Advertisement

- China

- /

- Infrastructure

- /

- SHSE:600575

Benign Growth For Huaihe Energy (Group) Co.,Ltd (SHSE:600575) Underpins Stock's 27% Plummet

Huaihe Energy (Group) Co.,Ltd (SHSE:600575) shares have had a horrible month, losing 27% after a relatively good period beforehand. Still, a bad month hasn't completely ruined the past year with the stock gaining 31%, which is great even in a bull market.

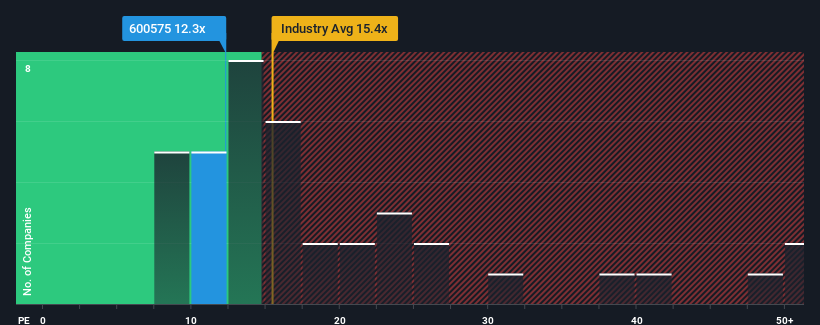

After such a large drop in price, Huaihe Energy (Group)Ltd may be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 12.3x, since almost half of all companies in China have P/E ratios greater than 34x and even P/E's higher than 65x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

With its earnings growth in positive territory compared to the declining earnings of most other companies, Huaihe Energy (Group)Ltd has been doing quite well of late. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Huaihe Energy (Group)Ltd

How Is Huaihe Energy (Group)Ltd's Growth Trending?

In order to justify its P/E ratio, Huaihe Energy (Group)Ltd would need to produce anemic growth that's substantially trailing the market.

Retrospectively, the last year delivered an exceptional 216% gain to the company's bottom line. Pleasingly, EPS has also lifted 160% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Shifting to the future, estimates from the lone analyst covering the company suggest earnings should grow by 6.3% over the next year. That's shaping up to be materially lower than the 38% growth forecast for the broader market.

With this information, we can see why Huaihe Energy (Group)Ltd is trading at a P/E lower than the market. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

What We Can Learn From Huaihe Energy (Group)Ltd's P/E?

Huaihe Energy (Group)Ltd's P/E looks about as weak as its stock price lately. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Huaihe Energy (Group)Ltd's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Huaihe Energy (Group)Ltd, and understanding should be part of your investment process.

If you're unsure about the strength of Huaihe Energy (Group)Ltd's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Huaihe Energy (Group)Ltd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600575

Huaihe Energy (Group)Ltd

Engages in the logistics and trade business in China.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|12.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|21.7% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.1% undervalued

EA

Community Contributor