Advertisement

Traton (XTRA:8TRA) Narrows Guidance as Net Income Falls Are Core Markets Losing Their Edge?

Simply Wall St

Reviewed by Sasha Jovanovic

- Traton SE recently reported its earnings for the nine months ended September 30, 2025, posting sales of €32.32 billion and net income of €1.04 billion, both down compared to the prior year.

- This results update highlighted ongoing operational challenges, with Traton also narrowing its future guidance amid difficult market conditions in North America and Brazil.

- We'll examine how the drop in net income and revised guidance could shape Traton's broader investment outlook and future prospects.

We've found 21 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Traton Investment Narrative Recap

To be a Traton shareholder, you have to believe in the company’s ability to rebound from current sector headwinds, particularly in North America and Brazil, and deliver long-term returns through its push into electrification and commercial vehicle innovation. The latest earnings miss and narrowed guidance do increase pressure on the most immediate catalyst, strengthening order intake as macro conditions stabilize, while highlighting the risk of a prolonged demand slump, especially if market weakness endures. The impact of these results on short-term prospects is material and may weigh on investor sentiment for some time.

Among recent announcements, Traton’s July 2025 update lowering full-year revenue and unit sales guidance is particularly relevant, as it reflects management’s direct response to the ongoing volume declines and pricing pressure already cited in this quarter’s results. This move sets more cautious expectations for the rest of the year, placing additional importance on the pace of recovery in Traton’s key markets.

Yet with order books still under pressure and dealer inventories remaining high, the risk that further downgrades could follow is something investors should be aware of if...

Read the full narrative on Traton (it's free!)

Traton's outlook suggests €48.9 billion in revenue and €3.3 billion in earnings by 2028. This scenario is based on an annual revenue growth rate of 2.0% and an increase in earnings of €1.1 billion from the current €2.2 billion.

Uncover how Traton's forecasts yield a €33.26 fair value, a 20% upside to its current price.

Exploring Other Perspectives

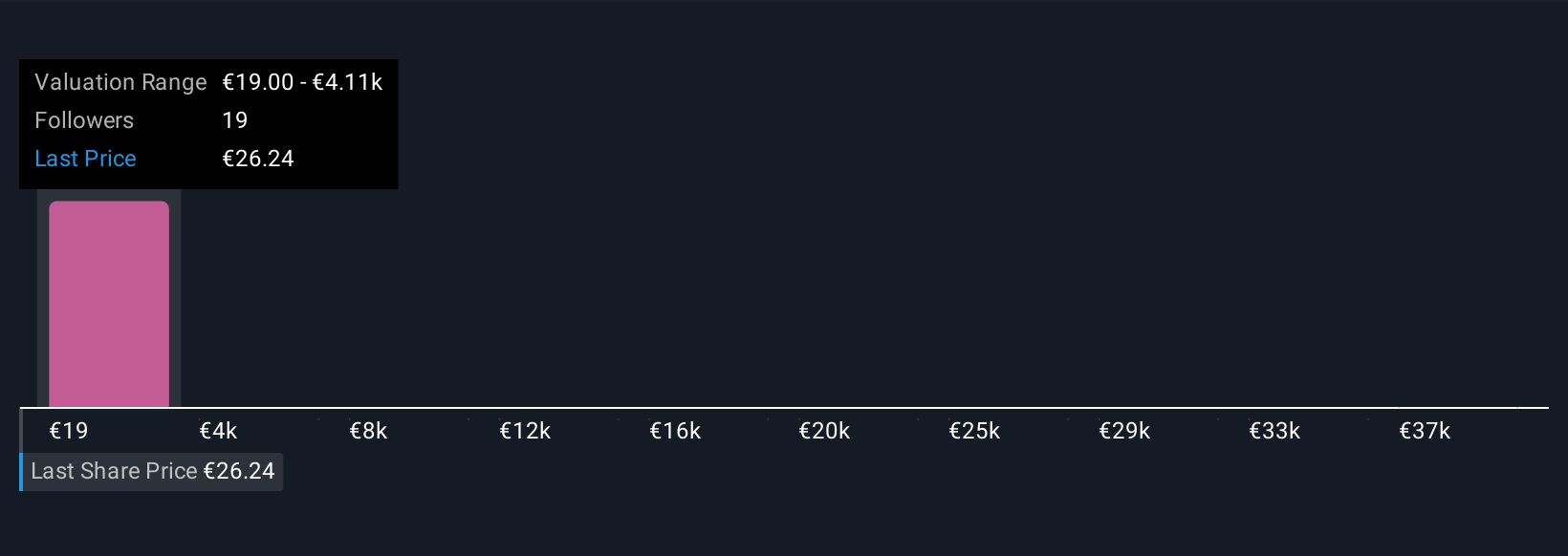

Eight fair value estimates from the Simply Wall St Community span from €19 to €40,964, underscoring wide differences in individual outlooks. While some are focused on Traton’s potential in electric mobility, others remain cautious due to ongoing demand challenges in North America and Brazil; you can explore these diverse perspectives to weigh the company’s prospects for yourself.

Explore 8 other fair value estimates on Traton - why the stock might be worth 31% less than the current price!

Build Your Own Traton Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Traton research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Traton research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Traton's overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Traton might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:8TRA

Traton

Manufactures and sells commercial vehicles in Germany, rest of Europe, the United States of America, rest of North America, Brazil, rest of South America, and internationally.

Undervalued second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|8.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.6% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor