Advertisement

After Leaping 36% LUDWIG BECK am Rathauseck - Textilhaus Feldmeier AG (ETR:ECK) Shares Are Not Flying Under The Radar

LUDWIG BECK am Rathauseck - Textilhaus Feldmeier AG (ETR:ECK) shareholders would be excited to see that the share price has had a great month, posting a 36% gain and recovering from prior weakness. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 27% over that time.

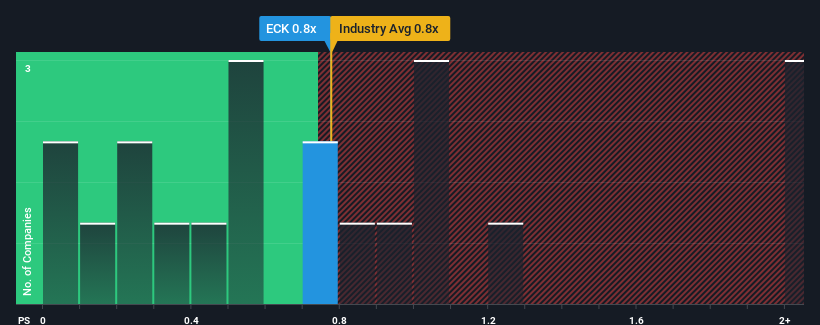

Even after such a large jump in price, it's still not a stretch to say that LUDWIG BECK am Rathauseck - Textilhaus Feldmeier's price-to-sales (or "P/S") ratio of 0.8x right now seems quite "middle-of-the-road" compared to the Multiline Retail industry in Germany, seeing as it matches the P/S ratio of the wider industry. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for LUDWIG BECK am Rathauseck - Textilhaus Feldmeier

What Does LUDWIG BECK am Rathauseck - Textilhaus Feldmeier's Recent Performance Look Like?

LUDWIG BECK am Rathauseck - Textilhaus Feldmeier has been doing a decent job lately as it's been growing revenue at a reasonable pace. Perhaps the expectation moving forward is that the revenue growth will track in line with the wider industry for the near term, which has kept the P/S subdued. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Although there are no analyst estimates available for LUDWIG BECK am Rathauseck - Textilhaus Feldmeier, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.What Are Revenue Growth Metrics Telling Us About The P/S?

In order to justify its P/S ratio, LUDWIG BECK am Rathauseck - Textilhaus Feldmeier would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered a decent 6.2% gain to the company's revenues. This was backed up an excellent period prior to see revenue up by 40% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Comparing that to the industry, which is predicted to deliver 12% growth in the next 12 months, the company's momentum is pretty similar based on recent medium-term annualised revenue results.

With this in consideration, it's clear to see why LUDWIG BECK am Rathauseck - Textilhaus Feldmeier's P/S matches up closely to its industry peers. It seems most investors are expecting to see average growth rates continue into the future and are only willing to pay a moderate amount for the stock.

The Final Word

LUDWIG BECK am Rathauseck - Textilhaus Feldmeier appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

It appears to us that LUDWIG BECK am Rathauseck - Textilhaus Feldmeier maintains its moderate P/S off the back of its recent three-year growth being in line with the wider industry forecast. With previous revenue trends that keep up with the current industry outlook, it's hard to justify the company's P/S ratio deviating much from it's current point. Unless the recent medium-term conditions change, they will continue to support the share price at these levels.

Having said that, be aware LUDWIG BECK am Rathauseck - Textilhaus Feldmeier is showing 4 warning signs in our investment analysis, and 2 of those can't be ignored.

If you're unsure about the strength of LUDWIG BECK am Rathauseck - Textilhaus Feldmeier's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:ECK

LUDWIG BECK am Rathauseck - Textilhaus Feldmeier

Engages in the wholesale and retail of textiles, clothing, hardware, and other merchandise in Germany.

Fair value with low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor