Advertisement

- China

- /

- Semiconductors

- /

- SZSE:300776

Why We're Not Concerned About Wuhan DR Laser Technology Corp.,Ltd's (SZSE:300776) Share Price

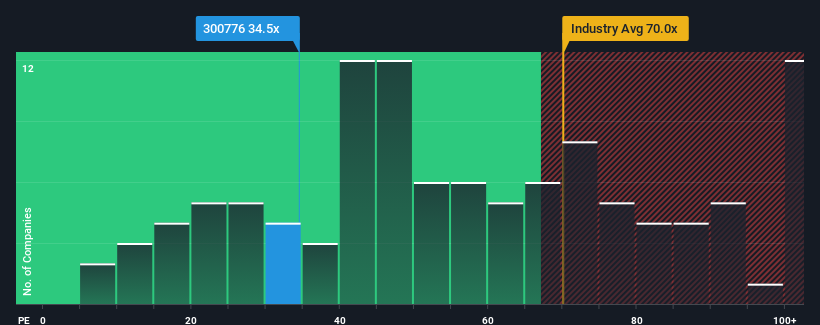

With a median price-to-earnings (or "P/E") ratio of close to 38x in China, you could be forgiven for feeling indifferent about Wuhan DR Laser Technology Corp.,Ltd's (SZSE:300776) P/E ratio of 34.5x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

Recent times have been pleasing for Wuhan DR Laser TechnologyLtd as its earnings have risen in spite of the market's earnings going into reverse. One possibility is that the P/E is moderate because investors think the company's earnings will be less resilient moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

View our latest analysis for Wuhan DR Laser TechnologyLtd

Does Growth Match The P/E?

There's an inherent assumption that a company should be matching the market for P/E ratios like Wuhan DR Laser TechnologyLtd's to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 23%. EPS has also lifted 27% in aggregate from three years ago, mostly thanks to the last 12 months of growth. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Shifting to the future, estimates from the seven analysts covering the company suggest earnings should grow by 35% over the next year. That's shaping up to be similar to the 37% growth forecast for the broader market.

With this information, we can see why Wuhan DR Laser TechnologyLtd is trading at a fairly similar P/E to the market. It seems most investors are expecting to see average future growth and are only willing to pay a moderate amount for the stock.

The Bottom Line On Wuhan DR Laser TechnologyLtd's P/E

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Wuhan DR Laser TechnologyLtd maintains its moderate P/E off the back of its forecast growth being in line with the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings won't throw up any surprises. It's hard to see the share price moving strongly in either direction in the near future under these circumstances.

Plus, you should also learn about this 1 warning sign we've spotted with Wuhan DR Laser TechnologyLtd.

If these risks are making you reconsider your opinion on Wuhan DR Laser TechnologyLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Wuhan DR Laser TechnologyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300776

Wuhan DR Laser TechnologyLtd

Provides precision laser processing solutions in China.

Proven track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor