Advertisement

After Leaping 28% Shandong Kaisheng New Materials Co.,Ltd. (SZSE:301069) Shares Are Not Flying Under The Radar

Shandong Kaisheng New Materials Co.,Ltd. (SZSE:301069) shareholders are no doubt pleased to see that the share price has bounced 28% in the last month, although it is still struggling to make up recently lost ground. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 47% in the last twelve months.

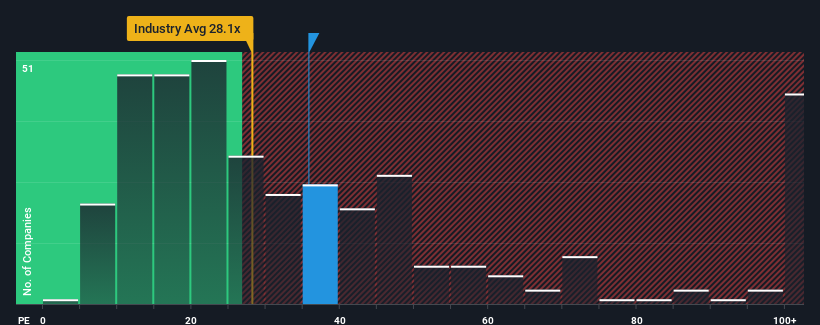

Since its price has surged higher, Shandong Kaisheng New MaterialsLtd's price-to-earnings (or "P/E") ratio of 35.8x might make it look like a sell right now compared to the market in China, where around half of the companies have P/E ratios below 29x and even P/E's below 18x are quite common. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

With earnings that are retreating more than the market's of late, Shandong Kaisheng New MaterialsLtd has been very sluggish. One possibility is that the P/E is high because investors think the company will turn things around completely and accelerate past most others in the market. If not, then existing shareholders may be very nervous about the viability of the share price.

See our latest analysis for Shandong Kaisheng New MaterialsLtd

Does Growth Match The High P/E?

There's an inherent assumption that a company should outperform the market for P/E ratios like Shandong Kaisheng New MaterialsLtd's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 25% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 17% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 91% during the coming year according to the one analyst following the company. That's shaping up to be materially higher than the 41% growth forecast for the broader market.

With this information, we can see why Shandong Kaisheng New MaterialsLtd is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

Shandong Kaisheng New MaterialsLtd's P/E is getting right up there since its shares have risen strongly. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Shandong Kaisheng New MaterialsLtd maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

It is also worth noting that we have found 3 warning signs for Shandong Kaisheng New MaterialsLtd (1 doesn't sit too well with us!) that you need to take into consideration.

If you're unsure about the strength of Shandong Kaisheng New MaterialsLtd's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301069

Shandong Kaisheng New MaterialsLtd

Engages in the research and development, production, and sale of fine chemical products and new polymer materials in Mainland China, Japan, South Korea, the United States, and internationally.

Adequate balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor