Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688766

Optimistic Investors Push Puya Semiconductor (Shanghai) Co., Ltd. (SHSE:688766) Shares Up 40% But Growth Is Lacking

Despite an already strong run, Puya Semiconductor (Shanghai) Co., Ltd. (SHSE:688766) shares have been powering on, with a gain of 40% in the last thirty days. Looking back a bit further, it's encouraging to see the stock is up 55% in the last year.

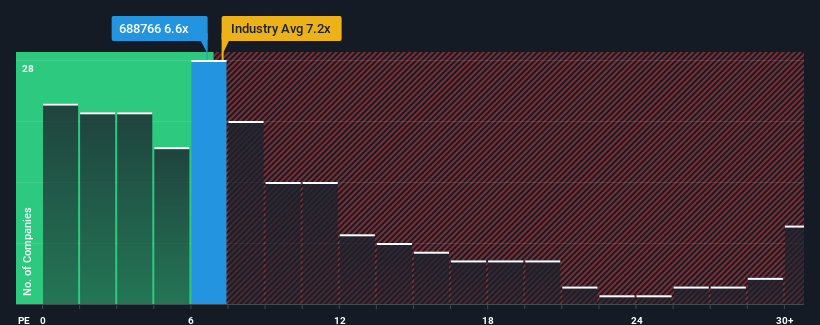

Even after such a large jump in price, there still wouldn't be many who think Puya Semiconductor (Shanghai)'s price-to-sales (or "P/S") ratio of 6.6x is worth a mention when the median P/S in China's Semiconductor industry is similar at about 7.2x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for Puya Semiconductor (Shanghai)

What Does Puya Semiconductor (Shanghai)'s Recent Performance Look Like?

Puya Semiconductor (Shanghai) certainly has been doing a good job lately as it's been growing revenue more than most other companies. Perhaps the market is expecting this level of performance to taper off, keeping the P/S from soaring. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Puya Semiconductor (Shanghai) will help you uncover what's on the horizon.Do Revenue Forecasts Match The P/S Ratio?

In order to justify its P/S ratio, Puya Semiconductor (Shanghai) would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered an exceptional 86% gain to the company's top line. The latest three year period has also seen an excellent 60% overall rise in revenue, aided by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 31% during the coming year according to the four analysts following the company. With the industry predicted to deliver 49% growth, the company is positioned for a weaker revenue result.

In light of this, it's curious that Puya Semiconductor (Shanghai)'s P/S sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

The Key Takeaway

Puya Semiconductor (Shanghai) appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Given that Puya Semiconductor (Shanghai)'s revenue growth projections are relatively subdued in comparison to the wider industry, it comes as a surprise to see it trading at its current P/S ratio. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Before you take the next step, you should know about the 2 warning signs for Puya Semiconductor (Shanghai) that we have uncovered.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688766

Puya Semiconductor (Shanghai)

Engages in research, development, design, and sale of non-volatile memory chips and memory based derivative chips in China and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor