Distribuidora Internacional de Alimentación (BME:DIA) has been catching the attention of investors lately, and for good reason. While there is no headline-grabbing event driving the latest move, the stock’s recent swings might prompt you to wonder whether this is a signal for a broader shift or just a pause in momentum. For those weighing whether to hold, sell, or even consider a position for the first time, understanding how the market is valuing DIA right now could be more crucial than ever.

Looking back, DIA has seen nearly 98% growth over the past year, a surge that stands out in any context. However, the long-term five-year return remains deep in negative territory. Shorter-term performance has been mixed. Momentum built early but slipped in the past few months, with the stock down 7% over the past quarter after having risen sharply earlier this year. This back-and-forth points to investors constantly recalibrating their expectations as the company reports meaningful, if not explosive, progress in revenues and profits.

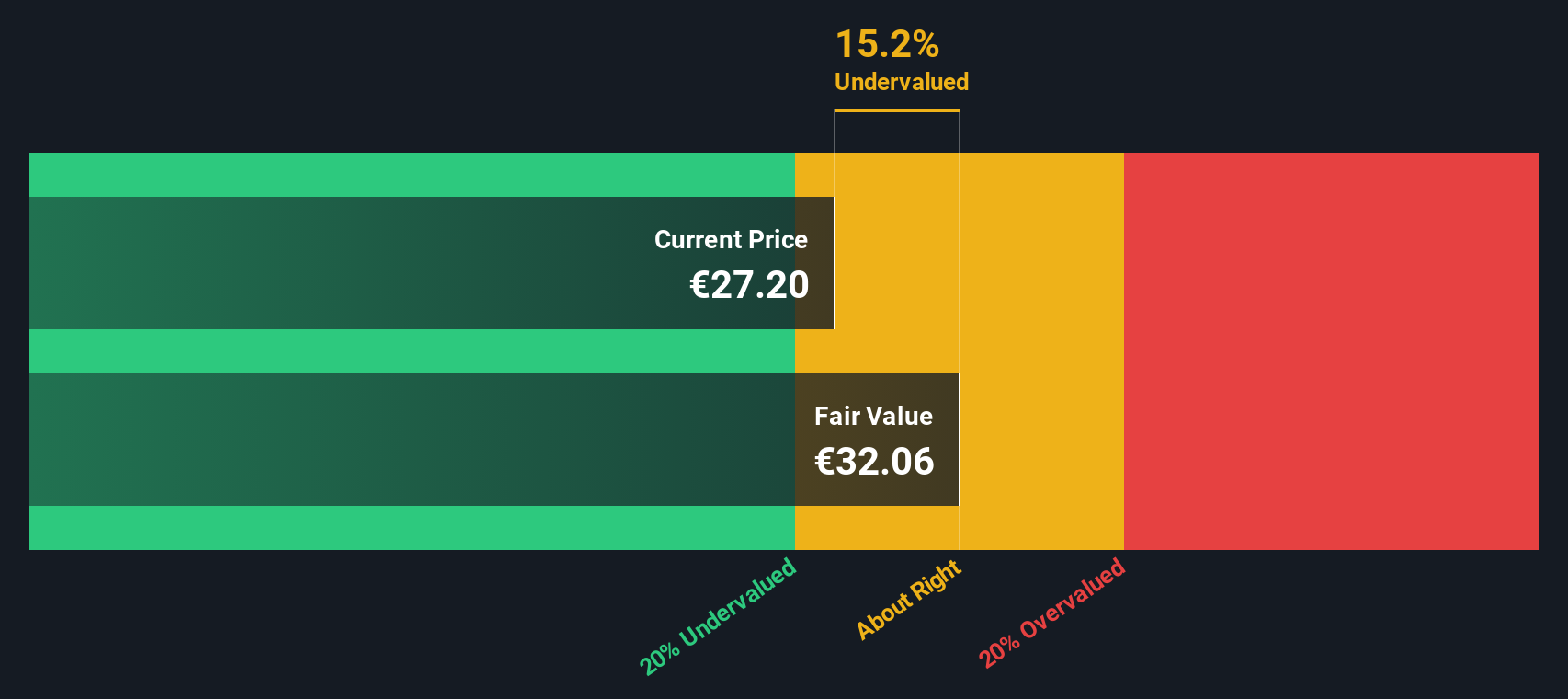

Is DIA undervalued after its pullback, or have gains already captured any future upside? The next step is to dig into what the numbers really tell us about where the market might be heading.

Advertisement

Price-to-Earnings of 39.1x: Is it justified?

Based on the price-to-earnings ratio, DIA appears significantly more expensive than the average of both its peer group and the wider industry. This suggests the market is pricing in high expectations for future growth or improved profitability that may not be matched by current performance.

The price-to-earnings (P/E) ratio measures how much investors are willing to pay for each euro of earnings generated by the company. It serves as a key yardstick when comparing one company’s valuation to others in the sector, as well as to its own historical performance. In the consumer retailing sector, this multiple helps investors gauge whether a stock’s price reflects underlying business improvements or if enthusiasm has run ahead of fundamentals.

With a P/E of 39.1x, DIA trades at almost double the peer average and more than double the industry average. This sends a clear signal that the market is assigning a premium to the company. This premium could be based on anticipated growth or strategic changes; however, it sets a demanding bar for DIA’s upcoming financial results to justify the current level.

However, any missteps in executing growth plans or unexpected competitive pressures could quickly challenge the optimistic valuation and shift investor sentiment.

While traditional price-to-earnings ratios imply the shares are expensive, our SWS DCF model comes to a similar conclusion and also suggests the stock may be trading above its fair value. This raises the question: has the market run too far, or could ongoing improvements eventually justify recent prices?

Build Your Own Distribuidora Internacional de Alimentación Narrative

If you see the story differently or want to dig deeper into the numbers yourself, you can craft your own analysis in just a few minutes. Do it your way.

A great starting point for your Distribuidora Internacional de Alimentación research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

You don’t have to stop your search here. Take your investing strategy to the next level with unique opportunities tailored to your interests and goals. There is a universe of stocks waiting for you.

Tap into growth by tracking companies transforming artificial intelligence in industries that matter through AI penny stocks.

Boost your portfolio with reliable income sources by finding top picks offering yields above 3% right now with dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.