Does the Recent Rally and EV Pivot Leave VW Shares Still Attractive in 2025?

Reviewed by Bailey Pemberton

- Wondering if Volkswagen is still a value play or if the easy money has already been made? Here is a breakdown of what the current share price is really implying, and where the valuation story might be heading next.

- Volkswagen's share price has been choppy in the short term, down 2.8% over the last week, but it is still up 9.9% over the past month, 19.2% year to date, and 27.1% over the last year, which suggests sentiment has been steadily improving.

- Recent headlines have focused on Volkswagen's ongoing push into electric vehicles, strategic partnerships, and continued restructuring to sharpen profitability. These developments help explain the shift in investor appetite. At the same time, debates around legacy combustion assets, regulatory pressures in Europe, and global competition from new EV players are keeping risk perceptions very much in play.

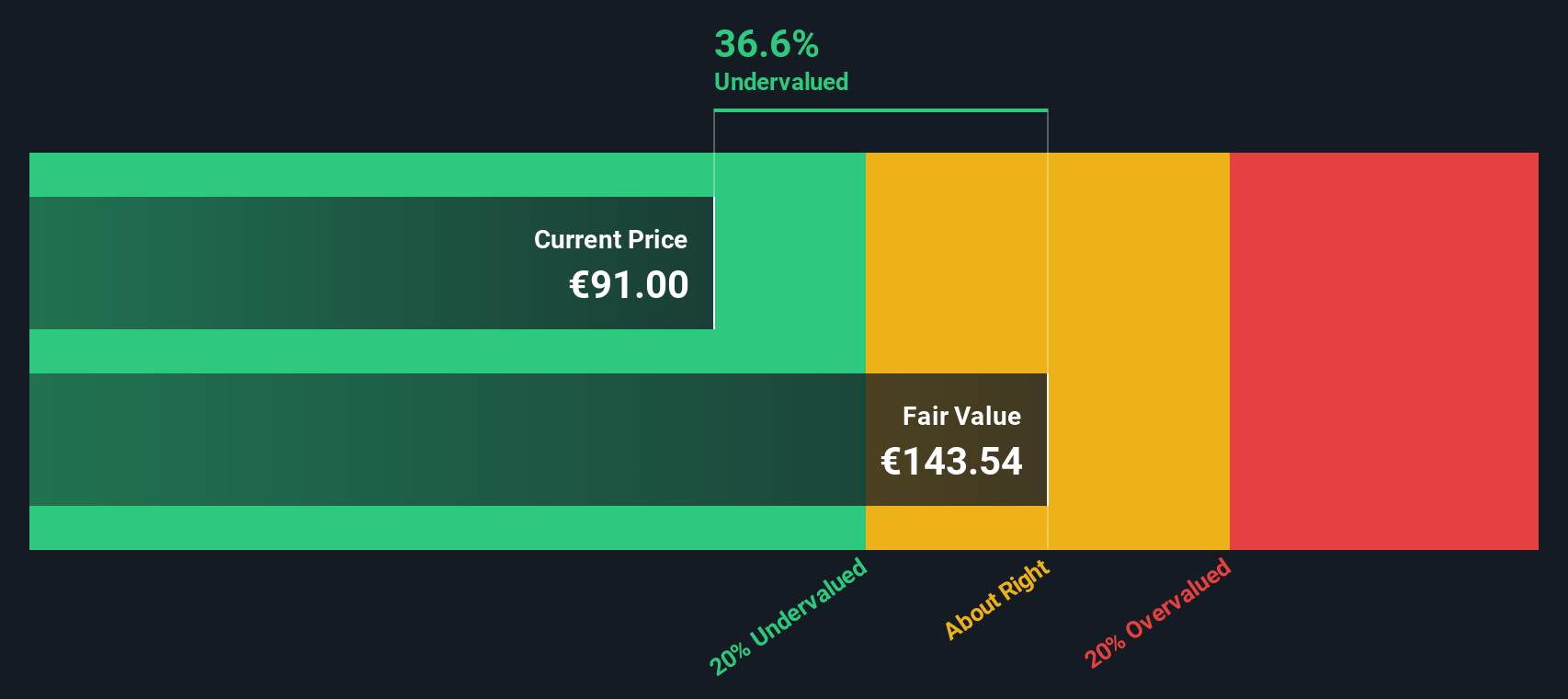

- On our checks, Volkswagen scores a solid 5/6 valuation score, indicating it looks undervalued on most of the metrics we track, but not all. Next, we will unpack those valuation approaches in detail, and then circle back at the end to a more powerful way of thinking about what Volkswagen is really worth.

Approach 1: Volkswagen Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow model estimates what a company is worth by projecting its future cash flows and then discounting those back into today’s euros, reflecting the time value of money and risk.

For Volkswagen, the latest twelve month free cash flow is negative at about €11 billion, highlighting the strain of heavy investment and industry transition. Analysts expect this to swing back into positive territory over the next few years, with Simply Wall St extrapolating those estimates further out. By 2029, free cash flow is projected to reach roughly €13.2 billion, and by 2035 the model assumes it could rise toward about €26.9 billion, with growth moderating over time.

Aggregating and discounting these projected cash flows using a 2 Stage Free Cash Flow to Equity approach yields an estimated intrinsic value of about €429 per share. Compared to the current share price, this implies Volkswagen is trading at a 75.7% discount to its DCF value, which indicates a substantial margin of safety if the cash flow recovery materializes.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Volkswagen is undervalued by 75.7%. Track this in your watchlist or portfolio, or discover 907 more undervalued stocks based on cash flows.

Approach 2: Volkswagen Price vs Earnings

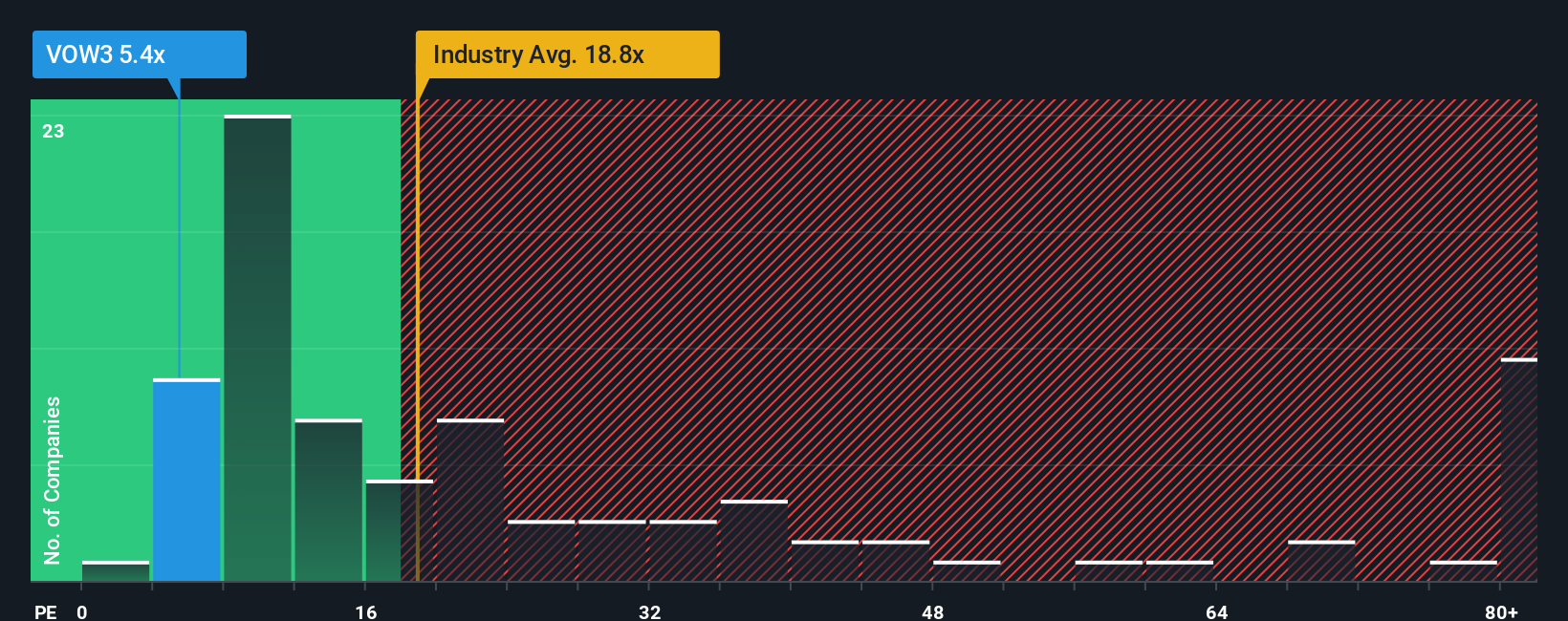

For a mature, profitable manufacturer like Volkswagen, the price to earnings ratio is a useful way to gauge how much investors are willing to pay for each euro of current profits. In general, companies with stronger growth prospects and lower perceived risk can justify a higher PE multiple, while slower growth or higher uncertainty should translate into a lower, more conservative PE.

Volkswagen currently trades on about 7.7x earnings, which is well below the Auto industry average of around 18.7x and also below the broader peer group average of roughly 24.2x. On those simple comparisons alone, the stock appears cheap. However, headline peer and industry multiples do not fully adjust for Volkswagen specific factors such as its earnings growth profile, margins, market cap and the risks tied to its strategic transition.

That is where Simply Wall St's Fair Ratio comes in, estimating what Volkswagen's PE might be given those fundamentals. For Volkswagen, the Fair Ratio is 15.9x, materially above the current 7.7x multiple. Because this measure explicitly incorporates growth, risk, profitability, industry and size, it offers a more tailored benchmark than raw peer or sector averages and, on this view, indicates that the market may be overly pessimistic.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1456 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Volkswagen Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of a company’s story with a clear financial forecast and a resulting fair value estimate. A Narrative is your version of what happens next at a company: you choose assumptions for revenue growth, profit margins and risk, and those inputs are turned into a forward-looking forecast that leads to a fair value you can compare with today’s share price to decide whether to buy, hold or sell. Narratives live inside the Simply Wall St Community page, where millions of investors can explore and share them, and they update dynamically as new information like earnings releases or major news flows through the platform. For Volkswagen, one investor might build a cautious Narrative that focuses on strategic missteps and low single digit growth with a fair value near €68, while another might emphasize EV expansion, restructuring benefits and resilient margins and arrive at a much higher fair value around €112.

For Volkswagen however we will make it really easy for you with previews of two leading Volkswagen Narratives:

Fair value: €111.60

Implied undervaluation vs last close: 6.7%

Revenue growth assumption: 2.99%

- Leans on expanding electrified and digital offerings, with BEV growth, premium mix and platform rationalization seen as key drivers of higher margins and returns.

- Assumes restructuring, local production, and partnerships such as Rivian reduce geopolitical and cost risks, supporting margin recovery and more resilient recurring revenues.

- Accepts risks from tariffs, BEV competition and capital intensity, but concludes that at consensus targets Volkswagen still offers upside with a modest valuation multiple.

Fair value: €68.40

Implied overvaluation vs last close: 52.2%

Revenue growth assumption: 1.0%

- Highlights a history of strategic missteps from diesel emissions to a slow EV pivot, leaving Volkswagen structurally exposed despite its dominant home market share.

- Points to falling profits, weak growth guidance, dependence on China and Mexico, and looming tariff risks as signs that earnings power is eroding.

- Views delayed margin improvement targets and complex, costly structures as red flags, arguing that near term, the balance of risks and rewards looks skewed to the downside.

Do you think there's more to the story for Volkswagen? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:VOW3

Volkswagen

Manufactures and sells automobiles in Germany, other European countries, North America, South America, the Asia-Pacific, and internationally.

Undervalued with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion