Advertisement

Dividend Investors: Don't Be Too Quick To Buy Altia Consultores, S.A. (BME:ALC) For Its Upcoming Dividend

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Altia Consultores, S.A. (BME:ALC) is about to go ex-dividend in just 3 days. You can purchase shares before the 30th of November in order to receive the dividend, which the company will pay on the 2nd of December.

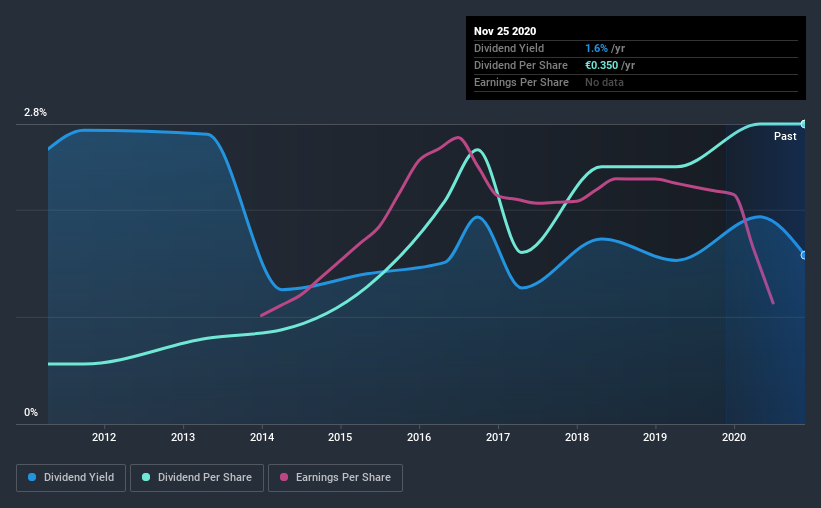

Altia Consultores's next dividend payment will be €0.12 per share, and in the last 12 months, the company paid a total of €0.35 per share. Based on the last year's worth of payments, Altia Consultores stock has a trailing yield of around 1.6% on the current share price of €22.2. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

See our latest analysis for Altia Consultores

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Fortunately Altia Consultores's payout ratio is modest, at just 29% of profit. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. It paid out more than half (61%) of its free cash flow in the past year, which is within an average range for most companies.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see how much of its profit Altia Consultores paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. Altia Consultores's earnings per share have fallen at approximately 5.8% a year over the previous five years. Such a sharp decline casts doubt on the future sustainability of the dividend.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Altia Consultores has delivered 17% dividend growth per year on average over the past 10 years.

The Bottom Line

Has Altia Consultores got what it takes to maintain its dividend payments? Earnings per share have fallen significantly, although at least Altia Consultores paid out less than half of its profits and free cash flow over the last year, leaving some margin of safety. To summarise, Altia Consultores looks okay on this analysis, although it doesn't appear a stand-out opportunity.

If you want to look further into Altia Consultores, it's worth knowing the risks this business faces. For example, Altia Consultores has 2 warning signs (and 1 which is a bit unpleasant) we think you should know about.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade Altia Consultores, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About BME:ALC

Altia Consultores

Operates in the information and communication technologies (ICT) sector in Spain and internationally.

Excellent balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.2% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|90.0% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.6% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.1% undervalued

AG

Community Contributor