Advertisement

- China

- /

- Electrical

- /

- SZSE:300444

Spotlight On DBAPPSecurity And Two Other High Growth Insider Picks

Simply Wall St

Reviewed by Simply Wall St

As global markets continue to reach record highs, driven by a mix of domestic policy decisions and geopolitical developments, investors are increasingly looking for opportunities in high-growth companies with significant insider ownership. In this context, understanding the potential of stocks like DBAPPSecurity and others becomes crucial as insider ownership often signals confidence in a company's future prospects amidst fluctuating market conditions.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.9% | 39.9% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 37.3% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 26.3% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.3% |

| SKS Technologies Group (ASX:SKS) | 32.4% | 24.8% |

| Medley (TSE:4480) | 34% | 31.7% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 131.1% |

| Fulin Precision (SZSE:300432) | 13.6% | 66.7% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 110.9% |

| Findi (ASX:FND) | 34.8% | 112.9% |

Let's take a closer look at a couple of our picks from the screened companies.

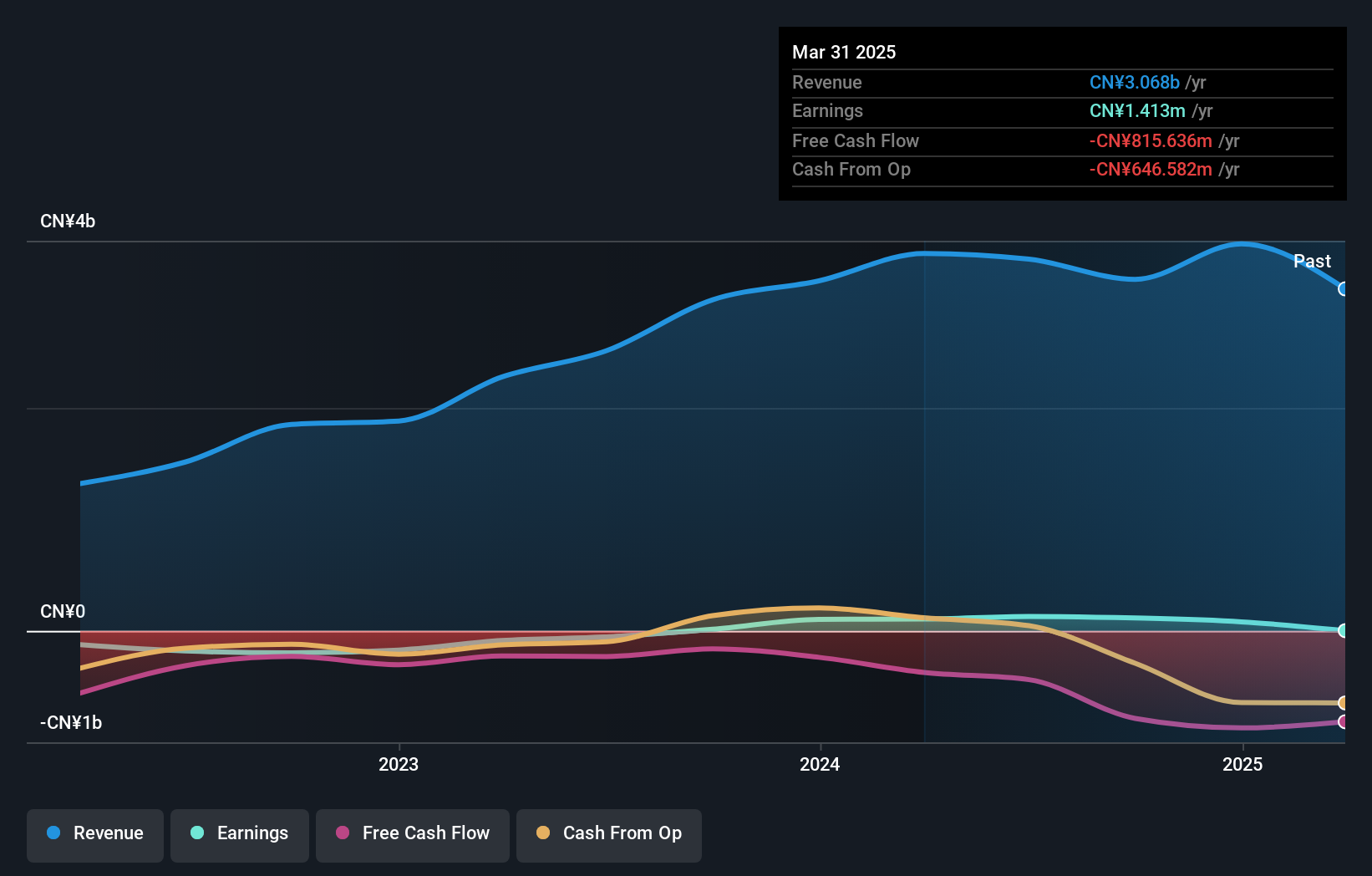

DBAPPSecurity (SHSE:688023)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: DBAPPSecurity Co., Ltd. is involved in the research, development, manufacture, and sale of cybersecurity products in China, with a market cap of CN¥5.40 billion.

Operations: DBAPPSecurity Co., Ltd. generates revenue through its focus on cybersecurity product research, development, manufacturing, and sales within the Chinese market.

Insider Ownership: 16.9%

Revenue Growth Forecast: 18.2% p.a.

DBAPPSecurity is trading at a significant discount to its estimated fair value, suggesting potential for growth. Despite recent revenue decline to CNY 1.14 billion from CNY 1.21 billion, the company reduced net loss from CNY 535.53 million to CNY 336 million over nine months ending September 2024. Earnings are forecasted to grow substantially at nearly 70% annually, with profitability expected within three years, surpassing average market growth expectations despite low future return on equity projections.

- Take a closer look at DBAPPSecurity's potential here in our earnings growth report.

- Our valuation report here indicates DBAPPSecurity may be undervalued.

Shenzhen Genvict Technologies (SZSE:002869)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen Genvict Technologies Co., Ltd. and its subsidiaries focus on the research, development, and industrialization of smart transportation technology in China, with a market cap of approximately CN¥5.38 billion.

Operations: The company generates revenue from the Intelligent Traffic Industry segment, amounting to CN¥514.77 million.

Insider Ownership: 20.6%

Revenue Growth Forecast: 34.9% p.a.

Shenzhen Genvict Technologies reported modest revenue growth to CNY 352.44 million for the nine months ending September 2024, with net income increasing to CNY 31.09 million. Earnings per share improved from the previous year, reflecting positive financial performance. The company's earnings are forecasted to grow significantly at over 40% annually, outpacing the Chinese market average of 26%. Despite this growth potential, future return on equity is expected to remain low at around 5.7%.

- Click to explore a detailed breakdown of our findings in Shenzhen Genvict Technologies' earnings growth report.

- Our comprehensive valuation report raises the possibility that Shenzhen Genvict Technologies is priced higher than what may be justified by its financials.

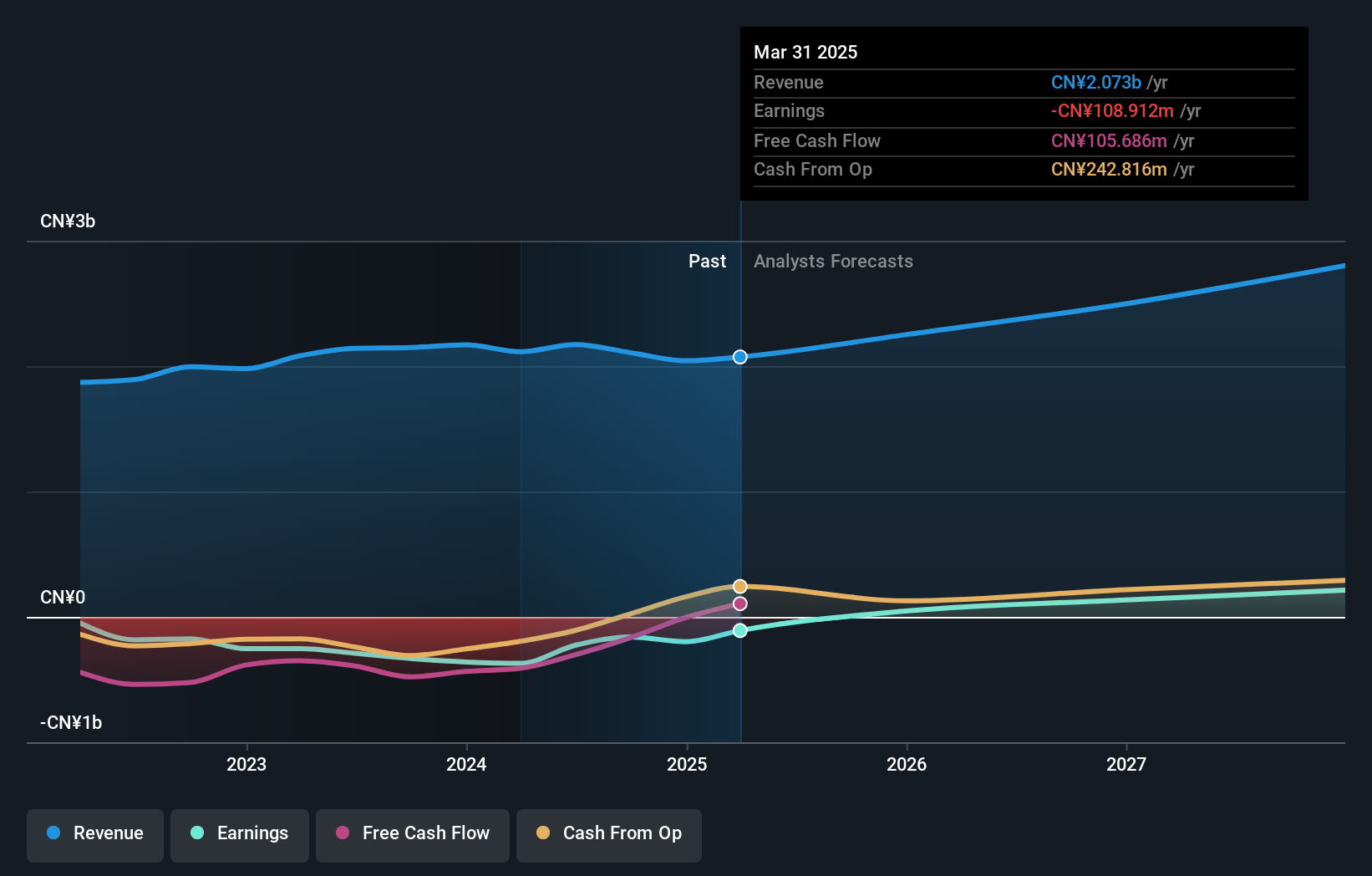

Beijing SOJO Electric (SZSE:300444)

Simply Wall St Growth Rating: ★★★★★★

Overview: Beijing SOJO Electric Co., Ltd. specializes in the research, production, export, and sale of power distribution and automation equipment for power transmission and distribution networks, with a market cap of CN¥6.42 billion.

Operations: Beijing SOJO Electric Co., Ltd. generates revenue through its involvement in the research, production, export, and sale of power distribution and automation equipment for transmission and distribution networks.

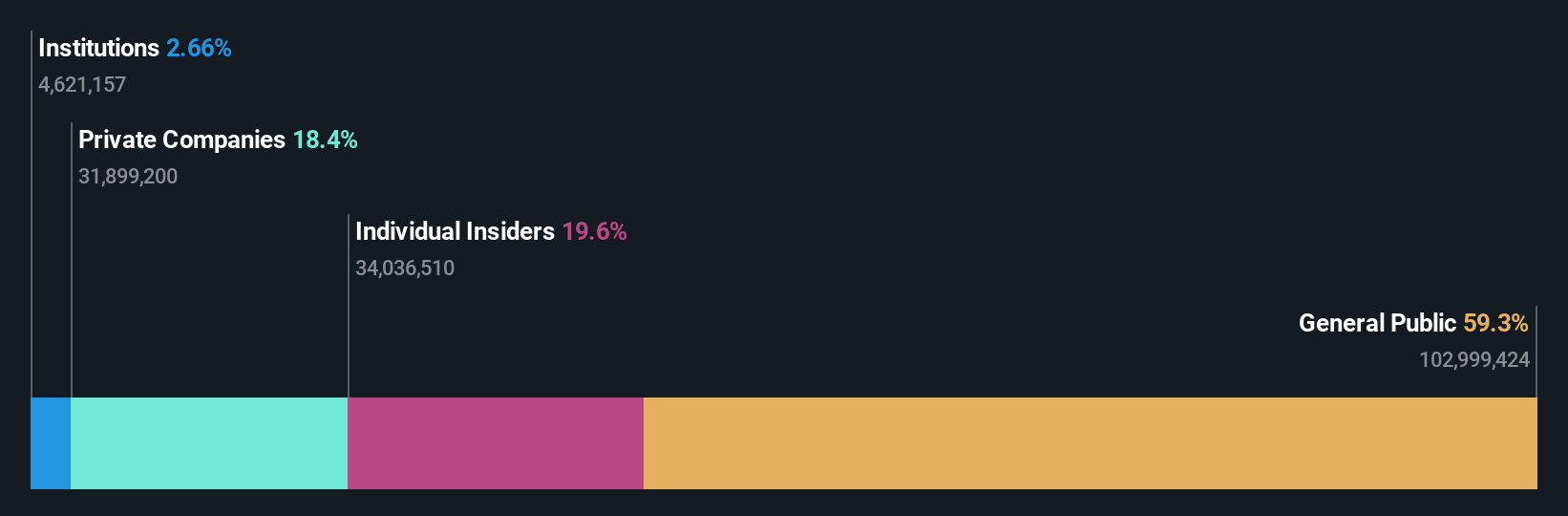

Insider Ownership: 38%

Revenue Growth Forecast: 26% p.a.

Beijing SOJO Electric's recent earnings report shows a steady increase in net income to CNY 116.25 million for the nine months ending September 2024, with revenue reaching CNY 2.56 billion. The company's earnings and revenue are forecasted to grow significantly, outpacing the Chinese market averages with expected annual growth rates of over 46% and 26%, respectively. Despite these promising forecasts, the company's debt coverage by operating cash flow remains a concern.

- Click here to discover the nuances of Beijing SOJO Electric with our detailed analytical future growth report.

- Our expertly prepared valuation report Beijing SOJO Electric implies its share price may be too high.

Seize The Opportunity

- Get an in-depth perspective on all 1512 Fast Growing Companies With High Insider Ownership by using our screener here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Beijing SOJO Electric might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300444

Beijing SOJO Electric

Engages in the research, production, export, and sale of power distribution equipment and automation equipment in the field of power transmission and distribution networks.

Mediocre balance sheet low.

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|59.6% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|20.8% undervalued

ZW

Community Contributor