Advertisement

Zhejiang Yonghe Refrigerant Co., Ltd. (SHSE:605020) CEO Jianguo Tong, the company's largest shareholder sees 5.2% reduction in holdings value

Key Insights

- Significant insider control over Zhejiang Yonghe Refrigerant implies vested interests in company growth

- A total of 2 investors have a majority stake in the company with 55% ownership

- Past performance of a company along with ownership data serve to give a strong idea about prospects for a business

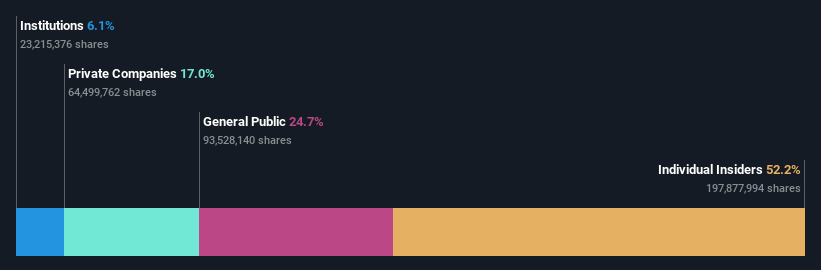

Every investor in Zhejiang Yonghe Refrigerant Co., Ltd. (SHSE:605020) should be aware of the most powerful shareholder groups. We can see that individual insiders own the lion's share in the company with 52% ownership. In other words, the group stands to gain the most (or lose the most) from their investment into the company.

As market cap fell to CN¥8.1b last week, insiders would have faced the highest losses than any other shareholder groups of the company.

Let's take a closer look to see what the different types of shareholders can tell us about Zhejiang Yonghe Refrigerant.

Check out our latest analysis for Zhejiang Yonghe Refrigerant

What Does The Institutional Ownership Tell Us About Zhejiang Yonghe Refrigerant?

Many institutions measure their performance against an index that approximates the local market. So they usually pay more attention to companies that are included in major indices.

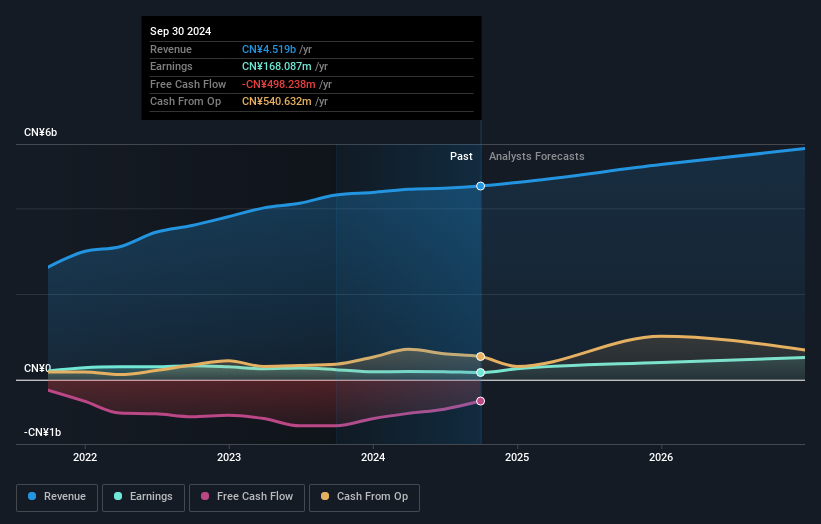

As you can see, institutional investors have a fair amount of stake in Zhejiang Yonghe Refrigerant. This suggests some credibility amongst professional investors. But we can't rely on that fact alone since institutions make bad investments sometimes, just like everyone does. When multiple institutions own a stock, there's always a risk that they are in a 'crowded trade'. When such a trade goes wrong, multiple parties may compete to sell stock fast. This risk is higher in a company without a history of growth. You can see Zhejiang Yonghe Refrigerant's historic earnings and revenue below, but keep in mind there's always more to the story.

Hedge funds don't have many shares in Zhejiang Yonghe Refrigerant. With a 48% stake, CEO Jianguo Tong is the largest shareholder. Ningbo Meishan Bonded Port Area Binglong Investment Partnership Enterprise (LP) is the second largest shareholder owning 7.3% of common stock, and Zhejiang Xinghao Investment Co., Ltd. holds about 5.0% of the company stock.

A more detailed study of the shareholder registry showed us that 2 of the top shareholders have a considerable amount of ownership in the company, via their 55% stake.

While it makes sense to study institutional ownership data for a company, it also makes sense to study analyst sentiments to know which way the wind is blowing. There is a little analyst coverage of the stock, but not much. So there is room for it to gain more coverage.

Insider Ownership Of Zhejiang Yonghe Refrigerant

The definition of an insider can differ slightly between different countries, but members of the board of directors always count. The company management answer to the board and the latter should represent the interests of shareholders. Notably, sometimes top-level managers are on the board themselves.

I generally consider insider ownership to be a good thing. However, on some occasions it makes it more difficult for other shareholders to hold the board accountable for decisions.

Our information suggests that insiders own more than half of Zhejiang Yonghe Refrigerant Co., Ltd.. This gives them effective control of the company. Given it has a market cap of CN¥8.1b, that means insiders have a whopping CN¥4.2b worth of shares in their own names. Most would be pleased to see the board is investing alongside them. You may wish to discover if they have been buying or selling.

General Public Ownership

The general public, who are usually individual investors, hold a 25% stake in Zhejiang Yonghe Refrigerant. While this size of ownership may not be enough to sway a policy decision in their favour, they can still make a collective impact on company policies.

Private Company Ownership

It seems that Private Companies own 17%, of the Zhejiang Yonghe Refrigerant stock. It's hard to draw any conclusions from this fact alone, so its worth looking into who owns those private companies. Sometimes insiders or other related parties have an interest in shares in a public company through a separate private company.

Next Steps:

I find it very interesting to look at who exactly owns a company. But to truly gain insight, we need to consider other information, too. Take risks for example - Zhejiang Yonghe Refrigerant has 4 warning signs (and 1 which is significant) we think you should know about.

If you would prefer discover what analysts are predicting in terms of future growth, do not miss this free report on analyst forecasts.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Yonghe Refrigerant might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:605020

Zhejiang Yonghe Refrigerant

Engages in research and development, production, and sale of fluorine chemical products.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor