Advertisement

As global markets navigate a landscape marked by fluctuating corporate earnings and competitive pressures from emerging AI technologies, investors are closely watching central bank policies and inflation trends. In this environment, identifying growth companies with substantial insider ownership can be advantageous, as it may signal confidence in the company's potential despite broader market volatility.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 17.3% | 22.8% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Propel Holdings (TSX:PRL) | 36.5% | 38.9% |

| On Holding (NYSE:ONON) | 19.1% | 29.7% |

| Pharma Mar (BME:PHM) | 11.9% | 44.7% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| Brightstar Resources (ASX:BTR) | 16.2% | 86% |

| Findi (ASX:FND) | 35.8% | 110.7% |

Let's review some notable picks from our screened stocks.

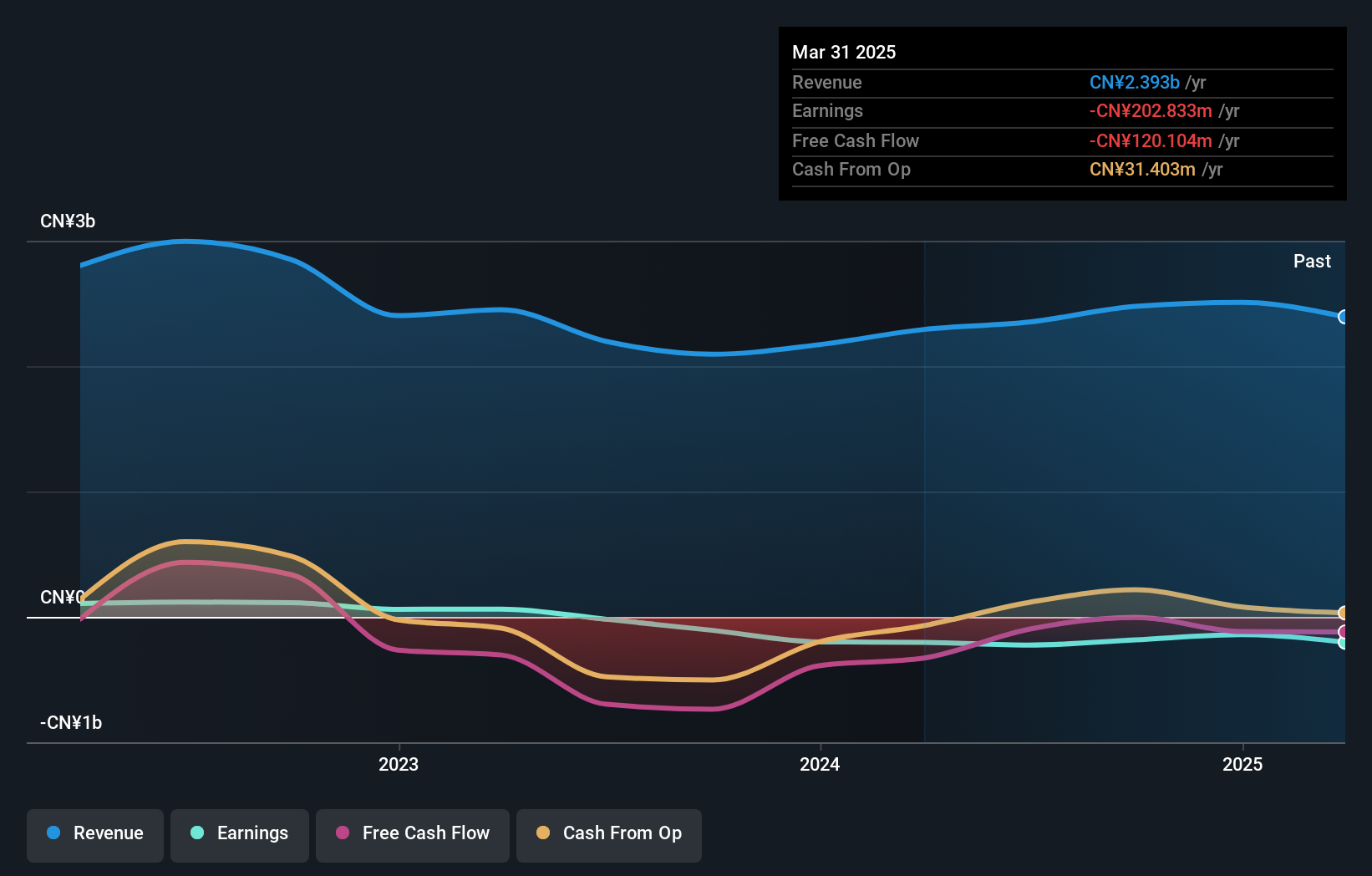

Unionman TechnologyLtd (SHSE:688609)

Simply Wall St Growth Rating: ★★★★★★

Overview: Unionman Technology Co., Ltd. engages in the production, sale, and servicing of multimedia information terminals, smart home network communication equipment, IoT communication modules, optical communication modules, smart security equipment, and related software systems and platforms with a market cap of approximately CN¥4.76 billion.

Operations: Unionman Technology Co., Ltd.'s revenue primarily comes from the Computer, Communications and Other Electronic Intelligent Equipment Manufacturing Industry, amounting to CN¥2.48 billion.

Insider Ownership: 32.4%

Earnings Growth Forecast: 88.3% p.a.

Unionman Technology Ltd. is trading at a good value compared to peers, with revenue expected to grow 34.4% annually, surpassing the Chinese market average of 13.3%. Earnings are forecasted to increase by 88.3% per year, and the company is anticipated to become profitable within three years, reflecting above-average market growth. However, its debt isn't well-covered by operating cash flow. Recent events include an upcoming shareholders meeting on December 25, 2024.

- Unlock comprehensive insights into our analysis of Unionman TechnologyLtd stock in this growth report.

- According our valuation report, there's an indication that Unionman TechnologyLtd's share price might be on the cheaper side.

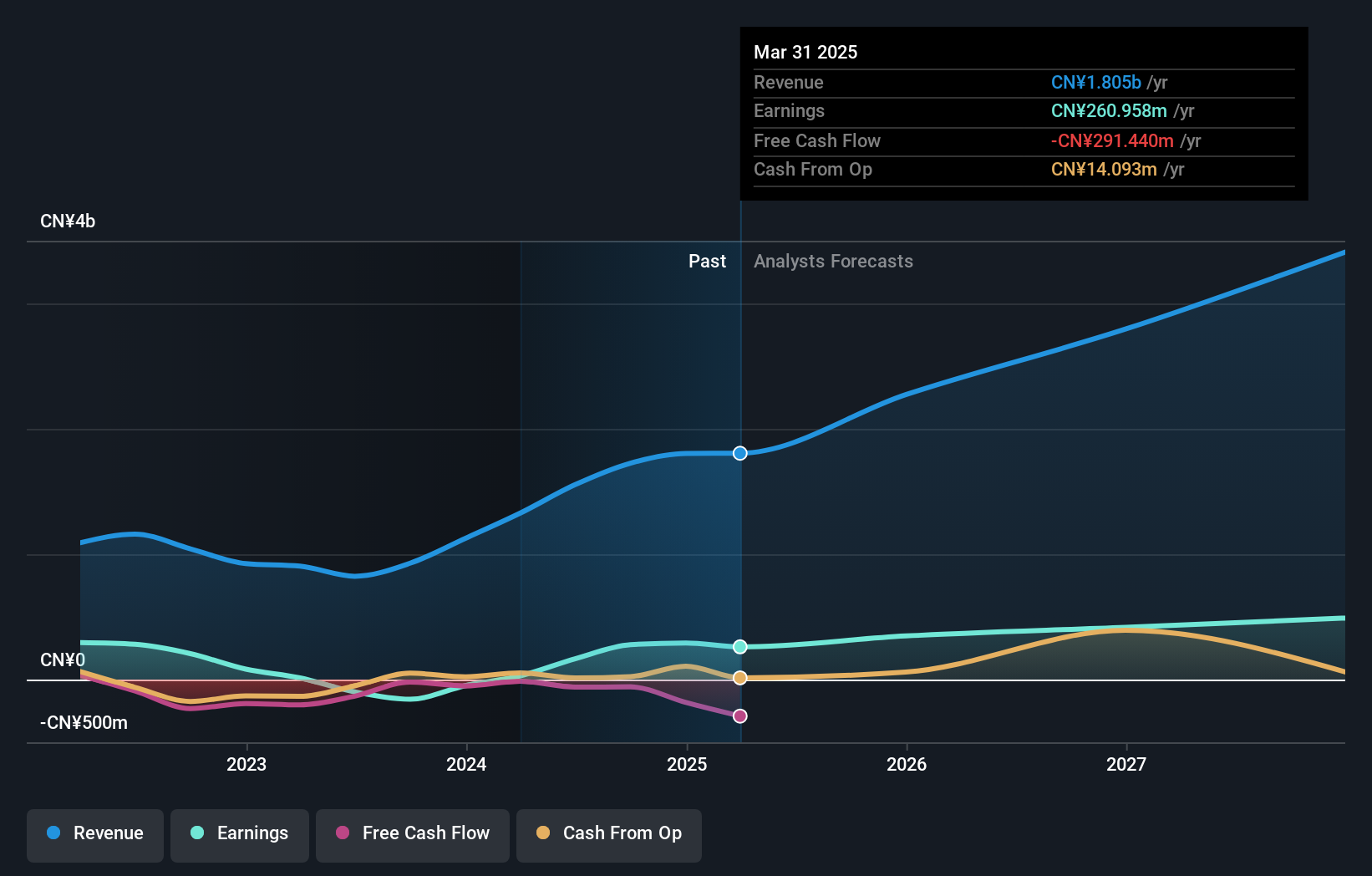

Puya Semiconductor (Shanghai) (SHSE:688766)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Puya Semiconductor (Shanghai) Co., Ltd. designs and sells non-volatile memory chips and derivative chips based on memory chips both in China and internationally, with a market cap of CN¥11.39 billion.

Operations: The company generates revenue from its Integrated Circuit segment, amounting to CN¥1.73 billion.

Insider Ownership: 23.8%

Earnings Growth Forecast: 24.4% p.a.

Puya Semiconductor (Shanghai) is trading at a favorable value with a Price-To-Earnings ratio of 41.7x, below the industry average of 63.7x. The company recently became profitable and its revenue is forecast to grow at 24.1% annually, outpacing the Chinese market's growth rate of 13.3%. Earnings are expected to rise by 24.38% per year, although this lags behind the broader market's anticipated growth rate of 25.1%.

- Click here and access our complete growth analysis report to understand the dynamics of Puya Semiconductor (Shanghai).

- The valuation report we've compiled suggests that Puya Semiconductor (Shanghai)'s current price could be quite moderate.

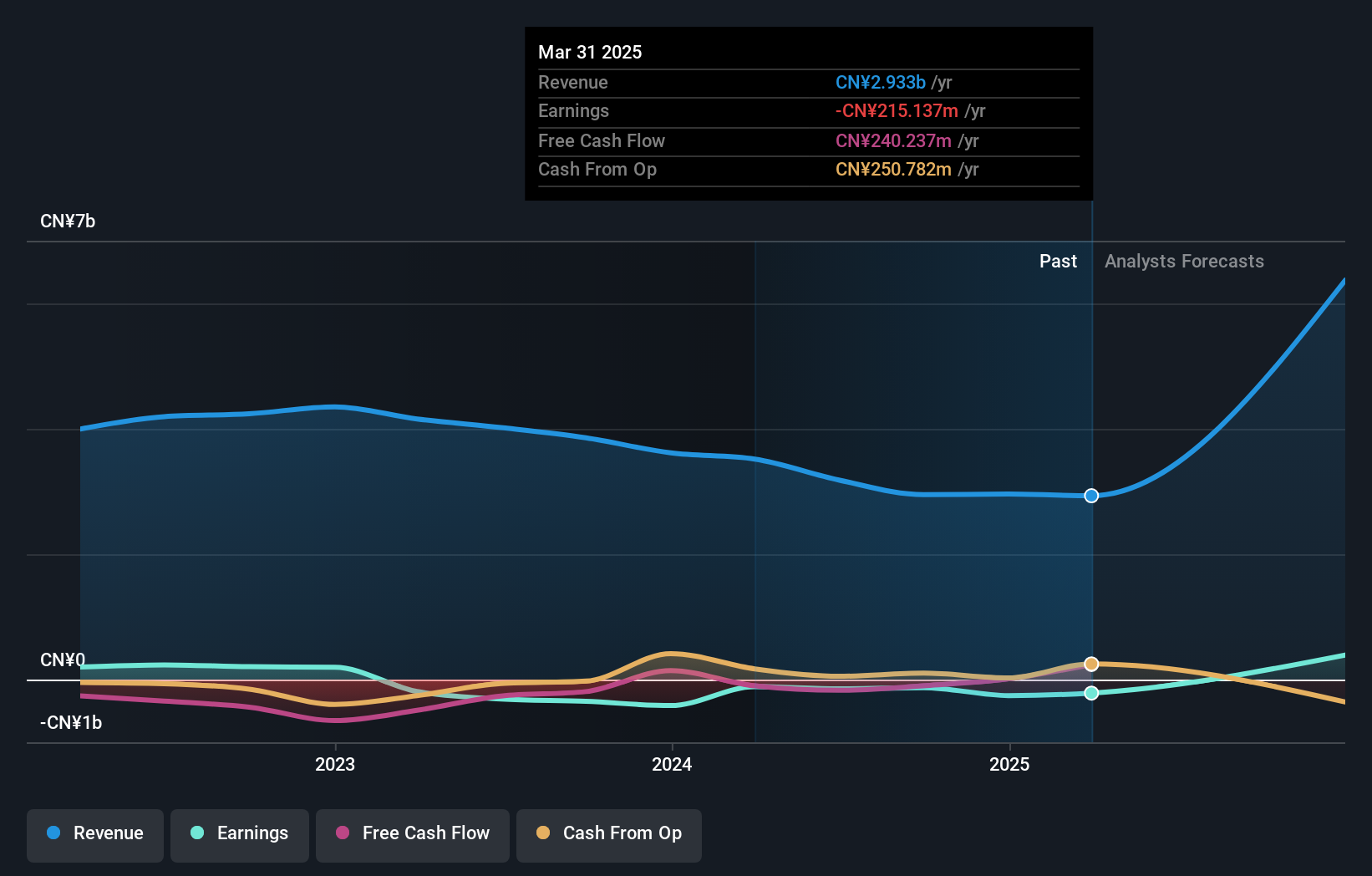

Miracle Automation EngineeringLtd (SZSE:002009)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Miracle Automation Engineering Co. Ltd offers intelligent equipment solutions and services both in China and internationally, with a market cap of CN¥5.47 billion.

Operations: Miracle Automation Engineering Co. Ltd generates revenue from its intelligent equipment solutions and services in both domestic and international markets.

Insider Ownership: 28.1%

Earnings Growth Forecast: 114.2% p.a.

Miracle Automation Engineering Ltd. is trading at a good value compared to its peers and industry, with earnings projected to grow significantly by 114.23% annually, indicating strong potential for profitability within three years. Revenue growth is expected at 47.3% per year, surpassing the Chinese market average of 13.3%. However, the company's debt coverage through operating cash flow remains inadequate and its share price has been highly volatile recently.

- Take a closer look at Miracle Automation EngineeringLtd's potential here in our earnings growth report.

- Our valuation report unveils the possibility Miracle Automation EngineeringLtd's shares may be trading at a discount.

Seize The Opportunity

- Dive into all 1478 of the Fast Growing Companies With High Insider Ownership we have identified here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002009

Miracle Automation EngineeringLtd

Provides intelligent equipment solutions and services in China and internationally.

Good value with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor