Advertisement

- China

- /

- Semiconductors

- /

- SHSE:600360

Risks Still Elevated At These Prices As Jilin Sino-Microelectronics Co., Ltd. (SHSE:600360) Shares Dive 42%

The Jilin Sino-Microelectronics Co., Ltd. (SHSE:600360) share price has fared very poorly over the last month, falling by a substantial 42%. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 52% loss during that time.

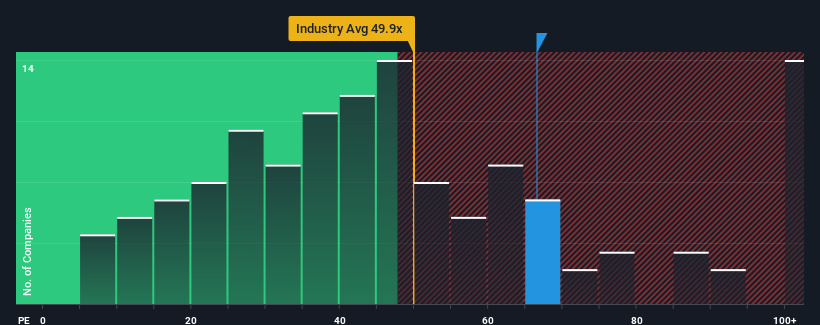

Even after such a large drop in price, given close to half the companies in China have price-to-earnings ratios (or "P/E's") below 32x, you may still consider Jilin Sino-Microelectronics as a stock to avoid entirely with its 66.5x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Earnings have risen firmly for Jilin Sino-Microelectronics recently, which is pleasing to see. One possibility is that the P/E is high because investors think this respectable earnings growth will be enough to outperform the broader market in the near future. If not, then existing shareholders may be a little nervous about the viability of the share price.

Check out our latest analysis for Jilin Sino-Microelectronics

Is There Enough Growth For Jilin Sino-Microelectronics?

In order to justify its P/E ratio, Jilin Sino-Microelectronics would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered a decent 13% gain to the company's bottom line. EPS has also lifted 23% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 38% shows it's noticeably less attractive on an annualised basis.

With this information, we find it concerning that Jilin Sino-Microelectronics is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with recent growth rates.

The Bottom Line On Jilin Sino-Microelectronics' P/E

Even after such a strong price drop, Jilin Sino-Microelectronics' P/E still exceeds the rest of the market significantly. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Jilin Sino-Microelectronics currently trades on a much higher than expected P/E since its recent three-year growth is lower than the wider market forecast. When we see weak earnings with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

You should always think about risks. Case in point, we've spotted 2 warning signs for Jilin Sino-Microelectronics you should be aware of.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600360

Jilin Sino-Microelectronics

Designs, develops, and markets semiconductor devices in China and internationally.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|8.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.6% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor