Advertisement

- China

- /

- Metals and Mining

- /

- SHSE:601212

Baiyin Nonferrous Group's (SHSE:601212) Returns On Capital Not Reflecting Well On The Business

Ignoring the stock price of a company, what are the underlying trends that tell us a business is past the growth phase? More often than not, we'll see a declining return on capital employed (ROCE) and a declining amount of capital employed. Basically the company is earning less on its investments and it is also reducing its total assets. Having said that, after a brief look, Baiyin Nonferrous Group (SHSE:601212) we aren't filled with optimism, but let's investigate further.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Baiyin Nonferrous Group is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

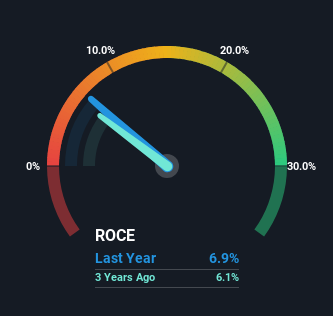

0.069 = CN¥1.8b ÷ (CN¥48b - CN¥22b) (Based on the trailing twelve months to March 2024).

Thus, Baiyin Nonferrous Group has an ROCE of 6.9%. On its own that's a low return on capital but it's in line with the industry's average returns of 7.3%.

Check out our latest analysis for Baiyin Nonferrous Group

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you'd like to look at how Baiyin Nonferrous Group has performed in the past in other metrics, you can view this free graph of Baiyin Nonferrous Group's past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

There is reason to be cautious about Baiyin Nonferrous Group, given the returns are trending downwards. To be more specific, the ROCE was 9.6% five years ago, but since then it has dropped noticeably. And on the capital employed front, the business is utilizing roughly the same amount of capital as it was back then. This combination can be indicative of a mature business that still has areas to deploy capital, but the returns received aren't as high due potentially to new competition or smaller margins. If these trends continue, we wouldn't expect Baiyin Nonferrous Group to turn into a multi-bagger.

Another thing to note, Baiyin Nonferrous Group has a high ratio of current liabilities to total assets of 45%. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Bottom Line

All in all, the lower returns from the same amount of capital employed aren't exactly signs of a compounding machine. It should come as no surprise then that the stock has fallen 22% over the last five years, so it looks like investors are recognizing these changes. That being the case, unless the underlying trends revert to a more positive trajectory, we'd consider looking elsewhere.

If you'd like to know about the risks facing Baiyin Nonferrous Group, we've discovered 2 warning signs that you should be aware of.

While Baiyin Nonferrous Group may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're here to simplify it.

Discover if Baiyin Nonferrous Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:601212

Baiyin Nonferrous Group

Engages in the mining, smelting, processing, and trading of various non-ferrous metals in China.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor