Advertisement

Why We're Not Concerned About Jiangsu Favored Nanotechnology Co., Ltd's (SHSE:688371) Share Price

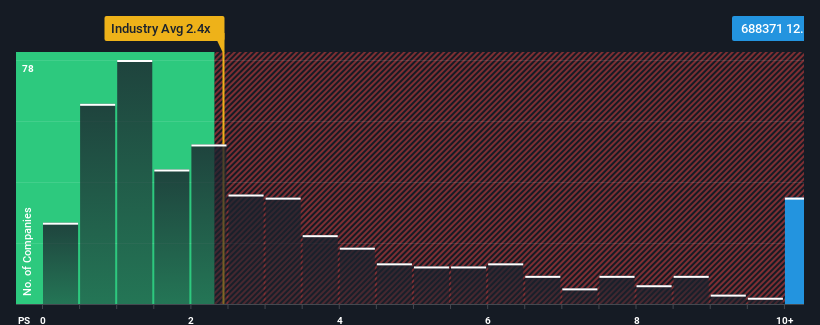

When close to half the companies in the Chemicals industry in China have price-to-sales ratios (or "P/S") below 2.4x, you may consider Jiangsu Favored Nanotechnology Co., Ltd (SHSE:688371) as a stock to avoid entirely with its 12.1x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

See our latest analysis for Jiangsu Favored Nanotechnology

How Jiangsu Favored Nanotechnology Has Been Performing

With revenue growth that's superior to most other companies of late, Jiangsu Favored Nanotechnology has been doing relatively well. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on analyst estimates for the company? Then our free report on Jiangsu Favored Nanotechnology will help you uncover what's on the horizon.What Are Revenue Growth Metrics Telling Us About The High P/S?

The only time you'd be truly comfortable seeing a P/S as steep as Jiangsu Favored Nanotechnology's is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered an exceptional 40% gain to the company's top line. Revenue has also lifted 7.9% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Accordingly, shareholders would have probably been satisfied with the medium-term rates of revenue growth.

Turning to the outlook, the next year should generate growth of 57% as estimated by the one analyst watching the company. With the industry only predicted to deliver 24%, the company is positioned for a stronger revenue result.

With this in mind, it's not hard to understand why Jiangsu Favored Nanotechnology's P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What Does Jiangsu Favored Nanotechnology's P/S Mean For Investors?

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our look into Jiangsu Favored Nanotechnology shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless these conditions change, they will continue to provide strong support to the share price.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Jiangsu Favored Nanotechnology that you need to be mindful of.

If these risks are making you reconsider your opinion on Jiangsu Favored Nanotechnology, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688371

Jiangsu Favored Nanotechnology

Engages in the research and development, production, and sale of nanotechnology coatings worldwide.

Flawless balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor