- China

- /

- Communications

- /

- SHSE:603496

EmbedWay Technologies (Shanghai) Corporation's (SHSE:603496) Price In Tune With Revenues

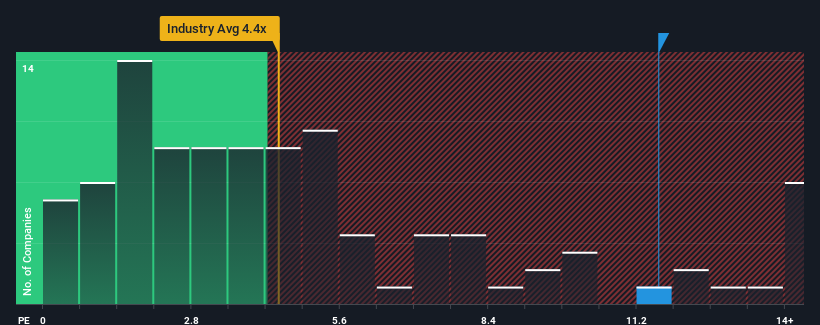

With a price-to-sales (or "P/S") ratio of 11.6x EmbedWay Technologies (Shanghai) Corporation (SHSE:603496) may be sending very bearish signals at the moment, given that almost half of all the Communications companies in China have P/S ratios under 4.4x and even P/S lower than 2x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

View our latest analysis for EmbedWay Technologies (Shanghai)

How EmbedWay Technologies (Shanghai) Has Been Performing

Recent revenue growth for EmbedWay Technologies (Shanghai) has been in line with the industry. It might be that many expect the mediocre revenue performance to strengthen positively, which has kept the P/S ratio from falling. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think EmbedWay Technologies (Shanghai)'s future stacks up against the industry? In that case, our free report is a great place to start.Is There Enough Revenue Growth Forecasted For EmbedWay Technologies (Shanghai)?

The only time you'd be truly comfortable seeing a P/S as steep as EmbedWay Technologies (Shanghai)'s is when the company's growth is on track to outshine the industry decidedly.

Taking a look back first, we see that there was hardly any revenue growth to speak of for the company over the past year. Although pleasingly revenue has lifted 45% in aggregate from three years ago, notwithstanding the last 12 months. So while the company has done a solid job in the past, it's somewhat concerning to see revenue growth decline as much as it has.

Looking ahead now, revenue is anticipated to climb by 77% during the coming year according to the three analysts following the company. With the industry only predicted to deliver 49%, the company is positioned for a stronger revenue result.

In light of this, it's understandable that EmbedWay Technologies (Shanghai)'s P/S sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Key Takeaway

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of EmbedWay Technologies (Shanghai)'s analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless these conditions change, they will continue to provide strong support to the share price.

You always need to take note of risks, for example - EmbedWay Technologies (Shanghai) has 1 warning sign we think you should be aware of.

If you're unsure about the strength of EmbedWay Technologies (Shanghai)'s business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if EmbedWay Technologies (Shanghai) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603496

EmbedWay Technologies (Shanghai)

Engages in the provision of network visibility, intelligent system platforms, and intelligent computing solutions and services in China.

High growth potential with adequate balance sheet.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Q3 Outlook modestly optimistic

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion