Advertisement

Exploring Three Promising Asian Stocks with Strong Potential

Simply Wall St

Reviewed by Simply Wall St

As global markets experience shifts driven by trade negotiations and economic indicators, Asian markets are drawing attention with their unique dynamics and opportunities. In this environment, identifying stocks with strong fundamentals and growth potential can be particularly rewarding, especially as investors seek to navigate the evolving landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Hubei Three Gorges Tourism Group | 11.24% | -15.32% | 17.90% | ★★★★★★ |

| Korea Ratings | NA | 0.74% | 1.47% | ★★★★★★ |

| Konishi | 0.15% | 0.46% | 12.50% | ★★★★★★ |

| Hongmian Zhihui Science and Technology InnovationLtd.Guangzhou | 11.90% | -28.99% | 46.16% | ★★★★★★ |

| Anji Foodstuff | NA | 9.94% | -16.40% | ★★★★★★ |

| JHT DesignLtd | 2.19% | 33.65% | -8.51% | ★★★★★★ |

| Shanghai Haixin Group | 0.78% | -0.42% | 8.03% | ★★★★★★ |

| Guangdong Transtek Medical Electronics | 18.69% | -7.58% | -3.26% | ★★★★★☆ |

| Shenzhen Longtech Smart Control | 8.06% | 18.09% | 13.26% | ★★★★★☆ |

| Shenzhen Easttop Supply Chain Management | 73.12% | -30.87% | -1.20% | ★★★★★☆ |

Here we highlight a subset of our preferred stocks from the screener.

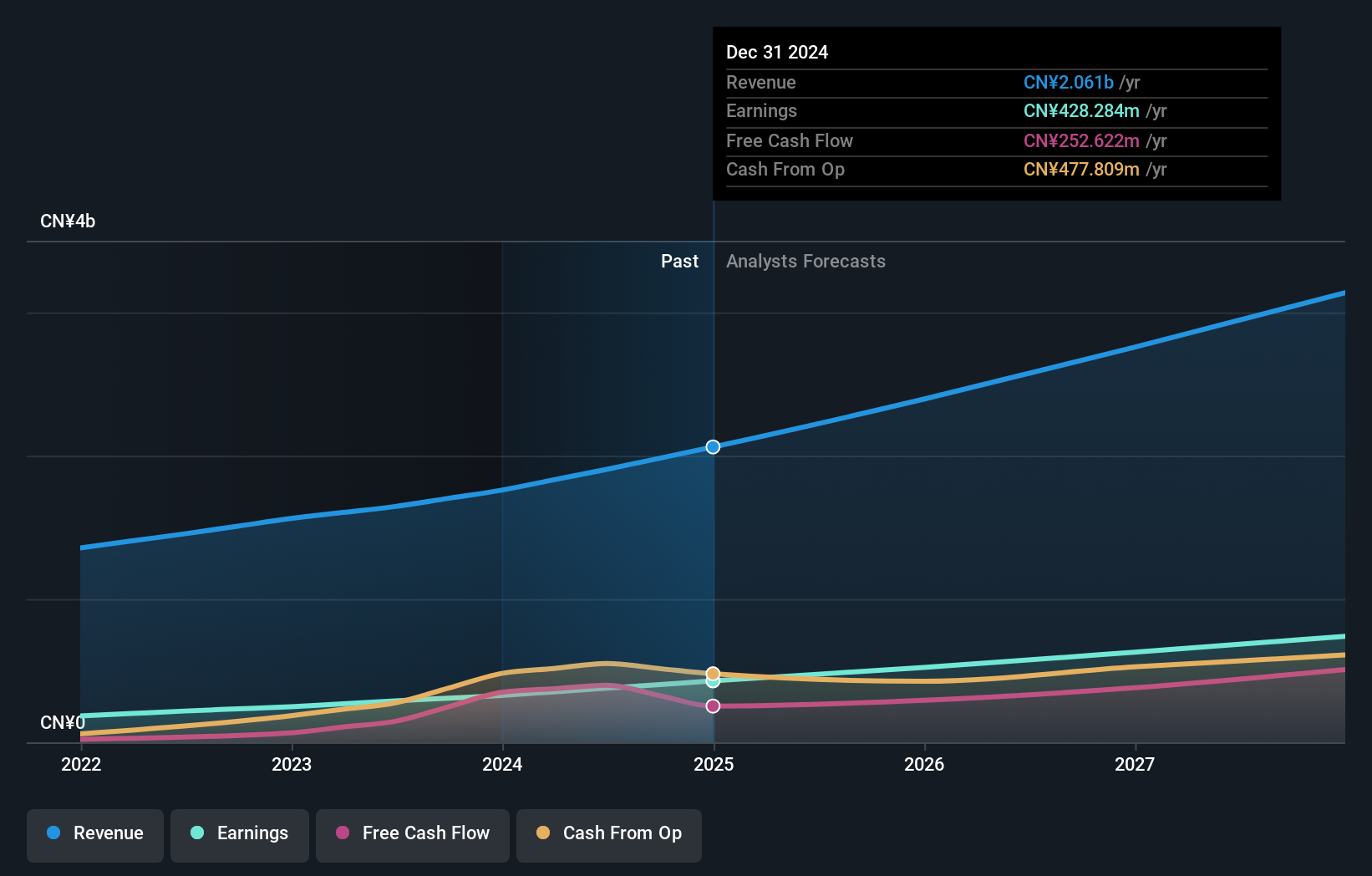

Shanghai Conant Optical (SEHK:2276)

Simply Wall St Value Rating: ★★★★★☆

Overview: Shanghai Conant Optical Co., Ltd. is a company that manufactures and sells resin spectacle lenses across multiple regions including Mainland China, the Americas, Asia, Europe, Oceania, and Africa with a market capitalization of HK$12.41 billion.

Operations: The primary revenue stream for Shanghai Conant Optical comes from the manufacturing and sales of resin spectacle lenses, generating CN¥2.06 billion.

Shanghai Conant Optical's recent performance paints a promising picture, with earnings growth of 31% outpacing the Medical Equipment industry's 9.6%. The company's net income for 2024 reached CNY 428.28 million, a notable increase from CNY 327.02 million in the previous year, while basic earnings per share rose to CNY 1.03 from CNY 0.77. Interest payments on its debt are well-covered by EBIT at an impressive ratio of over 104 times, highlighting strong financial health and stability within this small cap entity in Asia's bustling market landscape.

- Click here to discover the nuances of Shanghai Conant Optical with our detailed analytical health report.

Evaluate Shanghai Conant Optical's historical performance by accessing our past performance report.

Broadex Technologies (SZSE:300548)

Simply Wall St Value Rating: ★★★★★☆

Overview: Broadex Technologies Co., Ltd. focuses on the research, development, production, and sale of integrated optoelectronic devices for optical communications both in China and globally, with a market cap of approximately CN¥13.16 billion.

Operations: Broadex Technologies generates revenue primarily from the sale of integrated optoelectronic devices for optical communications. The company's net profit margin has shown notable trends, reflecting its financial performance dynamics.

Broadex Technologies, a notable player in the tech sector, recently showcased impressive growth with earnings rising 309.9% over the past year, far outpacing the industry average of -2.1%. Trading at 47% below its estimated fair value, it presents an intriguing opportunity for investors seeking undervalued assets. The company reported first-quarter sales of CNY 538.51 million and net income of CNY 89.7 million, a significant leap from last year's figures. Despite a volatile share price recently, Broadex's financial health is bolstered by having more cash than total debt and positive free cash flow status.

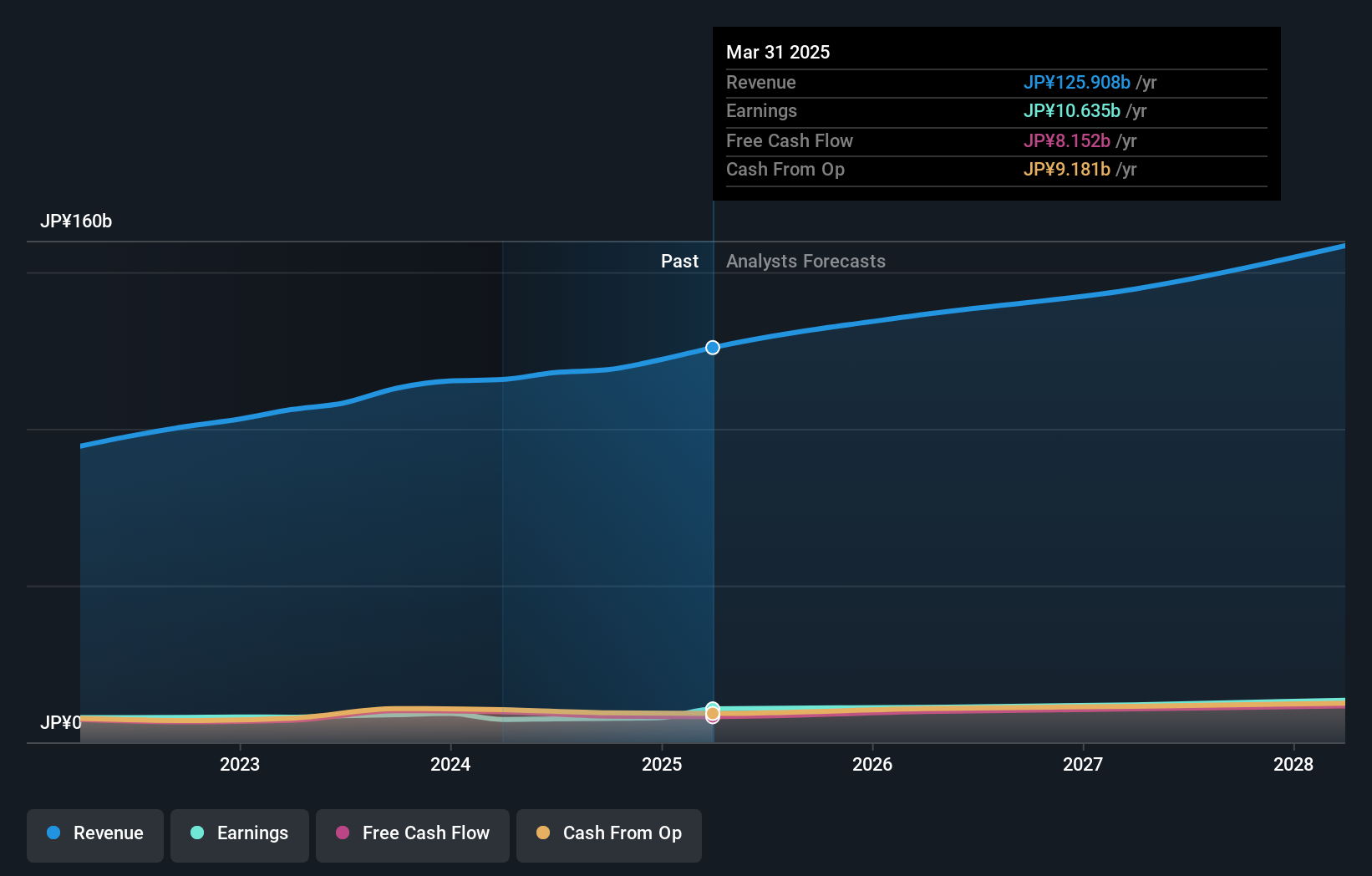

DTS (TSE:9682)

Simply Wall St Value Rating: ★★★★★★

Overview: DTS Corporation is a Japanese company specializing in systems integration services with a market capitalization of ¥183.96 billion.

Operations: The company generates revenue primarily through its systems integration services. It has a market capitalization of ¥183.96 billion.

DTS, a small but promising player in the IT sector, has been making strategic moves with a focus on innovation and shareholder value. The company reported impressive earnings growth of 45.8% over the past year, outpacing the industry average of 10.8%. Trading at 10.2% below its fair value estimate, DTS offers good relative value compared to peers. A recent share repurchase plan aims to buy back 750,000 shares for ¥2.5 billion by July 2025, enhancing capital efficiency and shareholder returns. Organizational changes emphasize generative AI initiatives and global business expansion to drive future growth opportunities.

Taking Advantage

- Unlock our comprehensive list of 2704 Asian Undiscovered Gems With Strong Fundamentals by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:9682

Very undervalued with flawless balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor