- Germany

- /

- Specialty Stores

- /

- XTRA:ZAL

3 German Growth Stocks With Up To 35% Insider Ownership

Reviewed by Simply Wall St

As the German DAX index ekes out modest gains amidst a cautious European market, investors are increasingly looking at growth companies with substantial insider ownership as potential opportunities. In this article, we explore three German growth stocks where insiders hold up to 35% of the shares, a factor often seen as a strong vote of confidence in the company's future prospects.

Top 10 Growth Companies With High Insider Ownership In Germany

| Name | Insider Ownership | Earnings Growth |

| pferdewetten.de (XTRA:EMH) | 26.8% | 98.3% |

| Stemmer Imaging (XTRA:S9I) | 25.2% | 23.2% |

| Deutsche Beteiligungs (XTRA:DBAN) | 39.5% | 54.1% |

| Exasol (XTRA:EXL) | 25.3% | 117.1% |

| adidas (XTRA:ADS) | 16.6% | 42.1% |

| Alelion Energy Systems (DB:2FZ) | 37.4% | 106.6% |

| Beyond Frames Entertainment (DB:8WP) | 10.8% | 112.2% |

| R. STAHL (XTRA:RSL2) | 37.9% | 59.3% |

| Friedrich Vorwerk Group (XTRA:VH2) | 18% | 24.6% |

| elumeo (XTRA:ELB) | 25.8% | 120.2% |

We'll examine a selection from our screener results.

adidas (XTRA:ADS)

Simply Wall St Growth Rating: ★★★★★☆

Overview: adidas AG, with a market cap of €41.74 billion, designs, develops, produces, and markets athletic and sports lifestyle products across Europe, the Middle East, Africa, North America, Greater China, the Asia-Pacific region, and Latin America.

Operations: The company's revenue segments are as follows: Greater China (€3.26 billion), Latin America (€2.39 billion), and North America (€5.07 billion).

Insider Ownership: 16.6%

adidas AG, a growth company with high insider ownership, is forecast to see its revenue grow at 8.4% per year, outpacing the German market's 5.5%. Earnings are expected to grow significantly at 42.1% annually over the next three years, with a high return on equity forecasted at 31.5%. Recently profitable, adidas reported Q2 sales of €5.82 billion and net income of €190 million, raising its full-year guidance for currency-neutral revenues and operating profit despite unfavorable currency effects impacting profitability in 2024.

- Click here and access our complete growth analysis report to understand the dynamics of adidas.

- Insights from our recent valuation report point to the potential overvaluation of adidas shares in the market.

Hypoport (XTRA:HYQ)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hypoport SE develops and markets technology platforms for the financial services, property, and insurance industries in Germany with a market cap of €2.01 billion.

Operations: The company's revenue segments include €157.97 million from the Credit Platform, €66.89 million from the Insurance Platform, and €175.87 million from Segment Adjustment.

Insider Ownership: 35%

Hypoport SE, recently added to the MDAX Index, reported Q2 2024 sales of €110.62 million and a net income of €2.4 million, rebounding from a loss last year. Despite high share price volatility and large one-off items affecting results, its earnings are forecast to grow significantly at 34% annually over the next three years. Revenue is expected to grow faster than the German market but slower than 20% per year.

- Get an in-depth perspective on Hypoport's performance by reading our analyst estimates report here.

- Our valuation report here indicates Hypoport may be overvalued.

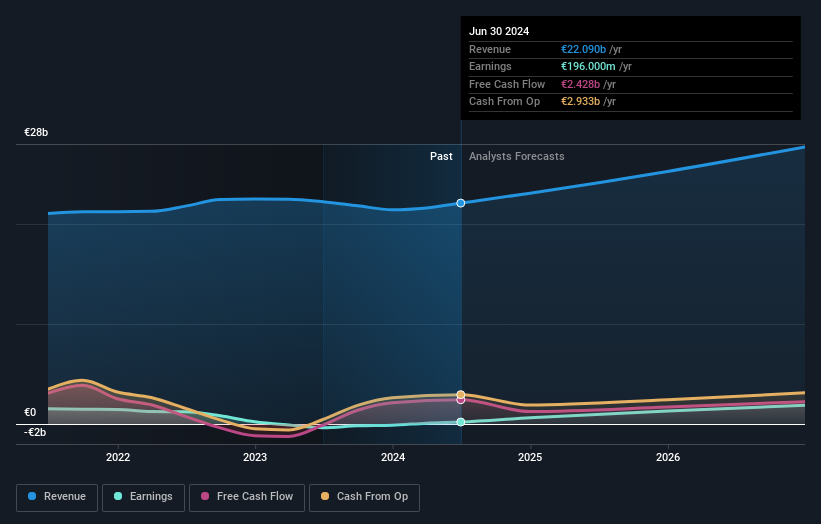

Zalando (XTRA:ZAL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Zalando SE operates an online platform for fashion and lifestyle products with a market cap of €7.42 billion.

Operations: Zalando SE generates revenue primarily through its online platform for fashion and lifestyle products, amounting to €10.49 billion.

Insider Ownership: 10.4%

Zalando SE, a growth company with high insider ownership, recently reported Q2 2024 sales of €2.64 billion and net income of €95.7 million, showing significant year-over-year improvement. Despite CFO Dr. Sandra Dembeck's upcoming departure in February 2025, the company's earnings are forecast to grow at 25.15% annually, outpacing the German market average of 20%. Trading at approximately half its estimated fair value, Zalando’s revenue growth is expected to slightly exceed the market rate.

- Unlock comprehensive insights into our analysis of Zalando stock in this growth report.

- The analysis detailed in our Zalando valuation report hints at an inflated share price compared to its estimated value.

Where To Now?

- Delve into our full catalog of 21 Fast Growing German Companies With High Insider Ownership here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Zalando might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:ZAL

Excellent balance sheet with reasonable growth potential.