- China

- /

- Medical Equipment

- /

- SZSE:300832

High Insider Ownership Fuels Growth Stocks In October 2024

Reviewed by Simply Wall St

As global markets navigate a landscape of fluctuating interest rates and shifting economic indicators, the U.S. indices have shown resilience, with the S&P 500 and Nasdaq Composite making notable gains driven by sectors like utilities and technology. In this environment, growth companies with high insider ownership are capturing attention as they often reflect strong internal confidence and alignment of interests, which can be particularly appealing amid evolving market conditions.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 30.1% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 27.4% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 35.6% |

| Medley (TSE:4480) | 34% | 30.4% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.7% | 49.1% |

| Findi (ASX:FND) | 35.8% | 64.8% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 105.8% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 107.6% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

We'll examine a selection from our screener results.

Ming Yang Smart Energy Group (SHSE:601615)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Ming Yang Smart Energy Group Limited is involved in the research, design, manufacture, sale, maintenance, and operation of energy equipment and wind turbines in China with a market cap of CN¥25.03 billion.

Operations: Ming Yang Smart Energy Group Limited generates revenue through its activities in the research and development, design, manufacture, sale, maintenance, and operation of energy equipment and wind turbines in China.

Insider Ownership: 15.8%

Revenue Growth Forecast: 20.4% p.a.

Ming Yang Smart Energy Group's revenue is forecast to grow at 20.4% annually, outpacing the Chinese market's 13.5% growth rate, while earnings are expected to rise significantly by 55.2% per year. Despite these positive growth prospects, profit margins have declined from last year's 6.1% to 1.3%. Recent financial results show stable net income with CNY 660.66 million for H1 2024, indicating steady performance amidst strategic leadership changes and equity incentive adjustments.

- Take a closer look at Ming Yang Smart Energy Group's potential here in our earnings growth report.

- Our comprehensive valuation report raises the possibility that Ming Yang Smart Energy Group is priced higher than what may be justified by its financials.

Hubei DinglongLtd (SZSE:300054)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hubei Dinglong Co., Ltd. focuses on the research, development, production, and service of integrated circuit chip design and semiconductor materials, with a market cap of CN¥25.89 billion.

Operations: The company generates revenue of CN¥3.00 billion from its photoelectric imaging display and semiconductor process materials industry segment.

Insider Ownership: 29.9%

Revenue Growth Forecast: 16.6% p.a.

Hubei Dinglong Ltd. demonstrates strong growth potential with revenue predicted to rise by 16.6% annually, surpassing the Chinese market's average of 13.5%. Earnings are set to increase significantly at 33.8% per year, highlighting robust profitability prospects. Recent earnings show substantial improvement; sales reached CNY 2.43 billion for the first nine months of 2024, up from CNY 1.87 billion a year ago, with net income more than doubling to CNY 376 million.

- Navigate through the intricacies of Hubei DinglongLtd with our comprehensive analyst estimates report here.

- Our valuation report unveils the possibility Hubei DinglongLtd's shares may be trading at a premium.

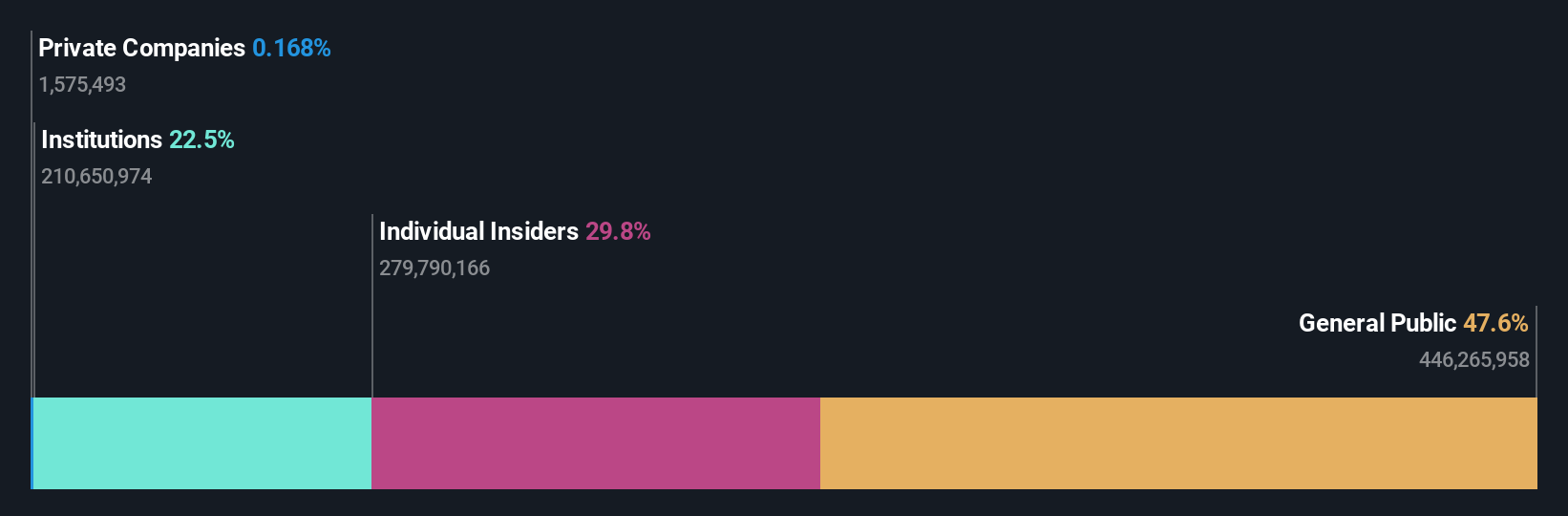

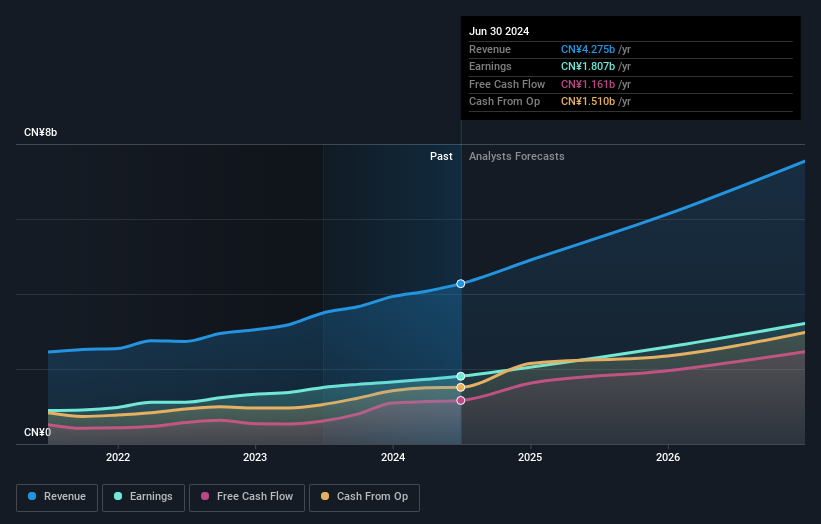

Shenzhen New Industries Biomedical Engineering (SZSE:300832)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen New Industries Biomedical Engineering Co., Ltd. is a bio-medical company involved in the research, development, production, and sale of clinical laboratory instruments and in vitro diagnostic reagents to hospitals both in China and internationally, with a market cap of CN¥53.59 billion.

Operations: The company generates revenue primarily from the sale of in vitro diagnostic products, amounting to CN¥4.28 billion.

Insider Ownership: 21.8%

Revenue Growth Forecast: 22.6% p.a.

Shenzhen New Industries Biomedical Engineering is poised for growth with revenue expected to increase by 22.6% annually, outpacing the Chinese market's 13.5%. Earnings are forecasted to grow significantly at 23% per year, although slightly below the market average of 23.8%. Recent earnings revealed a rise in sales to CNY 2.21 billion and net income to CNY 903.15 million for H1 2024, reflecting strong operational performance despite an unstable dividend history.

- Dive into the specifics of Shenzhen New Industries Biomedical Engineering here with our thorough growth forecast report.

- The analysis detailed in our Shenzhen New Industries Biomedical Engineering valuation report hints at an deflated share price compared to its estimated value.

Where To Now?

- Take a closer look at our Fast Growing Companies With High Insider Ownership list of 1489 companies by clicking here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300832

Shenzhen New Industries Biomedical Engineering

A bio-medical company, engages in the research, development, production, and sale of clinical laboratory instruments and in vitro diagnostic reagents to hospitals in the People's Republic of China and internationally.

Flawless balance sheet and undervalued.