Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688512

We're Hopeful That Smarter Microelectronics (Guangzhou) (SHSE:688512) Will Use Its Cash Wisely

We can readily understand why investors are attracted to unprofitable companies. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

Given this risk, we thought we'd take a look at whether Smarter Microelectronics (Guangzhou) (SHSE:688512) shareholders should be worried about its cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. Let's start with an examination of the business' cash, relative to its cash burn.

View our latest analysis for Smarter Microelectronics (Guangzhou)

When Might Smarter Microelectronics (Guangzhou) Run Out Of Money?

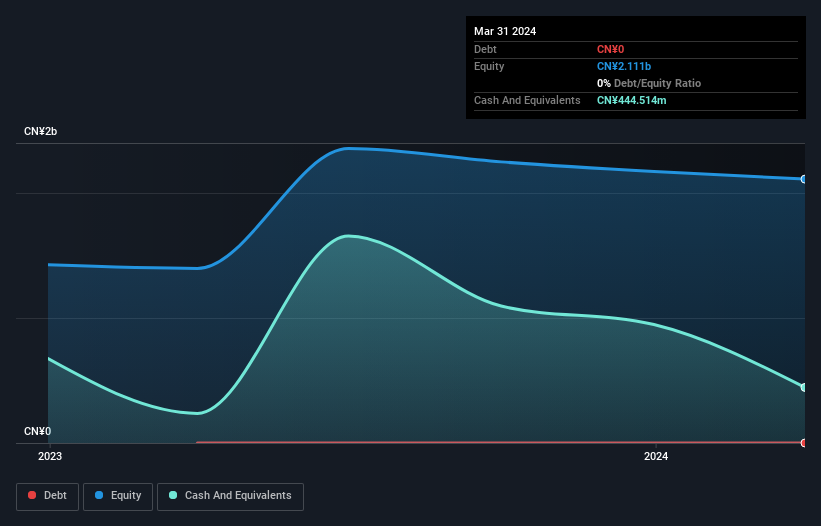

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at March 2024, Smarter Microelectronics (Guangzhou) had cash of CN¥445m and no debt. Looking at the last year, the company burnt through CN¥333m. So it had a cash runway of approximately 16 months from March 2024. That's not too bad, but it's fair to say the end of the cash runway is in sight, unless cash burn reduces drastically. The image below shows how its cash balance has been changing over the last few years.

How Well Is Smarter Microelectronics (Guangzhou) Growing?

Smarter Microelectronics (Guangzhou) reduced its cash burn by 9.8% during the last year, which points to some degree of discipline. On top of that, operating revenue was up 44%, making for a heartening combination We think it is growing rather well, upon reflection. Clearly, however, the crucial factor is whether the company will grow its business going forward. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Easily Can Smarter Microelectronics (Guangzhou) Raise Cash?

Smarter Microelectronics (Guangzhou) seems to be in a fairly good position, in terms of cash burn, but we still think it's worthwhile considering how easily it could raise more money if it wanted to. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Smarter Microelectronics (Guangzhou) has a market capitalisation of CN¥4.0b and burnt through CN¥333m last year, which is 8.4% of the company's market value. That's a low proportion, so we figure the company would be able to raise more cash to fund growth, with a little dilution, or even to simply borrow some money.

So, Should We Worry About Smarter Microelectronics (Guangzhou)'s Cash Burn?

The good news is that in our view Smarter Microelectronics (Guangzhou)'s cash burn situation gives shareholders real reason for optimism. One the one hand we have its solid cash burn relative to its market cap, while on the other it can also boast very strong revenue growth. Based on the factors mentioned in this article, we think its cash burn situation warrants some attention from shareholders, but we don't think they should be worried. Its important for readers to be cognizant of the risks that can affect the company's operations, and we've picked out 3 warning signs for Smarter Microelectronics (Guangzhou) that investors should know when investing in the stock.

Of course Smarter Microelectronics (Guangzhou) may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688512

Smarter Microelectronics (Guangzhou)

A chip design company, researches and develops, designs, and sells radio frequency (RF) front-end chips and modules in China.

Excellent balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor