Sacyr (BME:SCYR) has been making the rounds on investors’ watchlists after its latest price moves. There hasn’t been a headline event behind the change, which means all eyes are turning to what the underlying story in the numbers might be telling us. Sometimes, when stocks start to drift or pick up steam without a clear trigger, it pays to look past the noise and ask whether the market is starting to spot value, or if there’s more risk under the hood than expected.

Momentum for Sacyr over the past year tells an interesting story. After a solid 16% gain over the last twelve months, the share price has built on multi-year growth, rising over 90% in three years and more than doubling in five. Performance in the past month has pulled back slightly, but steady revenue and net income growth have kept long-term prospects in focus even as shorter-term volatility has crept in.

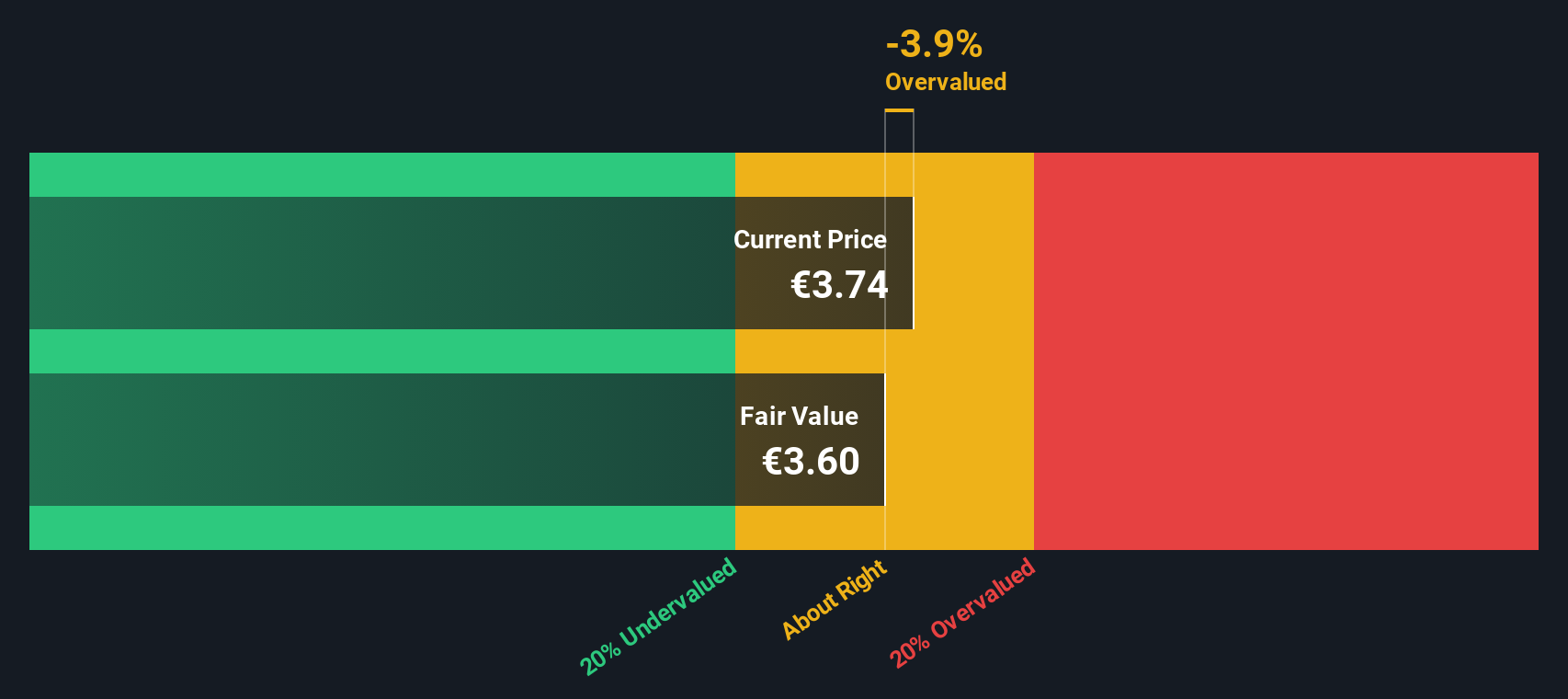

With that in mind, is the market giving investors a window to buy Sacyr at a discount, or has the recent run locked in expectations for future growth?

Advertisement

Most Popular Narrative: 4.4% Overvalued

According to Panayiotis, the most popular narrative suggests that Sacyr is trading at a modest premium to its fair value, factoring in projected moderate growth and future profitability. This viewpoint considers Sacyr's strategic push into renewables and digital infrastructure upgrades as potential catalysts for continued expansion, yet maintains a cautious stance on the company's overall valuation.

New Services & Projects: Sacyr’s pipeline includes opportunities in renewables, sustainable infrastructure, and digital upgrades. These initiatives, if successfully executed, could lift revenue beyond mere inflation.

Curious why Sacyr's growth ambitions have not translated into a discount? This narrative combines a surprising blend of steady margin expectations with a forward profit multiple that is rarely seen in the engineering space. What are the assumptions holding up this premium? If you want to uncover exactly how the future financials power this valuation, you will want to read further.

However, execution delays or tighter regulations could quickly challenge these growth assumptions. This reminds investors that optimism in infrastructure comes with persistent risks.

While the most popular narrative centers on future growth and profitability, our DCF model points to a very different outcome. This suggests the stock may not be as attractively priced as some believe. Could this deeper dive into cash flows shift the outlook?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sacyr for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Sacyr Narrative

If you see things differently or want to dig deeper on your own terms, building your own Sacyr narrative is quick and straightforward. Do it your way.

Set yourself up for success by acting now and tapping into investment themes that could define tomorrow’s winners. Here are three powerful ways to expand your watchlist and make smarter choices:

Capture the potential for breakout returns by spotting market underdogs showing strong cash-flow signals through our undervalued stocks based on cash flows.

Get in early on companies leading medical innovation by using our gateway to next-generation healthcare AI stocks opportunities.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks