Advertisement

- Spain

- /

- Commercial Services

- /

- BME:PSG

Don't Buy Prosegur Compañía de Seguridad, S.A. (BME:PSG) For Its Next Dividend Without Doing These Checks

Prosegur Compañía de Seguridad, S.A. (BME:PSG) stock is about to trade ex-dividend in couple of days. The ex-dividend date occurs one day before the record date which is the day on which shareholders need to be on the company's books in order to receive a dividend. The ex-dividend date is important as the process of settlement involves two full business days. So if you miss that date, you would not show up on the company's books on the record date. In other words, investors can purchase Prosegur Compañía de Seguridad's shares before the 2nd of December in order to be eligible for the dividend, which will be paid on the 4th of December.

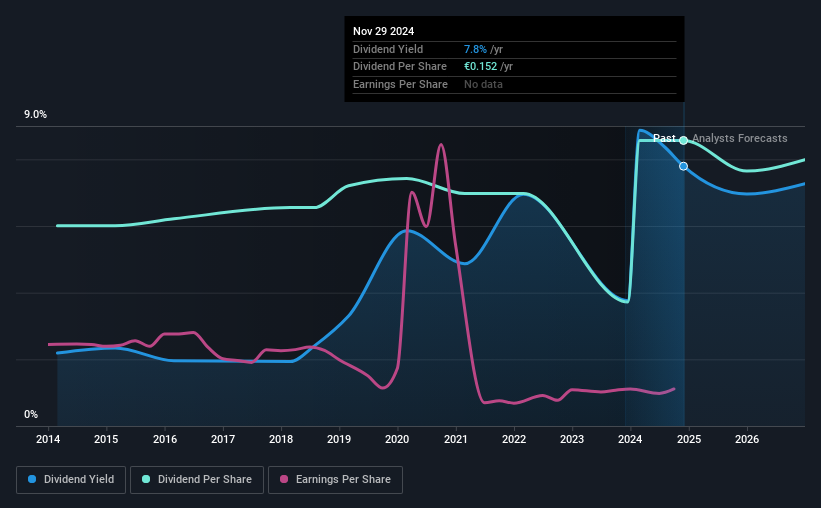

The company's next dividend payment will be €0.123363 per share, and in the last 12 months, the company paid a total of €0.15 per share. Based on the last year's worth of payments, Prosegur Compañía de Seguridad stock has a trailing yield of around 7.8% on the current share price of €1.954. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to check whether the dividend payments are covered, and if earnings are growing.

See our latest analysis for Prosegur Compañía de Seguridad

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Prosegur Compañía de Seguridad paid out 140% of profit in the past year, which we think is typically not sustainable unless there are mitigating characteristics such as unusually strong cash flow or a large cash balance. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Dividends consumed 51% of the company's free cash flow last year, which is within a normal range for most dividend-paying organisations.

It's disappointing to see that the dividend was not covered by profits, but cash is more important from a dividend sustainability perspective, and Prosegur Compañía de Seguridad fortunately did generate enough cash to fund its dividend. Still, if the company repeatedly paid a dividend greater than its profits, we'd be concerned. Extraordinarily few companies are capable of persistently paying a dividend that is greater than their profits.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. With that in mind, we're discomforted by Prosegur Compañía de Seguridad's 11% per annum decline in earnings in the past five years. Ultimately, when earnings per share decline, the size of the pie from which dividends can be paid, shrinks.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Prosegur Compañía de Seguridad has delivered 3.6% dividend growth per year on average over the past 10 years. The only way to pay higher dividends when earnings are shrinking is either to pay out a larger percentage of profits, spend cash from the balance sheet, or borrow the money. Prosegur Compañía de Seguridad is already paying out 140% of its profits, and with shrinking earnings we think it's unlikely that this dividend will grow quickly in the future.

The Bottom Line

Is Prosegur Compañía de Seguridad worth buying for its dividend? Earnings per share have been in decline, which is not encouraging. Additionally, Prosegur Compañía de Seguridad is paying out quite a high percentage of its earnings, and more than half its cash flow, so it's hard to evaluate whether the company is reinvesting enough in its business to improve its situation. It's not the most attractive proposition from a dividend perspective, and we'd probably give this one a miss for now.

With that being said, if you're still considering Prosegur Compañía de Seguridad as an investment, you'll find it beneficial to know what risks this stock is facing. In terms of investment risks, we've identified 2 warning signs with Prosegur Compañía de Seguridad and understanding them should be part of your investment process.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BME:PSG

Proven track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor