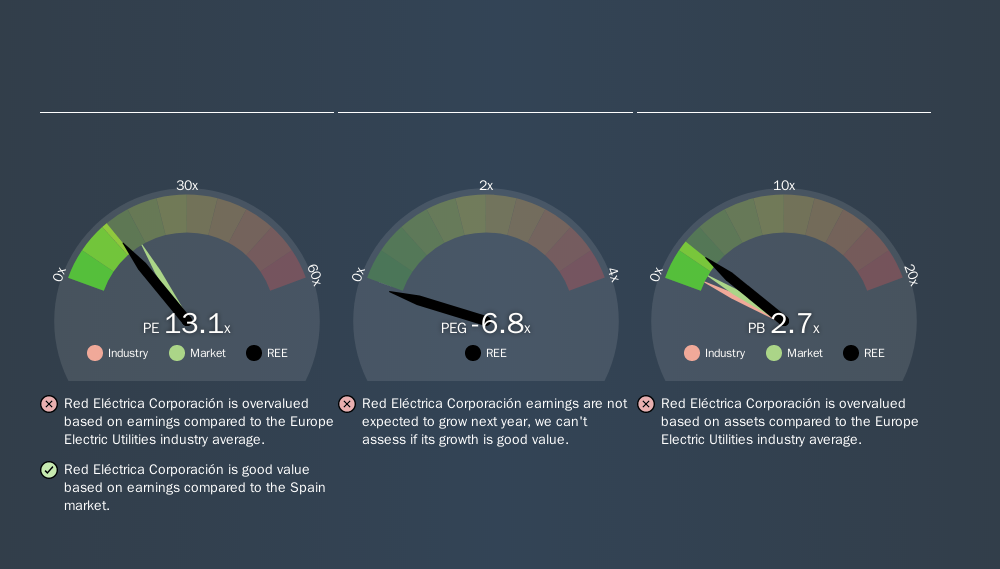

The goal of this article is to teach you how to use price to earnings ratios (P/E ratios). We'll look at Red Eléctrica Corporación, S.A.'s (BME:REE) P/E ratio and reflect on what it tells us about the company's share price. Red Eléctrica Corporación has a P/E ratio of 13.13, based on the last twelve months. That corresponds to an earnings yield of approximately 7.6%.

Check out our latest analysis for Red Eléctrica Corporación

How Do You Calculate A P/E Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for Red Eléctrica Corporación:

P/E of 13.13 = €17.34 ÷ €1.32 (Based on the trailing twelve months to September 2019.)

Is A High Price-to-Earnings Ratio Good?

The higher the P/E ratio, the higher the price tag of a business, relative to its trailing earnings. That isn't necessarily good or bad, but a high P/E implies relatively high expectations of what a company can achieve in the future.

Does Red Eléctrica Corporación Have A Relatively High Or Low P/E For Its Industry?

One good way to get a quick read on what market participants expect of a company is to look at its P/E ratio. The image below shows that Red Eléctrica Corporación has a P/E ratio that is roughly in line with the electric utilities industry average (13.1).

Red Eléctrica Corporación's P/E tells us that market participants think its prospects are roughly in line with its industry.

How Growth Rates Impact P/E Ratios

Generally speaking the rate of earnings growth has a profound impact on a company's P/E multiple. If earnings are growing quickly, then the 'E' in the equation will increase faster than it would otherwise. That means even if the current P/E is high, it will reduce over time if the share price stays flat. A lower P/E should indicate the stock is cheap relative to others -- and that may attract buyers.

Red Eléctrica Corporación's earnings per share grew by -2.7% in the last twelve months. So if Red Eléctrica Corporación grows EPS going forward, that should be a positive for the share price. Checking factors such as director buying and selling. could help you form your own view on if that will happen.

A Limitation: P/E Ratios Ignore Debt and Cash In The Bank

Don't forget that the P/E ratio considers market capitalization. That means it doesn't take debt or cash into account. Hypothetically, a company could reduce its future P/E ratio by spending its cash (or taking on debt) to achieve higher earnings.

While growth expenditure doesn't always pay off, the point is that it is a good option to have; but one that the P/E ratio ignores.

Red Eléctrica Corporación's Balance Sheet

Red Eléctrica Corporación has net debt worth 53% of its market capitalization. This is a reasonably significant level of debt -- all else being equal you'd expect a much lower P/E than if it had net cash.

The Bottom Line On Red Eléctrica Corporación's P/E Ratio

Red Eléctrica Corporación has a P/E of 13.1. That's below the average in the ES market, which is 16.9. The meaningful debt load is probably contributing to low expectations, even though it has improved earnings recently.

When the market is wrong about a stock, it gives savvy investors an opportunity. If the reality for a company is not as bad as the P/E ratio indicates, then the share price should increase as the market realizes this. So this free visualization of the analyst consensus on future earnings could help you make the right decision about whether to buy, sell, or hold.

But note: Red Eléctrica Corporación may not be the best stock to buy. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20).

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About BME:RED

Redeia Corporación

Engages in the electricity transmission, and system operation and management of the transmission network for the electricity system in Spain and internationally.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor