Advertisement

- Spain

- /

- Communications

- /

- BME:EZE

Grupo Ezentis, S.A.'s (BME:EZE) 27% Share Price Plunge Could Signal Some Risk

Unfortunately for some shareholders, the Grupo Ezentis, S.A. (BME:EZE) share price has dived 27% in the last thirty days, prolonging recent pain. Still, a bad month hasn't completely ruined the past year with the stock gaining 34%, which is great even in a bull market.

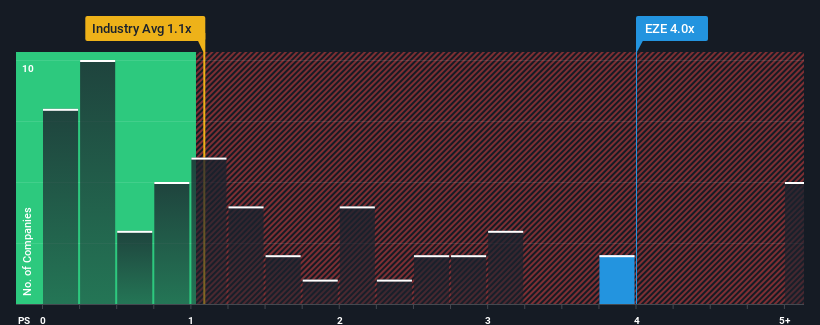

In spite of the heavy fall in price, you could still be forgiven for thinking Grupo Ezentis is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 4x, considering almost half the companies in Spain's Communications industry have P/S ratios below 1.1x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

See our latest analysis for Grupo Ezentis

How Has Grupo Ezentis Performed Recently?

For instance, Grupo Ezentis' receding revenue in recent times would have to be some food for thought. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/S from collapsing. If not, then existing shareholders may be quite nervous about the viability of the share price.

Although there are no analyst estimates available for Grupo Ezentis, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.How Is Grupo Ezentis' Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as steep as Grupo Ezentis' is when the company's growth is on track to outshine the industry decidedly.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 86%. This means it has also seen a slide in revenue over the longer-term as revenue is down 96% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

In contrast to the company, the rest of the industry is expected to grow by 2.8% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

In light of this, it's alarming that Grupo Ezentis' P/S sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

The Bottom Line On Grupo Ezentis' P/S

A significant share price dive has done very little to deflate Grupo Ezentis' very lofty P/S. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Grupo Ezentis currently trades on a much higher than expected P/S since its recent revenues have been in decline over the medium-term. With a revenue decline on investors' minds, the likelihood of a souring sentiment is quite high which could send the P/S back in line with what we'd expect. Unless the the circumstances surrounding the recent medium-term improve, it wouldn't be wrong to expect a a difficult period ahead for the company's shareholders.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Grupo Ezentis (at least 2 which make us uncomfortable), and understanding them should be part of your investment process.

If these risks are making you reconsider your opinion on Grupo Ezentis, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BME:EZE

Imperfect balance sheet with very low risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|20.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor