Advertisement

Is Zhuhai Zhongfu EnterpriseLtd (SZSE:000659) A Risky Investment?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Zhuhai Zhongfu Enterprise Co.,Ltd (SZSE:000659) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

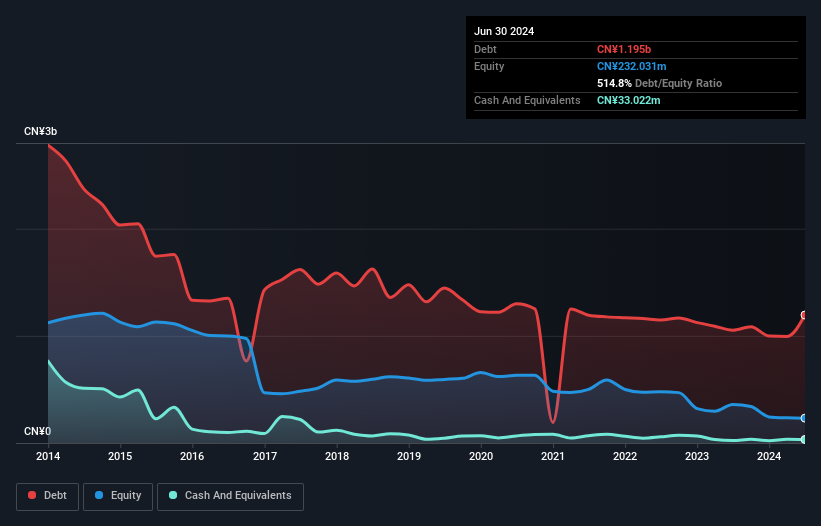

See our latest analysis for Zhuhai Zhongfu EnterpriseLtd

What Is Zhuhai Zhongfu EnterpriseLtd's Debt?

As you can see below, at the end of June 2024, Zhuhai Zhongfu EnterpriseLtd had CN¥1.19b of debt, up from CN¥1.05b a year ago. Click the image for more detail. However, it does have CN¥33.0m in cash offsetting this, leading to net debt of about CN¥1.16b.

How Strong Is Zhuhai Zhongfu EnterpriseLtd's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Zhuhai Zhongfu EnterpriseLtd had liabilities of CN¥1.53b due within 12 months and liabilities of CN¥153.6m due beyond that. Offsetting these obligations, it had cash of CN¥33.0m as well as receivables valued at CN¥222.8m due within 12 months. So it has liabilities totalling CN¥1.43b more than its cash and near-term receivables, combined.

This deficit isn't so bad because Zhuhai Zhongfu EnterpriseLtd is worth CN¥3.86b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Weak interest cover of 0.13 times and a disturbingly high net debt to EBITDA ratio of 10.2 hit our confidence in Zhuhai Zhongfu EnterpriseLtd like a one-two punch to the gut. This means we'd consider it to have a heavy debt load. Even worse, Zhuhai Zhongfu EnterpriseLtd saw its EBIT tank 89% over the last 12 months. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Zhuhai Zhongfu EnterpriseLtd will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Happily for any shareholders, Zhuhai Zhongfu EnterpriseLtd actually produced more free cash flow than EBIT over the last three years. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

On the face of it, Zhuhai Zhongfu EnterpriseLtd's interest cover left us tentative about the stock, and its EBIT growth rate was no more enticing than the one empty restaurant on the busiest night of the year. But at least it's pretty decent at converting EBIT to free cash flow; that's encouraging. Once we consider all the factors above, together, it seems to us that Zhuhai Zhongfu EnterpriseLtd's debt is making it a bit risky. That's not necessarily a bad thing, but we'd generally feel more comfortable with less leverage. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 1 warning sign we've spotted with Zhuhai Zhongfu EnterpriseLtd .

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Zhuhai Zhongfu EnterpriseLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:000659

Zhuhai Zhongfu EnterpriseLtd

Researches, develops, manufactures, and sells PET beverage packaging materials in China.

Imperfect balance sheet and overvalued.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor