Advertisement

As of October 2025, Asian markets are experiencing a notable upswing, with Chinese technology stocks leading the charge despite underlying economic challenges such as weak domestic demand and a prolonged housing market slump. In this environment, growth companies with high insider ownership can be particularly appealing to investors seeking alignment between management and shareholder interests, as these insiders often have a vested interest in the company's long-term success amidst fluctuating market conditions.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Techwing (KOSDAQ:A089030) | 19% | 84.7% |

| Streamax Technology (SZSE:002970) | 32.5% | 33.1% |

| Sineng ElectricLtd (SZSE:300827) | 36.1% | 26.6% |

| Seers Technology (KOSDAQ:A458870) | 33.9% | 84.6% |

| Novoray (SHSE:688300) | 23.6% | 30.3% |

| Laopu Gold (SEHK:6181) | 35.5% | 34.3% |

| J&V Energy Technology (TWSE:6869) | 17.5% | 24.9% |

| Gold Circuit Electronics (TWSE:2368) | 31.4% | 35.2% |

| Fulin Precision (SZSE:300432) | 11.6% | 50.7% |

| Ascentage Pharma Group International (SEHK:6855) | 12.8% | 91.9% |

Let's take a closer look at a couple of our picks from the screened companies.

ABL Bio (KOSDAQ:A298380)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: ABL Bio Inc. is a biotech research company that develops therapeutic drugs for immuno-oncology and neurodegenerative diseases, with a market cap of approximately ₩5.26 trillion.

Operations: The company's revenue is primarily derived from its biotechnology startups segment, amounting to approximately ₩94.93 billion.

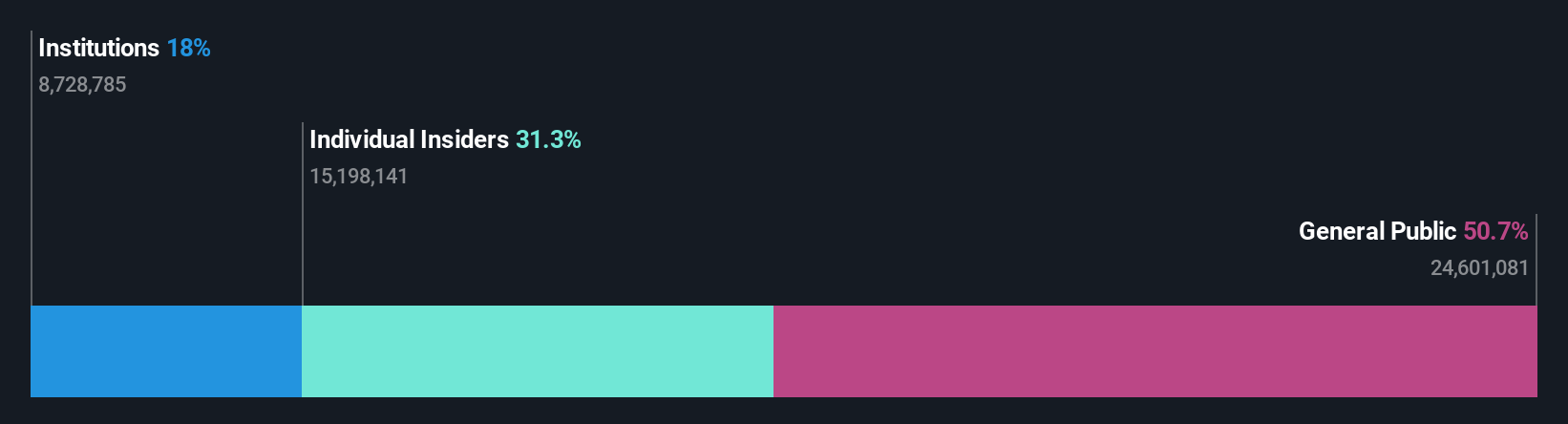

Insider Ownership: 26.3%

Revenue Growth Forecast: 11.1% p.a.

ABL Bio is positioned for growth, with revenue expected to rise 11.1% annually, outpacing the Korean market average of 8.9%. Despite recent share price volatility and a low forecasted return on equity of 3.5%, the company is projected to achieve profitability within three years, indicating above-average market growth potential. No significant insider trading activity has been reported recently, suggesting stability in insider sentiment amidst these developments.

- Take a closer look at ABL Bio's potential here in our earnings growth report.

- According our valuation report, there's an indication that ABL Bio's share price might be on the expensive side.

Jiangsu Pacific Quartz (SHSE:603688)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Jiangsu Pacific Quartz Co., Ltd. focuses on the research, development, manufacture, marketing, and sale of quartz materials in China and has a market cap of CN¥22.87 billion.

Operations: The company's revenue segments include the research, development, manufacture, marketing, and sale of quartz materials in China.

Insider Ownership: 31.6%

Revenue Growth Forecast: 41.7% p.a.

Jiangsu Pacific Quartz is poised for substantial growth, with earnings forecasted to grow significantly at 62.4% annually, surpassing the Chinese market average of 26.3%. Despite recent earnings declines and a volatile share price, the company’s revenue is expected to increase by 41.7% per year, well above the market rate. However, profit margins have contracted notably from last year’s figures and their dividend yield remains low and not well-covered by free cash flows.

- Click here to discover the nuances of Jiangsu Pacific Quartz with our detailed analytical future growth report.

- In light of our recent valuation report, it seems possible that Jiangsu Pacific Quartz is trading beyond its estimated value.

Novoray (SHSE:688300)

Simply Wall St Growth Rating: ★★★★★★

Overview: Novoray Corporation supplies industrial powder materials for diverse applications both in China and internationally, with a market cap of CN¥15.80 billion.

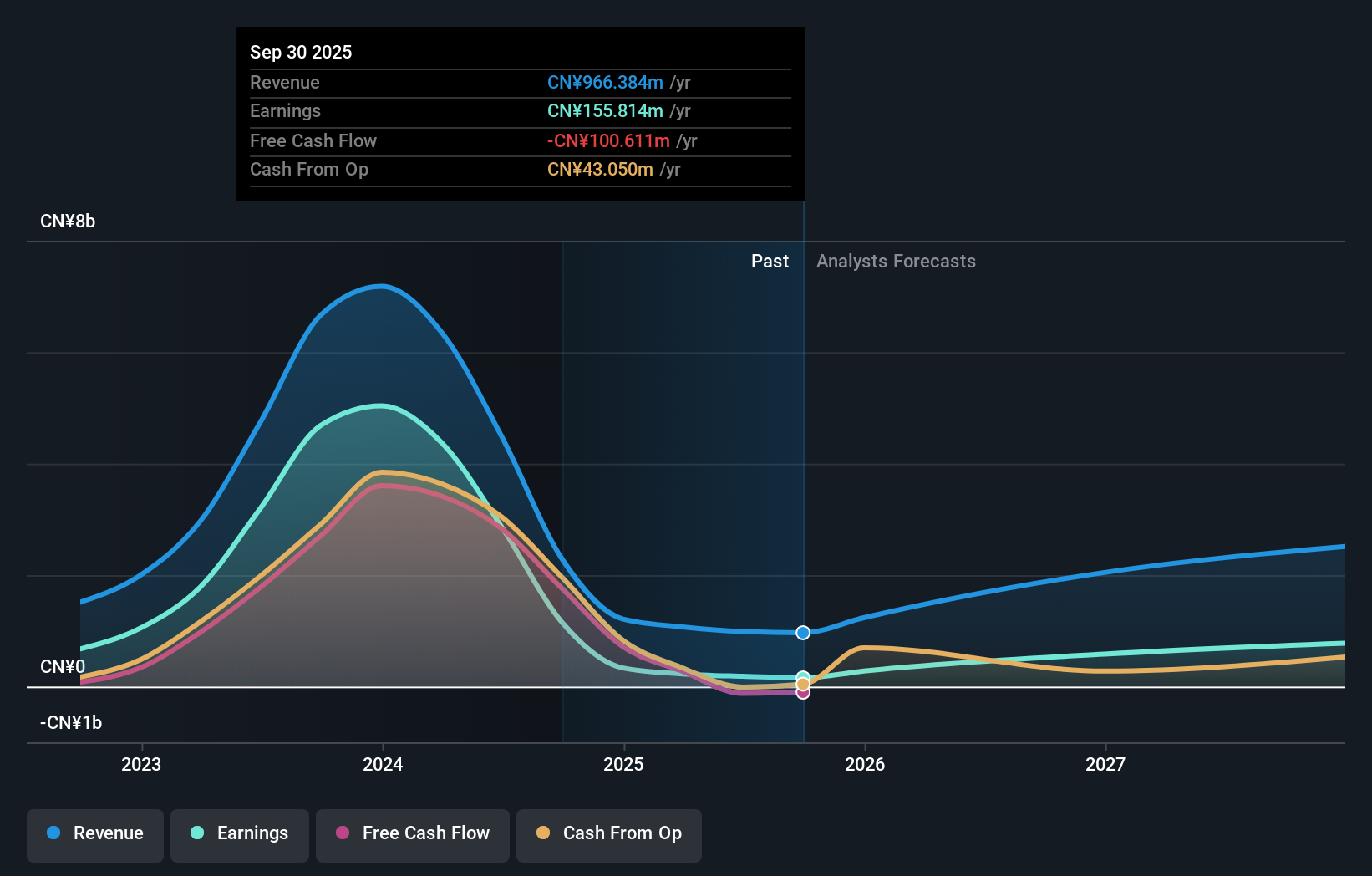

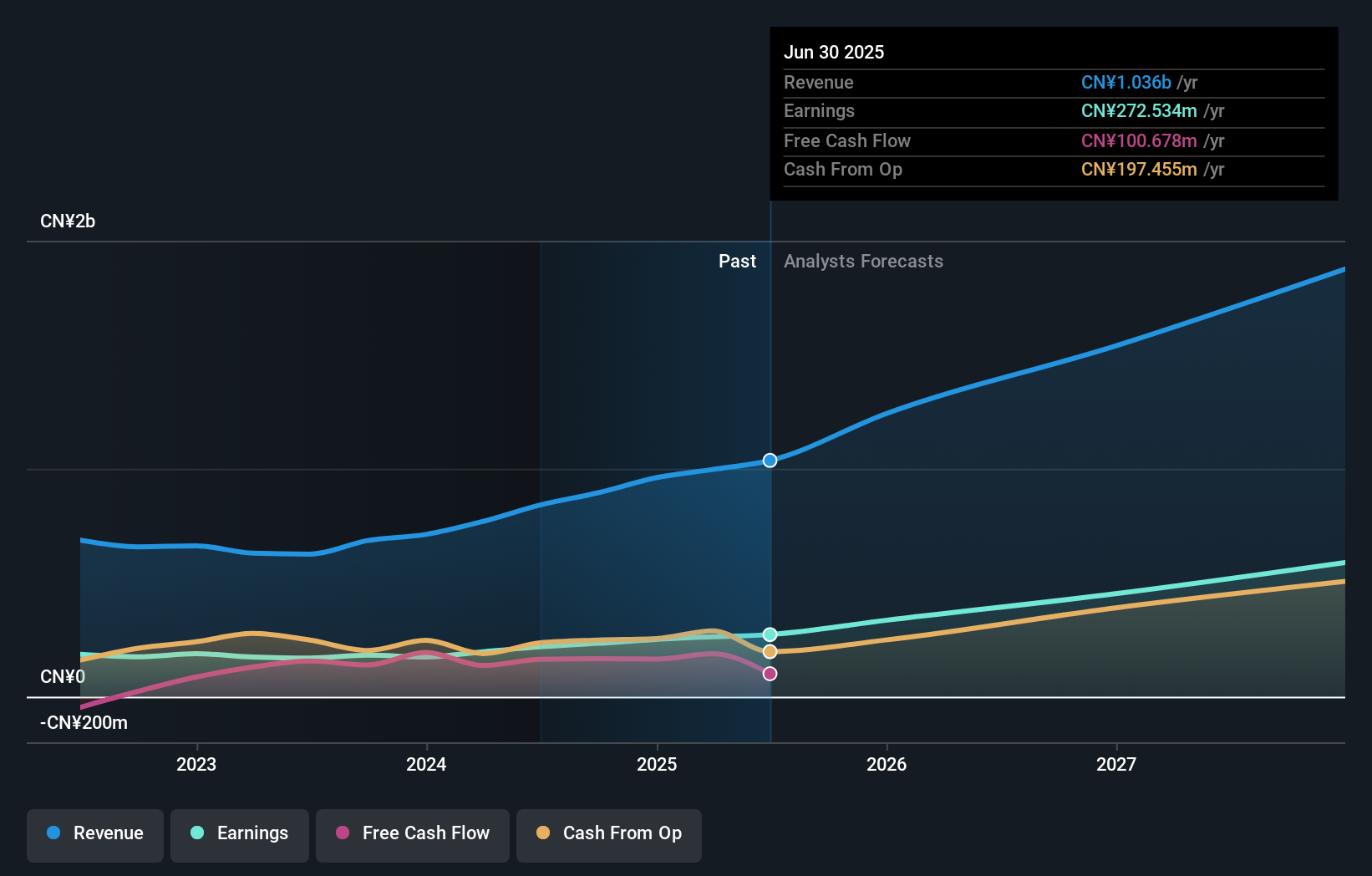

Operations: The company generates revenue from the manufacturing of non-metallic mineral processing products, amounting to CN¥1.04 billion.

Insider Ownership: 23.6%

Revenue Growth Forecast: 23.1% p.a.

Novoray shows promising growth potential with earnings forecasted to grow at 30.3% annually, outpacing the Chinese market's average growth rate. Recent earnings results for H1 2025 revealed a net income increase to CNY 138.65 million and revenue rising to CNY 519.26 million, reflecting robust performance despite a highly volatile share price in recent months. However, the dividend yield is low and not well-supported by free cash flows, warranting cautious consideration from investors focused on sustainable returns.

- Delve into the full analysis future growth report here for a deeper understanding of Novoray.

- The analysis detailed in our Novoray valuation report hints at an inflated share price compared to its estimated value.

Taking Advantage

- Access the full spectrum of 620 Fast Growing Asian Companies With High Insider Ownership by clicking on this link.

- Seeking Other Investments? These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Novoray might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688300

Novoray

Provides industrial powder materials for various applications in China and internationally.

Exceptional growth potential with solid track record.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor