Stock Analysis

- Germany

- /

- Specialty Stores

- /

- XTRA:ZAL

German Exchange Growth Companies With Up To 30% Insider Ownership

Reviewed by Simply Wall St

Amidst a backdrop of mixed performance across major European stock markets, Germany's DAX index has shown resilience with a modest rise. This context sets the stage for exploring growth companies in Germany, particularly those with substantial insider ownership, which can be a marker of confidence in the company's prospects from those who know it best.

Top 10 Growth Companies With High Insider Ownership In Germany

| Name | Insider Ownership | Earnings Growth |

| pferdewetten.de (XTRA:EMH) | 26.8% | 75.4% |

| Deutsche Beteiligungs (XTRA:DBAN) | 35.4% | 31.6% |

| YOC (XTRA:YOC) | 24.8% | 22.2% |

| NAGA Group (XTRA:N4G) | 14.1% | 79.2% |

| Exasol (XTRA:EXL) | 25.3% | 105.4% |

| Alelion Energy Systems (DB:2FZ) | 37.4% | 106.6% |

| Stratec (XTRA:SBS) | 30.9% | 21.9% |

| Redcare Pharmacy (XTRA:RDC) | 17.7% | 48.7% |

| Your Family Entertainment (DB:RTV) | 17.5% | 116.8% |

| Friedrich Vorwerk Group (XTRA:VH2) | 18% | 30.4% |

Here's a peek at a few of the choices from the screener.

Stratec (XTRA:SBS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Stratec SE operates globally, designing and manufacturing automation and instrumentation solutions for in-vitro diagnostics and life sciences, with a market capitalization of approximately €0.56 billion.

Operations: The company generates its revenue by designing and manufacturing automation and instrumentation solutions for in-vitro diagnostics and life sciences, primarily in Germany, the European Union, and other international markets.

Insider Ownership: 30.9%

Stratec SE, a German growth company with high insider ownership, faces mixed financial prospects. While its earnings are expected to grow significantly at 21.85% annually, surpassing the German market average of 18.6%, its revenue growth is less impressive at 7.8% per year, though still above the market's 5.2%. Recent financial results indicate a downturn, with Q1 sales and net income declining from the previous year to €50.87 million and €0.447 million respectively, reflecting lower profitability and operational challenges.

- Navigate through the intricacies of Stratec with our comprehensive analyst estimates report here.

- The analysis detailed in our Stratec valuation report hints at an inflated share price compared to its estimated value.

Friedrich Vorwerk Group (XTRA:VH2)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Friedrich Vorwerk Group SE specializes in offering solutions for the transformation and transportation of energy across Germany and Europe, with a market capitalization of approximately €364 million.

Operations: The company generates revenue from various segments including electricity (€72.07 million), natural gas (€157.60 million), clean hydrogen (€28.59 million), and adjacent opportunities (€118.73 million).

Insider Ownership: 18%

Friedrich Vorwerk Group SE, a German company with high insider ownership, is poised for significant earnings growth at 30.45% annually, outpacing the broader German market's 18.6%. However, its revenue growth of 8.3% per year, though above the market average of 5.2%, suggests moderate expansion. Recent financials show improvement with Q1 net income rising to €1.56 million from €0.748 million year-over-year and revenue increasing to €81.2 million from €78.51 million, signaling operational progress despite a forecasted low return on equity of 11% in three years.

- Get an in-depth perspective on Friedrich Vorwerk Group's performance by reading our analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Friedrich Vorwerk Group shares in the market.

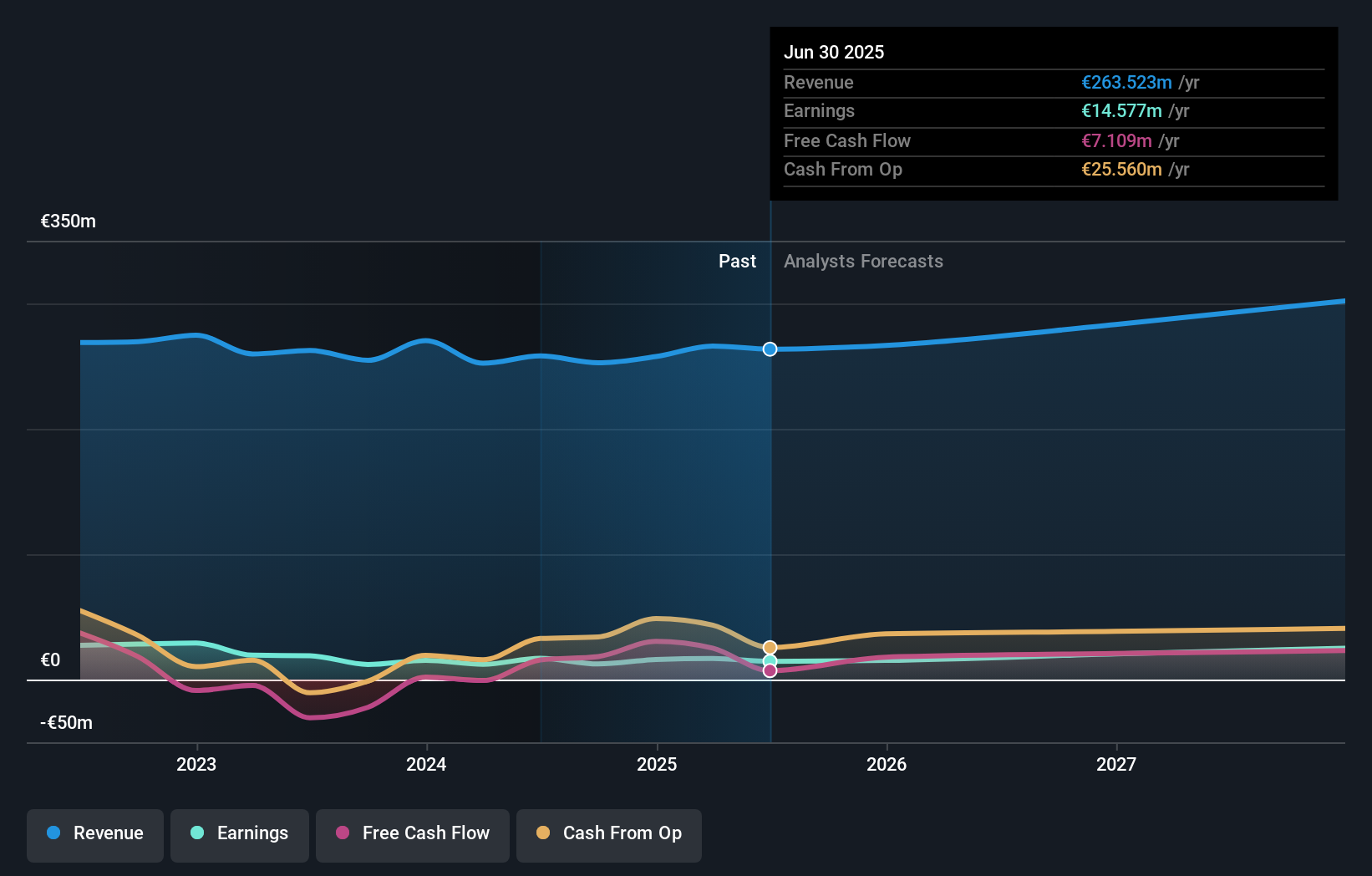

Zalando (XTRA:ZAL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Zalando SE is an online retailer specializing in fashion and lifestyle products, with a market capitalization of approximately €5.87 billion.

Operations: The company generates €10.40 billion in revenue from its online fashion and lifestyle platform.

Insider Ownership: 10.4%

Zalando SE, a growth-focused company in Germany with high insider ownership, trades at 55% below its estimated fair value, indicating potential undervaluation. Despite a modest revenue growth forecast of 5.4% per year, earnings are expected to surge by 26.56% annually over the next three years. Recent activities include several conference presentations and an earnings guidance suggesting stable sales growth and operational profit for 2024. However, its return on equity is projected to remain low at 12.7%.

- Click here to discover the nuances of Zalando with our detailed analytical future growth report.

- Our comprehensive valuation report raises the possibility that Zalando is priced higher than what may be justified by its financials.

Key Takeaways

- Embark on your investment journey to our 18 Fast Growing German Companies With High Insider Ownership selection here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Zalando is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:ZAL

Excellent balance sheet with reasonable growth potential.