Advertisement

In a week marked by geopolitical tensions and consumer spending concerns, global markets experienced volatility, with major indices like the S&P 500 initially reaching record highs before retreating. Amidst this backdrop of uncertainty, growth companies with high insider ownership stand out as potentially resilient investments due to the confidence insiders demonstrate in their long-term prospects.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 17.3% | 22.8% |

| Propel Holdings (TSX:PRL) | 36.5% | 38.7% |

| Pricol (NSEI:PRICOLLTD) | 25.4% | 25.2% |

| CD Projekt (WSE:CDR) | 29.7% | 39.4% |

| On Holding (NYSE:ONON) | 19.1% | 29.8% |

| Pharma Mar (BME:PHM) | 11.9% | 45.4% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| Findi (ASX:FND) | 35.8% | 133.7% |

Let's review some notable picks from our screened stocks.

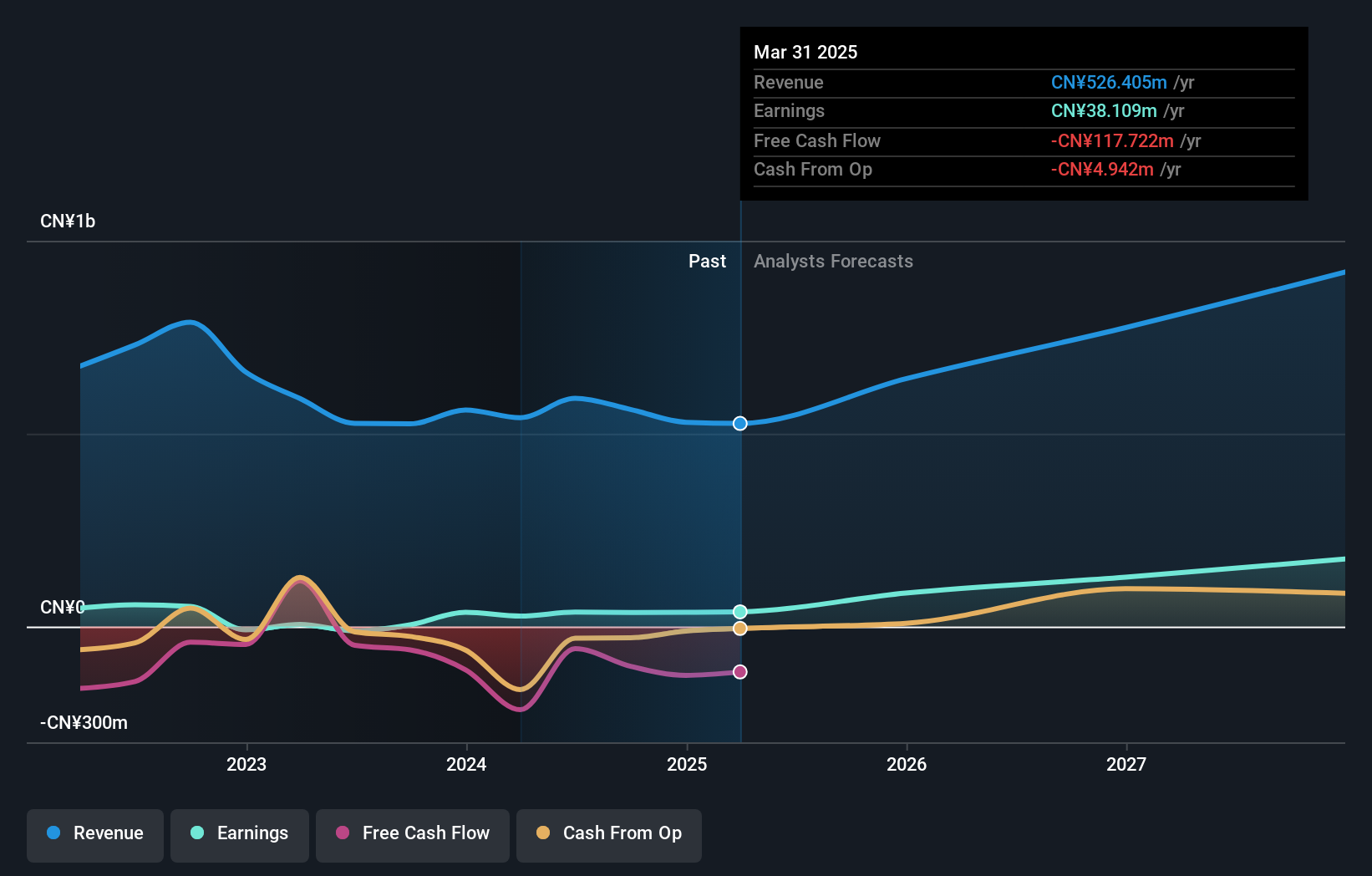

Koal Software (SHSE:603232)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Koal Software Co., Ltd. develops public key infrastructure platforms in China and has a market cap of CN¥3.54 billion.

Operations: Koal Software Co., Ltd. generates revenue through its development of public key infrastructure platforms in China.

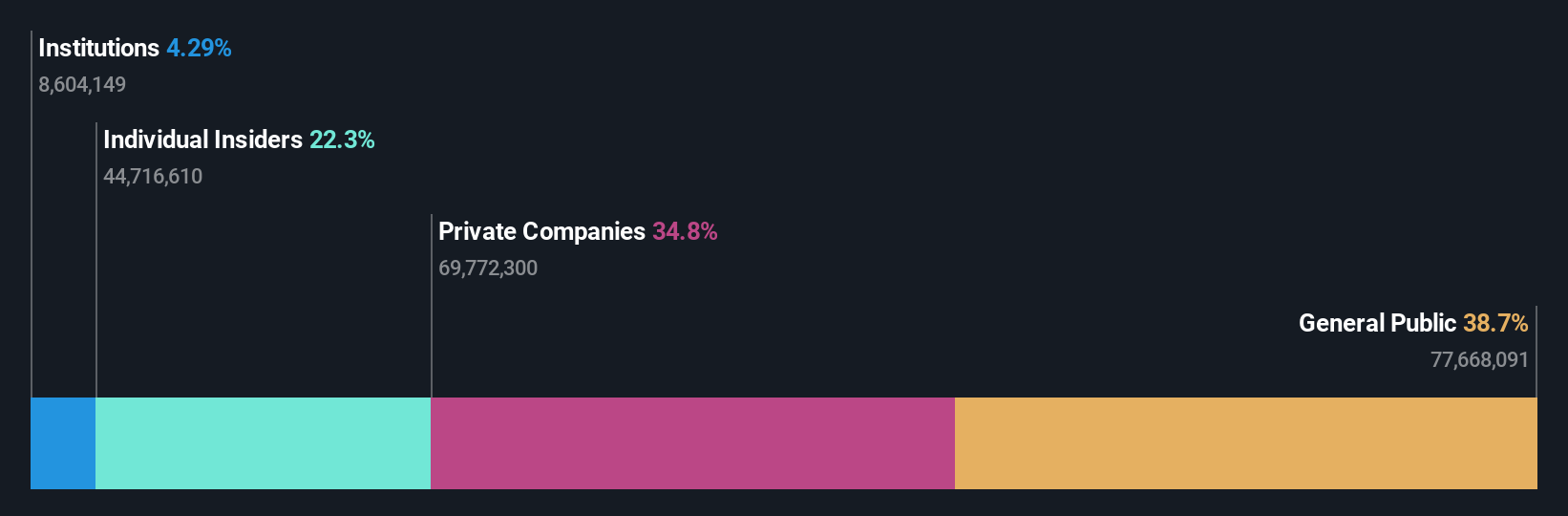

Insider Ownership: 30.7%

Revenue Growth Forecast: 19.5% p.a.

Koal Software shows potential with a Price-To-Earnings ratio of 96.9x, slightly below the industry average, suggesting reasonable valuation. Despite volatile share prices and large one-off items affecting earnings quality, its earnings are forecast to grow significantly at 45.6% annually, outpacing the market's 25.3%. Revenue growth is expected at 19.5% per year, surpassing the market's 13.4%. No substantial insider trading activity was reported in recent months.

- Unlock comprehensive insights into our analysis of Koal Software stock in this growth report.

- Our valuation report here indicates Koal Software may be overvalued.

Shanghai Taisheng Wind Power Equipment (SZSE:300129)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shanghai Taisheng Wind Power Equipment Co., Ltd. operates in the renewable energy sector, focusing on the production and supply of wind power equipment, with a market cap of CN¥6.66 billion.

Operations: Shanghai Taisheng Wind Power Equipment Co., Ltd. generates revenue primarily through the production and supply of equipment for the wind power industry.

Insider Ownership: 10.7%

Revenue Growth Forecast: 24.2% p.a.

Shanghai Taisheng Wind Power Equipment is positioned for growth with forecasted earnings expansion of 46.4% annually, surpassing the broader Chinese market's 25.3%. Revenue is expected to grow at 24.2% per year, outpacing market averages. Despite a decline in profit margins from last year, its Price-To-Earnings ratio of 32.6x suggests good valuation relative to peers. Recent changes in company bylaws indicate strategic shifts, though no significant insider trading activity has been noted recently.

- Click here to discover the nuances of Shanghai Taisheng Wind Power Equipment with our detailed analytical future growth report.

- The valuation report we've compiled suggests that Shanghai Taisheng Wind Power Equipment's current price could be quite moderate.

Hunan Sundy Science and Technology (SZSE:300515)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Hunan Sundy Science and Technology Co., Ltd provides coal analysis solutions both in the People’s Republic of China and internationally, with a market cap of CN¥3.26 billion.

Operations: The company's revenue is primarily derived from the Instrumentation Industry segment, which generated CN¥483.69 million.

Insider Ownership: 23.3%

Revenue Growth Forecast: 28.0% p.a.

Hunan Sundy Science and Technology is set for robust growth with earnings projected to rise 34.3% annually, outpacing the Chinese market's 25.3%. Revenue is anticipated to increase by 28% yearly, exceeding both industry and market averages. The company's P/E ratio of 40.4x indicates attractive valuation compared to its peers in the electronics sector. Recent board changes suggest strategic direction adjustments, while insider trading activity remains stable with no significant movements reported recently.

- Get an in-depth perspective on Hunan Sundy Science and Technology's performance by reading our analyst estimates report here.

- In light of our recent valuation report, it seems possible that Hunan Sundy Science and Technology is trading beyond its estimated value.

Where To Now?

- Embark on your investment journey to our 1450 Fast Growing Companies With High Insider Ownership selection here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Koal Software might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603232

High growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor