Advertisement

- China

- /

- Life Sciences

- /

- SZSE:301096

February 2025's Top Growth Companies With Strong Insider Ownership

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate the complexities of tariff uncertainties and fluctuating economic indicators, investors are keenly observing how these factors impact growth trajectories. With major indexes experiencing slight declines amid trade policy tensions, attention turns to companies that not only exhibit robust growth potential but also demonstrate strong insider ownership—a factor often seen as a vote of confidence in a company's future prospects.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 17.3% | 22.8% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 26.2% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| CD Projekt (WSE:CDR) | 29.7% | 39.4% |

| Pharma Mar (BME:PHM) | 11.9% | 44.7% |

| Medley (TSE:4480) | 34.1% | 27.3% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| Findi (ASX:FND) | 35.8% | 111.4% |

Underneath we present a selection of stocks filtered out by our screen.

3onedata (SHSE:688618)

Simply Wall St Growth Rating: ★★★★★☆

Overview: 3onedata Co., Ltd. offers industrial communication solutions and services globally, with a market cap of CN¥2.61 billion.

Operations: The company's revenue segments are not provided in the text.

Insider Ownership: 20.8%

Revenue Growth Forecast: 28.5% p.a.

3onedata is poised for significant growth, with earnings projected to rise 38.18% annually over the next three years, outpacing the Chinese market's 25.5%. Despite a decline in profit margins from last year, it trades at a substantial discount to its estimated fair value. Revenue growth is expected at 28.5% per year, surpassing market averages. No recent insider trading activity has been reported ahead of an upcoming shareholders meeting on January 23, 2025.

- Navigate through the intricacies of 3onedata with our comprehensive analyst estimates report here.

- Our comprehensive valuation report raises the possibility that 3onedata is priced lower than what may be justified by its financials.

Jiangsu Huahong Technology (SZSE:002645)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jiangsu Huahong Technology Co., Ltd. is involved in the R&D, manufacturing, marketing, and servicing of renewable resource processing equipment both in China and internationally, with a market cap of CN¥4.03 billion.

Operations: Jiangsu Huahong Technology Co., Ltd.'s revenue primarily stems from its activities in the research, development, manufacturing, marketing, and servicing of equipment for processing renewable resources both domestically and abroad.

Insider Ownership: 18.7%

Revenue Growth Forecast: 23% p.a.

Jiangsu Huahong Technology is forecasted to experience robust growth, with revenue expected to increase by 23% annually, surpassing the Chinese market's average. Earnings are projected to grow significantly at 88.7% per year, with profitability anticipated within three years. The company trades at a favorable valuation relative to peers despite its recent removal from the S&P Global BMI Index. There is no recent insider trading activity reported over the past three months.

- Delve into the full analysis future growth report here for a deeper understanding of Jiangsu Huahong Technology.

- Our valuation report unveils the possibility Jiangsu Huahong Technology's shares may be trading at a discount.

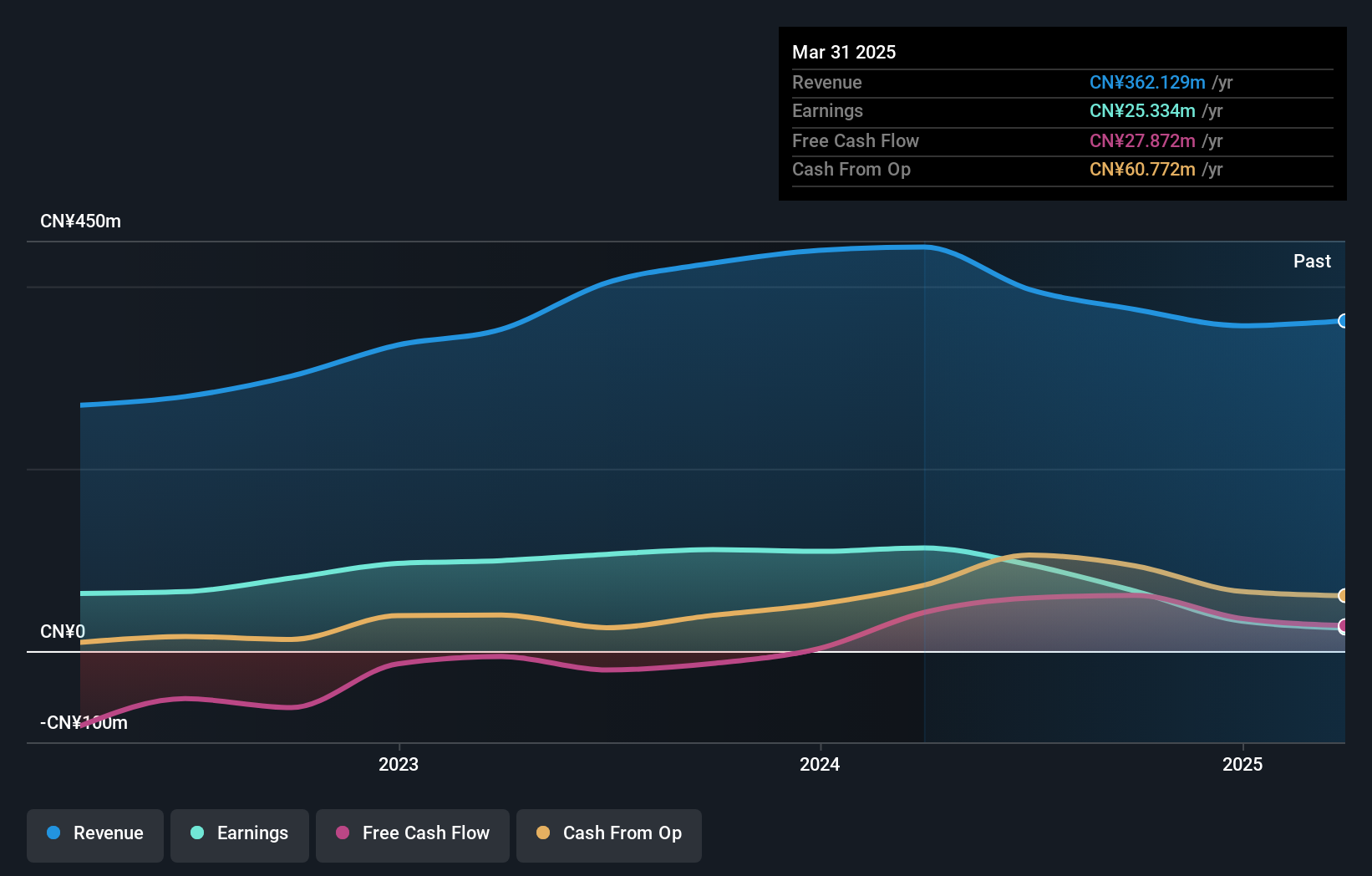

Hangzhou Bio-Sincerity Pharma-TechLtd (SZSE:301096)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Hangzhou Bio-Sincerity Pharma-Tech Co., Ltd. operates in the pharmaceutical industry and has a market cap of CN¥4.03 billion.

Operations: The company generates revenue from its biotechnology segment, amounting to CN¥1.03 billion.

Insider Ownership: 35%

Revenue Growth Forecast: 22.8% p.a.

Hangzhou Bio-Sincerity Pharma-Tech is poised for significant growth, with earnings projected to increase by 30.6% annually, outpacing the Chinese market average. Revenue is expected to grow at 22.8% per year, also exceeding market rates. The company trades at a favorable price-to-earnings ratio of 18.8x compared to the CN market's 36.7x, suggesting good relative value despite a low future return on equity forecast of 12.1%. Recent board changes include new director elections approved in February 2025.

- Take a closer look at Hangzhou Bio-Sincerity Pharma-TechLtd's potential here in our earnings growth report.

- The valuation report we've compiled suggests that Hangzhou Bio-Sincerity Pharma-TechLtd's current price could be quite moderate.

Turning Ideas Into Actions

- Click through to start exploring the rest of the 1438 Fast Growing Companies With High Insider Ownership now.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Hangzhou Bio-Sincerity Pharma-TechLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:301096

Hangzhou Bio-Sincerity Pharma-TechLtd

Hangzhou Bio-Sincerity Pharma-Tech Co.,Ltd.

Moderate growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor