Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688045

Slammed 28% Shenzhen Kiwi Instruments Co., Ltd. (SHSE:688045) Screens Well Here But There Might Be A Catch

Unfortunately for some shareholders, the Shenzhen Kiwi Instruments Co., Ltd. (SHSE:688045) share price has dived 28% in the last thirty days, prolonging recent pain. For any long-term shareholders, the last month ends a year to forget by locking in a 72% share price decline.

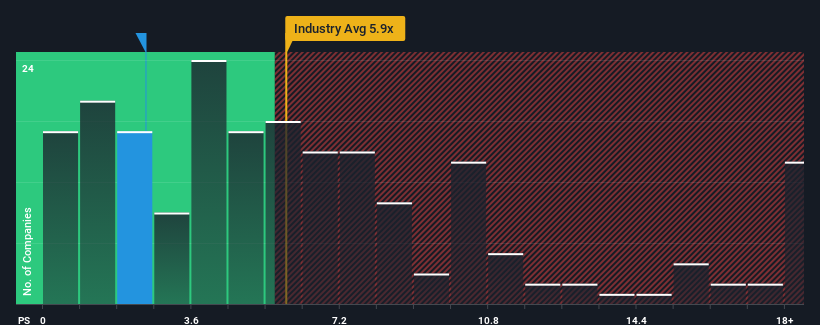

After such a large drop in price, Shenzhen Kiwi Instruments may look like a strong buying opportunity at present with its price-to-sales (or "P/S") ratio of 2.5x, considering almost half of all companies in the Semiconductor industry in China have P/S ratios greater than 5.9x and even P/S higher than 10x aren't out of the ordinary. However, the P/S might be quite low for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Shenzhen Kiwi Instruments

How Shenzhen Kiwi Instruments Has Been Performing

Shenzhen Kiwi Instruments could be doing better as it's been growing revenue less than most other companies lately. It seems that many are expecting the uninspiring revenue performance to persist, which has repressed the growth of the P/S ratio. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Shenzhen Kiwi Instruments.Is There Any Revenue Growth Forecasted For Shenzhen Kiwi Instruments?

Shenzhen Kiwi Instruments' P/S ratio would be typical for a company that's expected to deliver very poor growth or even falling revenue, and importantly, perform much worse than the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 10% last year. This was backed up an excellent period prior to see revenue up by 35% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenues over that time.

Turning to the outlook, the next year should generate growth of 61% as estimated by the lone analyst watching the company. Meanwhile, the rest of the industry is forecast to only expand by 34%, which is noticeably less attractive.

In light of this, it's peculiar that Shenzhen Kiwi Instruments' P/S sits below the majority of other companies. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

The Key Takeaway

Having almost fallen off a cliff, Shenzhen Kiwi Instruments' share price has pulled its P/S way down as well. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

A look at Shenzhen Kiwi Instruments' revenues reveals that, despite glowing future growth forecasts, its P/S is much lower than we'd expect. The reason for this depressed P/S could potentially be found in the risks the market is pricing in. At least price risks look to be very low, but investors seem to think future revenues could see a lot of volatility.

A lot of potential risks can sit within a company's balance sheet. Take a look at our free balance sheet analysis for Shenzhen Kiwi Instruments with six simple checks on some of these key factors.

If you're unsure about the strength of Shenzhen Kiwi Instruments' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688045

Shenzhen Kiwi Instruments

Engages in the design, research, development, manufacture, and sale of analog and digital-analog hybrid integrated circuits in China.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|12.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|21.7% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.1% undervalued

EA

Community Contributor