Advertisement

- China

- /

- Metals and Mining

- /

- SHSE:603315

Some Liaoning Fu-An Heavy Industry Co.,Ltd (SHSE:603315) Shareholders Look For Exit As Shares Take 26% Pounding

Liaoning Fu-An Heavy Industry Co.,Ltd (SHSE:603315) shares have had a horrible month, losing 26% after a relatively good period beforehand. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 22% share price drop.

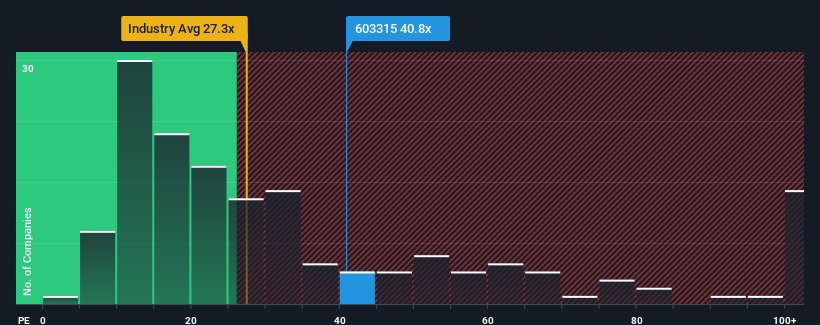

In spite of the heavy fall in price, Liaoning Fu-An Heavy IndustryLtd's price-to-earnings (or "P/E") ratio of 40.8x might still make it look like a sell right now compared to the market in China, where around half of the companies have P/E ratios below 30x and even P/E's below 18x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

With earnings growth that's exceedingly strong of late, Liaoning Fu-An Heavy IndustryLtd has been doing very well. It seems that many are expecting the strong earnings performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. If not, then existing shareholders might be a little nervous about the viability of the share price.

See our latest analysis for Liaoning Fu-An Heavy IndustryLtd

Is There Enough Growth For Liaoning Fu-An Heavy IndustryLtd?

There's an inherent assumption that a company should outperform the market for P/E ratios like Liaoning Fu-An Heavy IndustryLtd's to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 92% last year. However, this wasn't enough as the latest three year period has seen a very unpleasant 23% drop in EPS in aggregate. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

In contrast to the company, the rest of the market is expected to grow by 38% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

With this information, we find it concerning that Liaoning Fu-An Heavy IndustryLtd is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

The Bottom Line On Liaoning Fu-An Heavy IndustryLtd's P/E

Despite the recent share price weakness, Liaoning Fu-An Heavy IndustryLtd's P/E remains higher than most other companies. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Liaoning Fu-An Heavy IndustryLtd revealed its shrinking earnings over the medium-term aren't impacting its high P/E anywhere near as much as we would have predicted, given the market is set to grow. Right now we are increasingly uncomfortable with the high P/E as this earnings performance is highly unlikely to support such positive sentiment for long. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

We don't want to rain on the parade too much, but we did also find 3 warning signs for Liaoning Fu-An Heavy IndustryLtd (1 can't be ignored!) that you need to be mindful of.

You might be able to find a better investment than Liaoning Fu-An Heavy IndustryLtd. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603315

Liaoning Fu-An Heavy IndustryLtd

Produces and sells steel castings in China.

Mediocre balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor