Advertisement

- Germany

- /

- Consumer Durables

- /

- XTRA:TRU

Traumhaus AG (ETR:TRU) Might Not Be As Mispriced As It Looks After Plunging 35%

The Traumhaus AG (ETR:TRU) share price has fared very poorly over the last month, falling by a substantial 35%. For any long-term shareholders, the last month ends a year to forget by locking in a 53% share price decline.

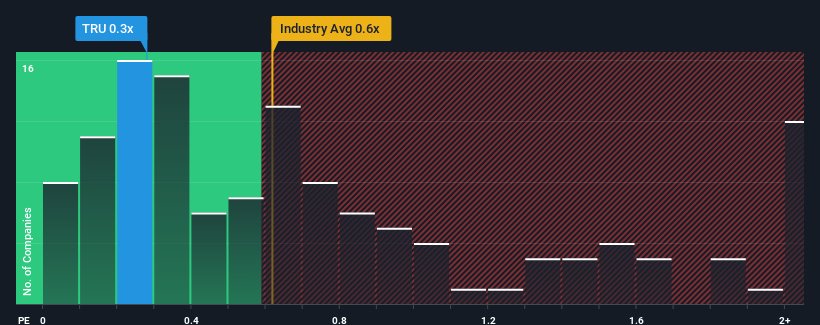

In spite of the heavy fall in price, you could still be forgiven for feeling indifferent about Traumhaus' P/S ratio of 0.3x, since the median price-to-sales (or "P/S") ratio for the Consumer Durables industry in Germany is about the same. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

View our latest analysis for Traumhaus

How Has Traumhaus Performed Recently?

Recent times haven't been great for Traumhaus as its revenue has been falling quicker than most other companies. One possibility is that the P/S is moderate because investors think the company's revenue trend will eventually fall in line with most others in the industry. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Traumhaus will help you uncover what's on the horizon.How Is Traumhaus' Revenue Growth Trending?

Traumhaus' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 29%. The last three years don't look nice either as the company has shrunk revenue by 16% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 20% per year as estimated by the dual analysts watching the company. That's shaping up to be materially higher than the 7.5% per year growth forecast for the broader industry.

In light of this, it's curious that Traumhaus' P/S sits in line with the majority of other companies. It may be that most investors aren't convinced the company can achieve future growth expectations.

What Does Traumhaus' P/S Mean For Investors?

With its share price dropping off a cliff, the P/S for Traumhaus looks to be in line with the rest of the Consumer Durables industry. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Traumhaus currently trades on a lower than expected P/S since its forecasted revenue growth is higher than the wider industry. There could be some risks that the market is pricing in, which is preventing the P/S ratio from matching the positive outlook. However, if you agree with the analysts' forecasts, you may be able to pick up the stock at an attractive price.

We don't want to rain on the parade too much, but we did also find 5 warning signs for Traumhaus (2 are potentially serious!) that you need to be mindful of.

If these risks are making you reconsider your opinion on Traumhaus, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Traumhaus might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:TRU

Traumhaus

Engages in the purchase, development, marketing, and sale of real estate properties.

Undervalued with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor