- Germany

- /

- Diversified Financial

- /

- XTRA:HYQ

Top German Growth Companies With High Insider Ownership In July 2024

Reviewed by Simply Wall St

As of July 2024, the German market has shown resilience with a notable 1.32% gain in the DAX index, reflecting a broader positive trend across major European stock indices. This uptick comes amidst varied economic signals, suggesting investors are navigating through periods of uncertainty with cautious optimism. In such a market environment, growth companies with high insider ownership can be particularly compelling. These firms often benefit from aligned interests between shareholders and management, potentially leading to more prudent long-term decision-making and robust handling of evolving economic dynamics.

Top 10 Growth Companies With High Insider Ownership In Germany

| Name | Insider Ownership | Earnings Growth |

| pferdewetten.de (XTRA:EMH) | 26.8% | 75.4% |

| Deutsche Beteiligungs (XTRA:DBAN) | 39.1% | 31.6% |

| YOC (XTRA:YOC) | 24.8% | 21.8% |

| NAGA Group (XTRA:N4G) | 14.1% | 79.2% |

| Exasol (XTRA:EXL) | 25.3% | 105.4% |

| Alelion Energy Systems (DB:2FZ) | 37.4% | 106.6% |

| Stratec (XTRA:SBS) | 30.9% | 21.9% |

| elumeo (XTRA:ELB) | 25.8% | 99.1% |

| Redcare Pharmacy (XTRA:RDC) | 17.7% | 47.4% |

| Friedrich Vorwerk Group (XTRA:VH2) | 18% | 30.4% |

Let's explore several standout options from the results in the screener.

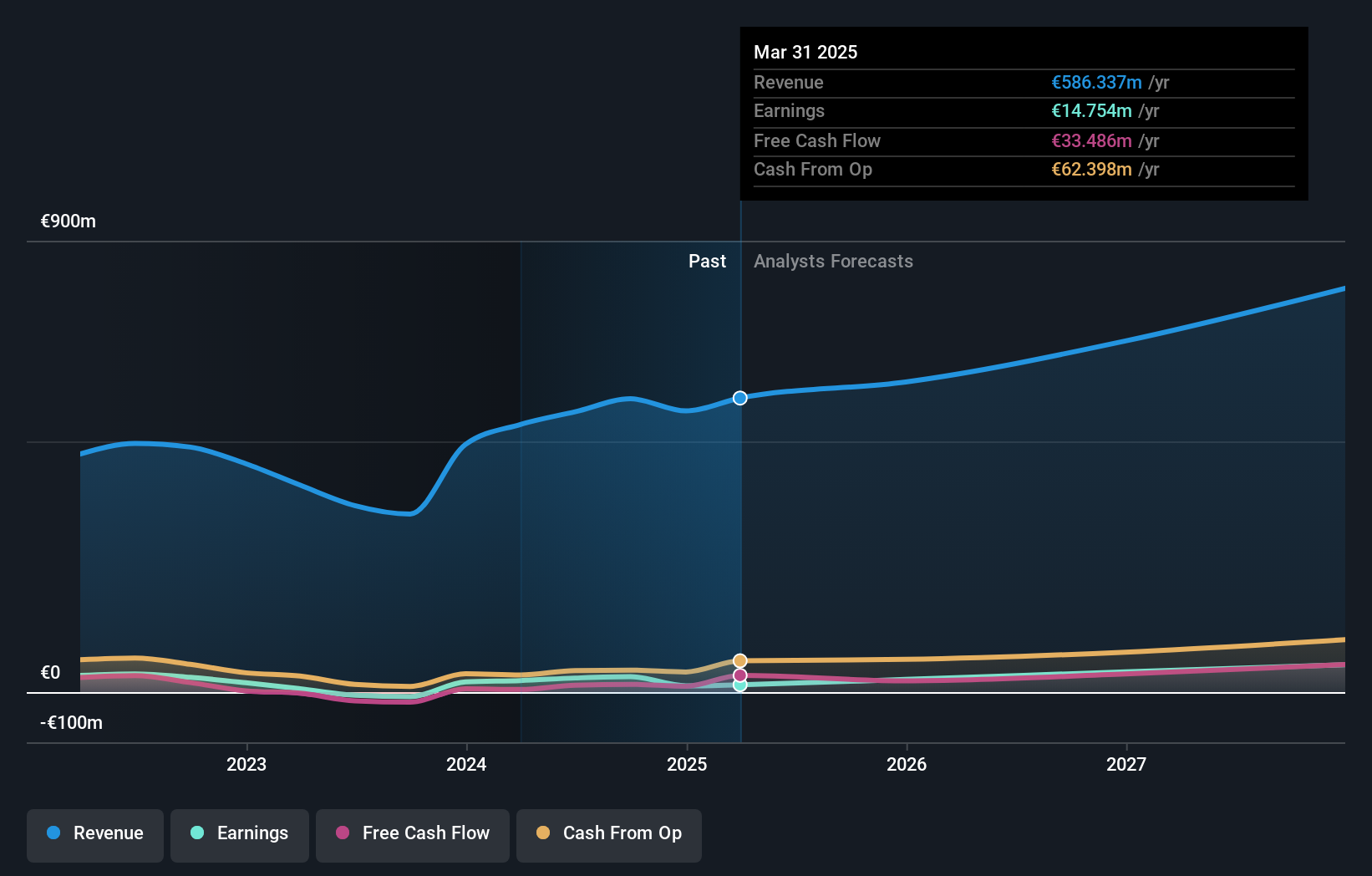

Hypoport (XTRA:HYQ)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hypoport SE is a technology-based financial service provider in Germany, with a market capitalization of approximately €2.06 billion.

Operations: The company generates revenue primarily through its Credit Platform and Insurance Platform, which brought in €155.60 million and €66.29 million respectively.

Insider Ownership: 35.1%

Earnings Growth Forecast: 31.9% p.a.

Hypoport SE, a German company with significant insider ownership, shows promising growth prospects. Recently reporting a substantial increase in quarterly sales to €107.47 million and net income to €3.04 million, the firm is outpacing average market expectations with forecasted annual earnings growth of 31.9% and revenue increases of 13.4%. However, its projected Return on Equity (RoE) remains modest at 9.1%, indicating potential challenges in achieving higher profitability relative to equity used.

- Navigate through the intricacies of Hypoport with our comprehensive analyst estimates report here.

- Our valuation report unveils the possibility Hypoport's shares may be trading at a premium.

Redcare Pharmacy (XTRA:RDC)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Redcare Pharmacy NV is an online pharmacy operating across the Netherlands, Germany, Italy, Belgium, Switzerland, Austria, and France with a market capitalization of approximately €2.78 billion.

Operations: The company generates revenue primarily from two segments: the DACH region (€1.62 billion) and other international markets (€0.37 billion).

Insider Ownership: 17.7%

Earnings Growth Forecast: 47.4% p.a.

Redcare Pharmacy, despite a volatile share price, reported a significant sales increase in Q1 2024 to €560.22 million from €372.05 million the previous year, reducing its net loss to €7.81 million from €10.22 million. The company's revenue growth is forecasted at 17.1% annually, outpacing the German market's 5.2%. Expected to turn profitable within three years, Redcare is trading at a substantial discount to its estimated fair value but faces shareholder dilution and low projected Return on Equity (7.5%).

- Click here and access our complete growth analysis report to understand the dynamics of Redcare Pharmacy.

- Our expertly prepared valuation report Redcare Pharmacy implies its share price may be too high.

Zalando (XTRA:ZAL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Zalando SE is an online retailer specializing in fashion and lifestyle products, with a market capitalization of approximately €6.06 billion.

Operations: The company generates €10.40 billion in revenue from its online fashion and lifestyle platform.

Insider Ownership: 10.4%

Earnings Growth Forecast: 26.4% p.a.

Zalando SE, a prominent German e-commerce company, reported a modest revenue growth forecast between 0% and 5% for 2024. Despite a net loss of €8.9 million in Q1 2024, earnings are expected to grow significantly at an annual rate of 26.42%, outpacing the broader German market's forecasted growth. The company is trading at a significant discount to its fair value, indicating potential undervaluation. However, Zalando's Return on Equity is projected to remain low at 12.6%, reflecting some efficiency challenges ahead.

- Take a closer look at Zalando's potential here in our earnings growth report.

- The analysis detailed in our Zalando valuation report hints at an inflated share price compared to its estimated value.

Next Steps

- Investigate our full lineup of 18 Fast Growing German Companies With High Insider Ownership right here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Hypoport might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:HYQ

Hypoport

Develops and markets technology platforms for the financial services, property, and insurance industries in Germany.

Reasonable growth potential with adequate balance sheet.