- China

- /

- Semiconductors

- /

- SHSE:688601

Returns At Wuxi ETEK MicroelectronicsLtd (SHSE:688601) Are On The Way Up

What trends should we look for it we want to identify stocks that can multiply in value over the long term? Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. So when we looked at Wuxi ETEK MicroelectronicsLtd (SHSE:688601) and its trend of ROCE, we really liked what we saw.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Wuxi ETEK MicroelectronicsLtd:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

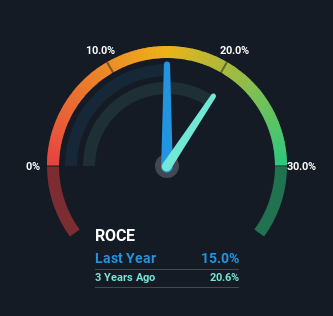

0.15 = CN¥208m ÷ (CN¥1.5b - CN¥97m) (Based on the trailing twelve months to March 2024).

Thus, Wuxi ETEK MicroelectronicsLtd has an ROCE of 15%. In absolute terms, that's a satisfactory return, but compared to the Semiconductor industry average of 3.9% it's much better.

View our latest analysis for Wuxi ETEK MicroelectronicsLtd

In the above chart we have measured Wuxi ETEK MicroelectronicsLtd's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free analyst report for Wuxi ETEK MicroelectronicsLtd .

So How Is Wuxi ETEK MicroelectronicsLtd's ROCE Trending?

Wuxi ETEK MicroelectronicsLtd is displaying some positive trends. The numbers show that in the last five years, the returns generated on capital employed have grown considerably to 15%. The company is effectively making more money per dollar of capital used, and it's worth noting that the amount of capital has increased too, by 435%. So we're very much inspired by what we're seeing at Wuxi ETEK MicroelectronicsLtd thanks to its ability to profitably reinvest capital.

On a related note, the company's ratio of current liabilities to total assets has decreased to 6.5%, which basically reduces it's funding from the likes of short-term creditors or suppliers. So shareholders would be pleased that the growth in returns has mostly come from underlying business performance.

In Conclusion...

In summary, it's great to see that Wuxi ETEK MicroelectronicsLtd can compound returns by consistently reinvesting capital at increasing rates of return, because these are some of the key ingredients of those highly sought after multi-baggers. Given the stock has declined 43% in the last three years, this could be a good investment if the valuation and other metrics are also appealing. That being the case, research into the company's current valuation metrics and future prospects seems fitting.

Like most companies, Wuxi ETEK MicroelectronicsLtd does come with some risks, and we've found 1 warning sign that you should be aware of.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Wuxi ETEK MicroelectronicsLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688601

Wuxi ETEK MicroelectronicsLtd

Engages in the research and development, manufacture, and sale of analog integrated circuits (ICs) in China and internationally.

High growth potential with adequate balance sheet.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion