Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688516

Not Many Are Piling Into Wuxi Autowell Technology Co.,Ltd. (SHSE:688516) Stock Yet As It Plummets 26%

To the annoyance of some shareholders, Wuxi Autowell Technology Co.,Ltd. (SHSE:688516) shares are down a considerable 26% in the last month, which continues a horrid run for the company. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 49% share price drop.

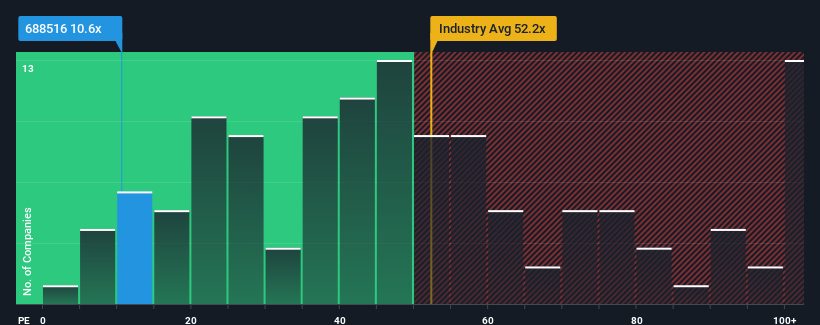

Since its price has dipped substantially, Wuxi Autowell TechnologyLtd may be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 10.6x, since almost half of all companies in China have P/E ratios greater than 30x and even P/E's higher than 57x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

Recent times have been advantageous for Wuxi Autowell TechnologyLtd as its earnings have been rising faster than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Check out our latest analysis for Wuxi Autowell TechnologyLtd

Is There Any Growth For Wuxi Autowell TechnologyLtd?

Wuxi Autowell TechnologyLtd's P/E ratio would be typical for a company that's expected to deliver very poor growth or even falling earnings, and importantly, perform much worse than the market.

If we review the last year of earnings growth, the company posted a terrific increase of 58%. The strong recent performance means it was also able to grow EPS by 519% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 29% per year during the coming three years according to the ten analysts following the company. That's shaping up to be materially higher than the 25% each year growth forecast for the broader market.

In light of this, it's peculiar that Wuxi Autowell TechnologyLtd's P/E sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Bottom Line On Wuxi Autowell TechnologyLtd's P/E

Wuxi Autowell TechnologyLtd's P/E looks about as weak as its stock price lately. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Wuxi Autowell TechnologyLtd currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. There could be some major unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

You need to take note of risks, for example - Wuxi Autowell TechnologyLtd has 2 warning signs (and 1 which shouldn't be ignored) we think you should know about.

You might be able to find a better investment than Wuxi Autowell TechnologyLtd. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Wuxi Autowell TechnologyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688516

Wuxi Autowell TechnologyLtd

Manufactures and sells automation equipment for photovoltaic equipment, lithium battery equipment, and semiconductor industries in China.

Excellent balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor