Advertisement

- Spain

- /

- Metals and Mining

- /

- BME:ACX

These 4 Measures Indicate That Acerinox (BME:ACX) Is Using Debt Extensively

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Acerinox, S.A. (BME:ACX) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Acerinox

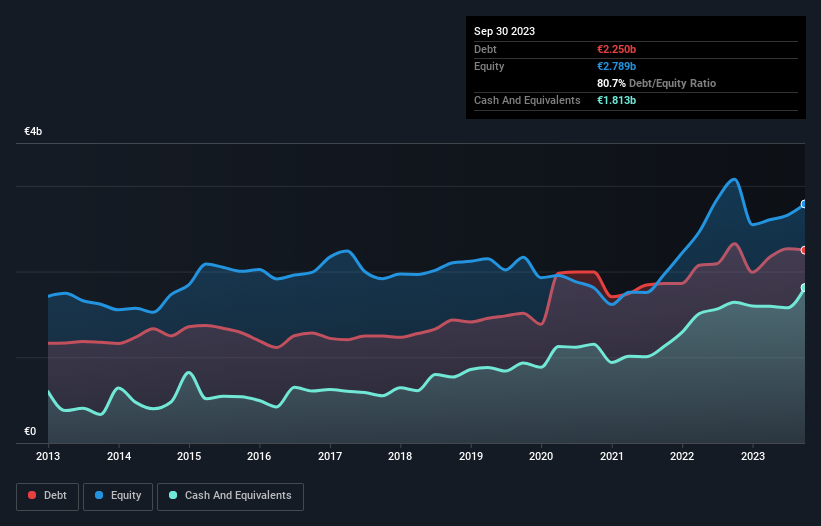

What Is Acerinox's Net Debt?

As you can see below, Acerinox had €2.25b of debt, at September 2023, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of €1.81b, its net debt is less, at about €437.0m.

How Healthy Is Acerinox's Balance Sheet?

We can see from the most recent balance sheet that Acerinox had liabilities of €2.01b falling due within a year, and liabilities of €1.77b due beyond that. Offsetting these obligations, it had cash of €1.81b as well as receivables valued at €743.0m due within 12 months. So its liabilities total €1.22b more than the combination of its cash and short-term receivables.

Acerinox has a market capitalization of €2.60b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Acerinox has a low net debt to EBITDA ratio of only 0.64. And its EBIT easily covers its interest expense, being 14.2 times the size. So we're pretty relaxed about its super-conservative use of debt. In fact Acerinox's saving grace is its low debt levels, because its EBIT has tanked 60% in the last twelve months. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Acerinox's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Looking at the most recent three years, Acerinox recorded free cash flow of 41% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

Acerinox's EBIT growth rate and level of total liabilities definitely weigh on it, in our esteem. But the good news is it seems to be able to cover its interest expense with its EBIT with ease. Looking at all the angles mentioned above, it does seem to us that Acerinox is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example - Acerinox has 3 warning signs we think you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BME:ACX

Acerinox

Manufactures and distributes stainless steel and high-performance alloys in Spain, the United States, Africa, Asia, rest of Europe, and internationally.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.564.5% undervalued

61 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.825.6% undervalued

23 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23053.3% overvalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

17 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32038.5% undervalued

32 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

BR

browser on Bentley Systems ·

Bentley Systems’ Strategic Positioning in the Digital Infrastructure Cycle

Fair Value:US$15.72102.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6526.7% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AR

ariz_scribe on Marti Technologies ·

$MRT at Roth - Pick of the Panel

Fair Value:US$1.9628.6% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.3% undervalued

89 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.8% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23053.3% overvalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

17 likesusers have liked this narrative