Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688535

Jiangsu HHCK Advanced MaterialsLtd (SHSE:688535) Takes On Some Risk With Its Use Of Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Jiangsu HHCK Advanced Materials Co.,Ltd (SHSE:688535) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Jiangsu HHCK Advanced MaterialsLtd

How Much Debt Does Jiangsu HHCK Advanced MaterialsLtd Carry?

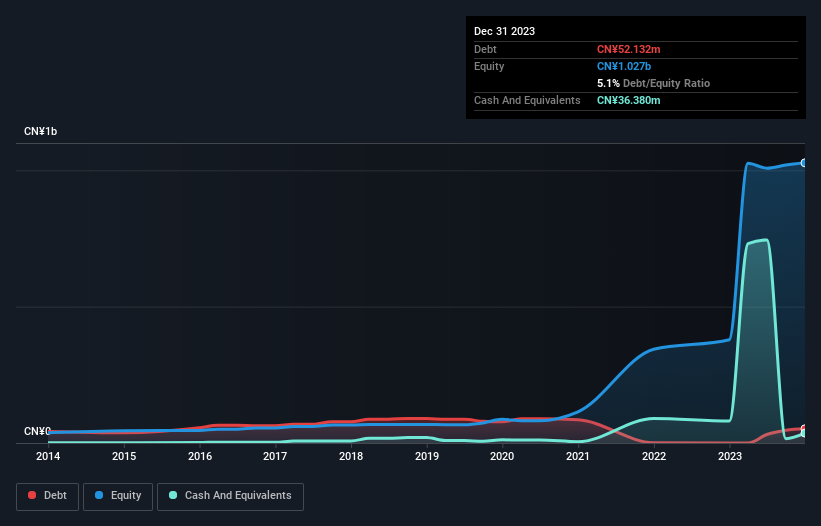

The image below, which you can click on for greater detail, shows that at December 2023 Jiangsu HHCK Advanced MaterialsLtd had debt of CN¥52.1m, up from none in one year. However, it also had CN¥36.4m in cash, and so its net debt is CN¥15.8m.

How Strong Is Jiangsu HHCK Advanced MaterialsLtd's Balance Sheet?

We can see from the most recent balance sheet that Jiangsu HHCK Advanced MaterialsLtd had liabilities of CN¥172.1m falling due within a year, and liabilities of CN¥31.1m due beyond that. Offsetting these obligations, it had cash of CN¥36.4m as well as receivables valued at CN¥191.4m due within 12 months. So it actually has CN¥24.6m more liquid assets than total liabilities.

This state of affairs indicates that Jiangsu HHCK Advanced MaterialsLtd's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the CN¥5.08b company is short on cash, but still worth keeping an eye on the balance sheet. Carrying virtually no net debt, Jiangsu HHCK Advanced MaterialsLtd has a very light debt load indeed.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Jiangsu HHCK Advanced MaterialsLtd has net debt of just 0.61 times EBITDA, suggesting it could ramp leverage without breaking a sweat. But the really cool thing is that it actually managed to receive more interest than it paid, over the last year. So it's fair to say it can handle debt like a hotshot teppanyaki chef handles cooking. The modesty of its debt load may become crucial for Jiangsu HHCK Advanced MaterialsLtd if management cannot prevent a repeat of the 60% cut to EBIT over the last year. When a company sees its earnings tank, it can sometimes find its relationships with its lenders turn sour. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Jiangsu HHCK Advanced MaterialsLtd can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Jiangsu HHCK Advanced MaterialsLtd burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Neither Jiangsu HHCK Advanced MaterialsLtd's ability to grow its EBIT nor its conversion of EBIT to free cash flow gave us confidence in its ability to take on more debt. But its interest cover tells a very different story, and suggests some resilience. Looking at all the angles mentioned above, it does seem to us that Jiangsu HHCK Advanced MaterialsLtd is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Jiangsu HHCK Advanced MaterialsLtd is showing 1 warning sign in our investment analysis , you should know about...

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688535

Jiangsu HHCK Advanced Materials

Jiangsu HHCK Advanced Materials Co., Ltd.

Adequate balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor