- Germany

- /

- Oil and Gas

- /

- XTRA:CE2

CropEnergies AG's (ETR:CE2) Stock Has Been Sliding But Fundamentals Look Strong: Is The Market Wrong?

CropEnergies (ETR:CE2) has had a rough three months with its share price down 17%. But if you pay close attention, you might gather that its strong financials could mean that the stock could potentially see an increase in value in the long-term, given how markets usually reward companies with good financial health. Specifically, we decided to study CropEnergies' ROE in this article.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

Check out our latest analysis for CropEnergies

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for CropEnergies is:

19% = €143m ÷ €767m (Based on the trailing twelve months to May 2023).

The 'return' is the amount earned after tax over the last twelve months. That means that for every €1 worth of shareholders' equity, the company generated €0.19 in profit.

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

CropEnergies' Earnings Growth And 19% ROE

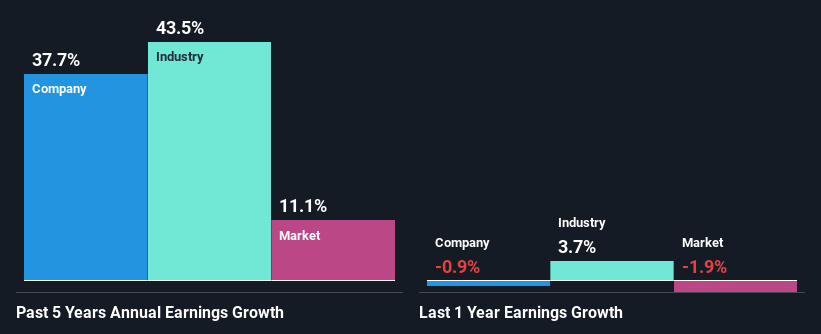

To begin with, CropEnergies seems to have a respectable ROE. Yet, the fact that the company's ROE is lower than the industry average of 27% does temper our expectations. Still, we can see that CropEnergies has seen a remarkable net income growth of 38% over the past five years. We believe that there might be other aspects that are positively influencing the company's earnings growth. Such as - high earnings retention or an efficient management in place. Bear in mind, the company does have a respectable ROE. It is just that the industry ROE is higher. So this also does lend some color to the high earnings growth seen by the company.

As a next step, we compared CropEnergies' net income growth with the industry and found that the company has a similar growth figure when compared with the industry average growth rate of 43% in the same period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if CropEnergies is trading on a high P/E or a low P/E, relative to its industry.

Is CropEnergies Making Efficient Use Of Its Profits?

The three-year median payout ratio for CropEnergies is 35%, which is moderately low. The company is retaining the remaining 65%. By the looks of it, the dividend is well covered and CropEnergies is reinvesting its profits efficiently as evidenced by its exceptional growth which we discussed above.

Moreover, CropEnergies is determined to keep sharing its profits with shareholders which we infer from its long history of paying a dividend for at least ten years.

Conclusion

On the whole, we feel that CropEnergies' performance has been quite good. Particularly, we like that the company is reinvesting heavily into its business at a moderate rate of return. Unsurprisingly, this has led to an impressive earnings growth. With that said, on studying the latest analyst forecasts, we found that while the company has seen growth in its past earnings, analysts expect its future earnings to shrink. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:CE2

CropEnergies

Manufactures and distributes bioethanol, and other biofuels and related products produced from grain or other agricultural raw materials in Germany and internationally.

Flawless balance sheet average dividend payer.