- China

- /

- Semiconductors

- /

- SHSE:605358

3 Growth Companies With Insider Ownership As High As 26%

Reviewed by Simply Wall St

As global markets navigate the challenges posed by rising U.S. Treasury yields and tepid economic growth, investors are seeking opportunities in growth stocks that show resilience amidst these conditions. One key factor that can signal strong potential is high insider ownership, as it often indicates confidence from those closest to the company's operations.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 34% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 26.3% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 35.6% |

| Laopu Gold (SEHK:6181) | 36.4% | 33% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.7% | 49.1% |

| Findi (ASX:FND) | 35.8% | 64.8% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 107.6% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

| Zhejiang Jolly PharmaceuticalLTD (SZSE:300181) | 23.5% | 24.6% |

Below we spotlight a couple of our favorites from our exclusive screener.

Hangzhou Lion ElectronicsLtd (SHSE:605358)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Hangzhou Lion Electronics Co., Ltd operates in China, focusing on the research and development, production, and sale of semiconductor silicon wafers, power devices, and compound semiconductor radio frequency chips with a market capitalization of CN¥17.55 billion.

Operations: Revenue Segments (in millions of CN¥): Hangzhou Lion Electronics Co., Ltd generates its revenue from semiconductor silicon wafers, power devices, and compound semiconductor radio frequency chips.

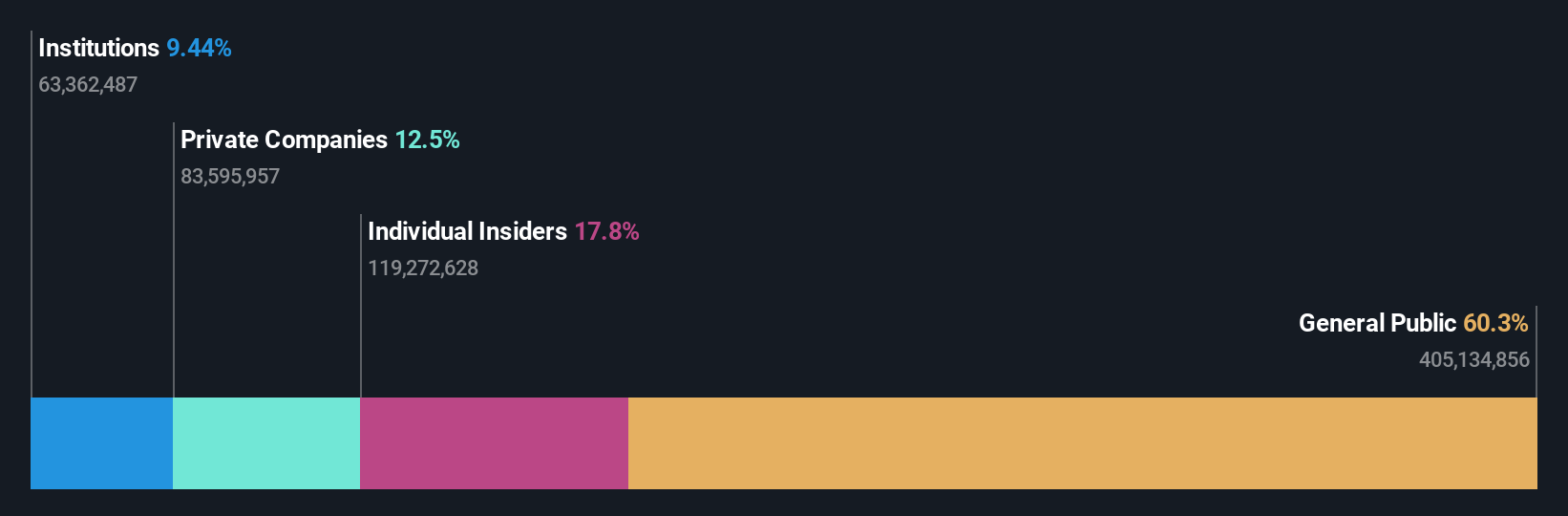

Insider Ownership: 18.8%

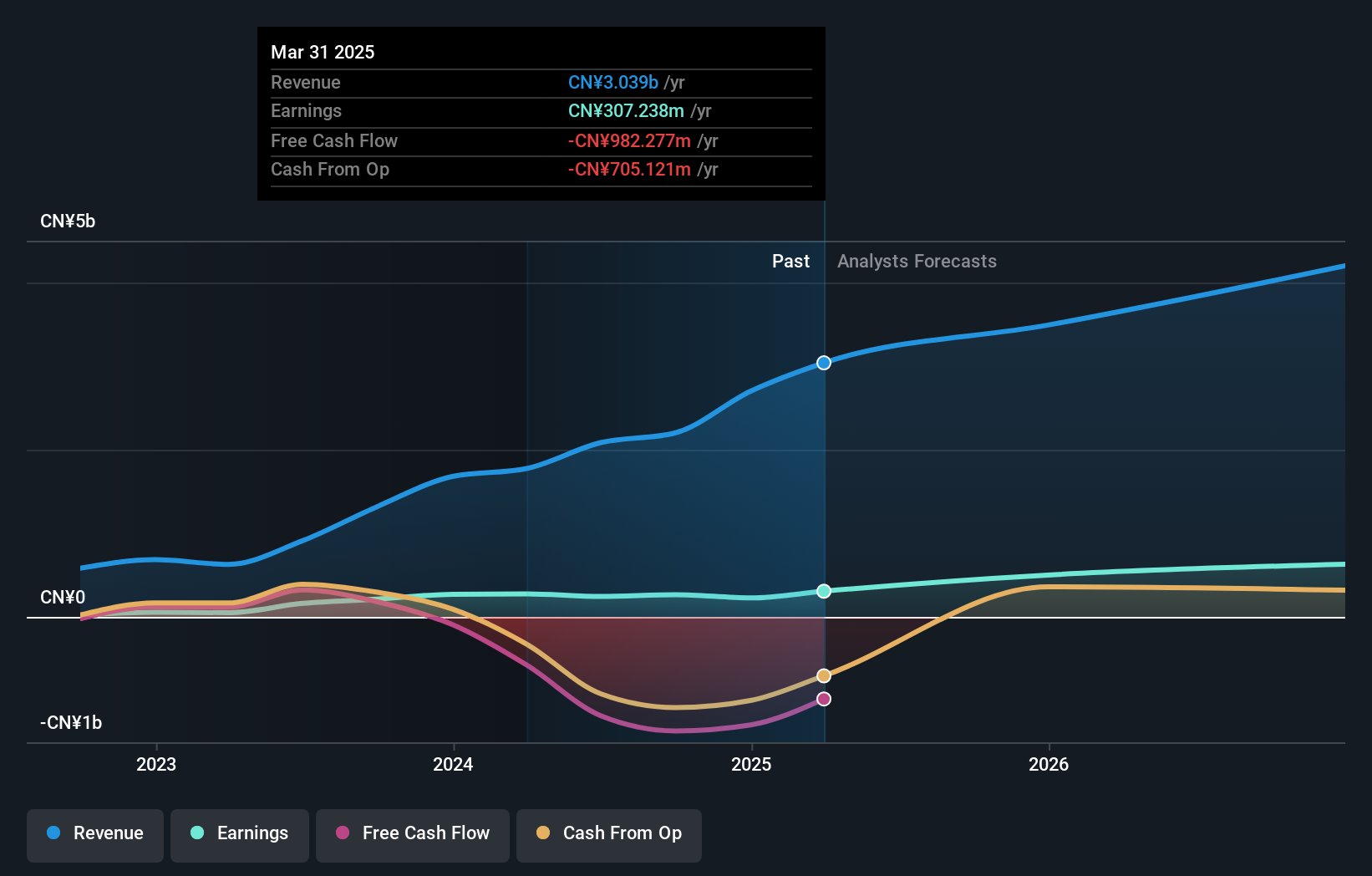

Hangzhou Lion Electronics Ltd. demonstrates significant growth potential with forecasted revenue growth of 23.7% annually, outpacing the Chinese market average. Despite a current net loss, the company is expected to become profitable within three years, suggesting robust future prospects. Recent financial results show increased sales but a net loss of CNY 54.34 million for nine months ending September 2024. The company completed a share buyback worth CNY 50 million, reflecting confidence in its long-term strategy and insider commitment.

- Navigate through the intricacies of Hangzhou Lion ElectronicsLtd with our comprehensive analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Hangzhou Lion ElectronicsLtd shares in the market.

Jiangsu Leadmicro Nano-Equipment Technology (SHSE:688147)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jiangsu Leadmicro Nano-Equipment Technology Ltd designs, manufactures, and services film deposition and etching equipment, with a market cap of CN¥11.85 billion.

Operations: The company's revenue primarily stems from the design, manufacture, and servicing of film deposition and etching equipment.

Insider Ownership: 18.7%

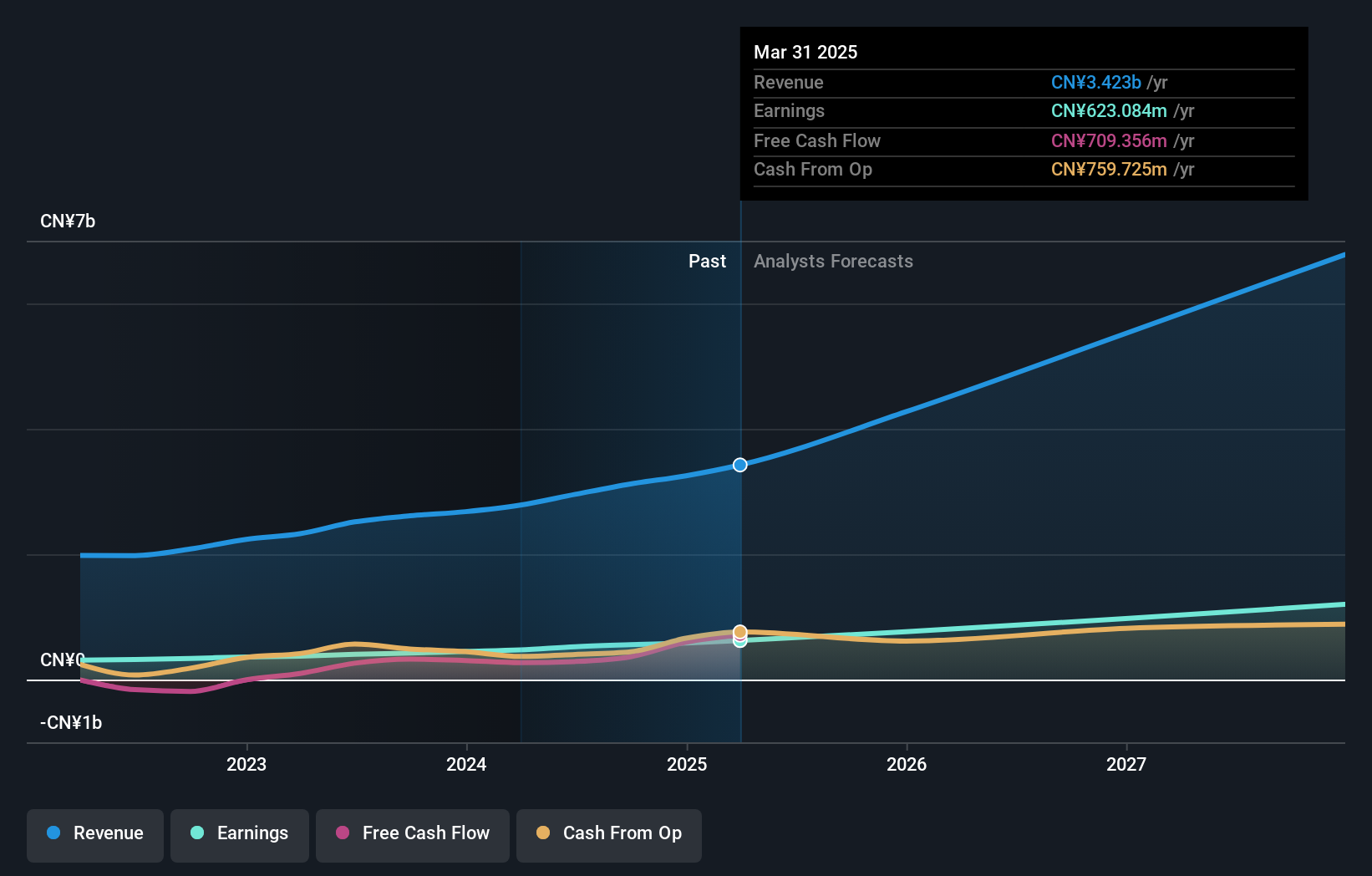

Jiangsu Leadmicro Nano-Equipment Technology shows promising growth prospects, with forecasted annual revenue and earnings growth of 39.1% and 43.6%, respectively, outpacing the Chinese market averages. Recent earnings reveal sales of CNY 1.54 billion for the nine months ending September 2024, up from CNY 1.02 billion a year ago, though net income slightly declined to CNY 150.75 million. The stock trades at a favorable price-to-earnings ratio compared to industry peers despite recent share price volatility.

- Take a closer look at Jiangsu Leadmicro Nano-Equipment Technology's potential here in our earnings growth report.

- According our valuation report, there's an indication that Jiangsu Leadmicro Nano-Equipment Technology's share price might be on the cheaper side.

Shanghai Huace Navigation Technology (SZSE:300627)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Shanghai Huace Navigation Technology Ltd. operates in the field of navigation and positioning technologies, with a market cap of CN¥19.89 billion.

Operations: The company generates revenue from its navigation and positioning technology operations.

Insider Ownership: 26.5%

Shanghai Huace Navigation Technology demonstrates solid growth potential, with revenue forecasted to increase by 25.9% annually, surpassing the Chinese market average. Recent earnings show a rise in sales to CNY 2.27 billion for the nine months ending September 2024, up from CNY 1.83 billion a year ago, and net income improved to CNY 389.69 million. The company's price-to-earnings ratio of 36.2x is attractive compared to industry averages, although its return on equity is expected to remain modest at 19.9%.

- Get an in-depth perspective on Shanghai Huace Navigation Technology's performance by reading our analyst estimates report here.

- Our expertly prepared valuation report Shanghai Huace Navigation Technology implies its share price may be too high.

Taking Advantage

- Embark on your investment journey to our 1523 Fast Growing Companies With High Insider Ownership selection here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Hangzhou Lion ElectronicsLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:605358

Hangzhou Lion ElectronicsLtd

Engages in the research and development, production, and sale of semiconductor silicon wafers and power devices, and compound semiconductor radio frequency chips in China.

High growth potential and slightly overvalued.