- China

- /

- Personal Products

- /

- SHSE:600315

Earnings are growing at Shanghai Jahwa United (SHSE:600315) but shareholders still don't like its prospects

Shanghai Jahwa United Co., Ltd. (SHSE:600315) shareholders should be happy to see the share price up 14% in the last month. But that doesn't change the fact that the returns over the last three years have been disappointing. Indeed, the share price is down a tragic 65% in the last three years. So it's good to see it climbing back up. The rise has some hopeful, but turnarounds are often precarious.

With the stock having lost 4.6% in the past week, it's worth taking a look at business performance and seeing if there's any red flags.

View our latest analysis for Shanghai Jahwa United

To quote Buffett, 'Ships will sail around the world but the Flat Earth Society will flourish. There will continue to be wide discrepancies between price and value in the marketplace...' One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

Although the share price is down over three years, Shanghai Jahwa United actually managed to grow EPS by 3.1% per year in that time. This is quite a puzzle, and suggests there might be something temporarily buoying the share price. Or else the company was over-hyped in the past, and so its growth has disappointed.

After considering the numbers, we'd posit that the the market had higher expectations of EPS growth, three years back. But it's possible a look at other metrics will be enlightening.

The modest 1.1% dividend yield is unlikely to be guiding the market view of the stock. We think that the revenue decline over three years, at a rate of 5.0% per year, probably had some shareholders looking to sell. After all, if revenue keeps shrinking, it may be difficult to find earnings growth in the future.

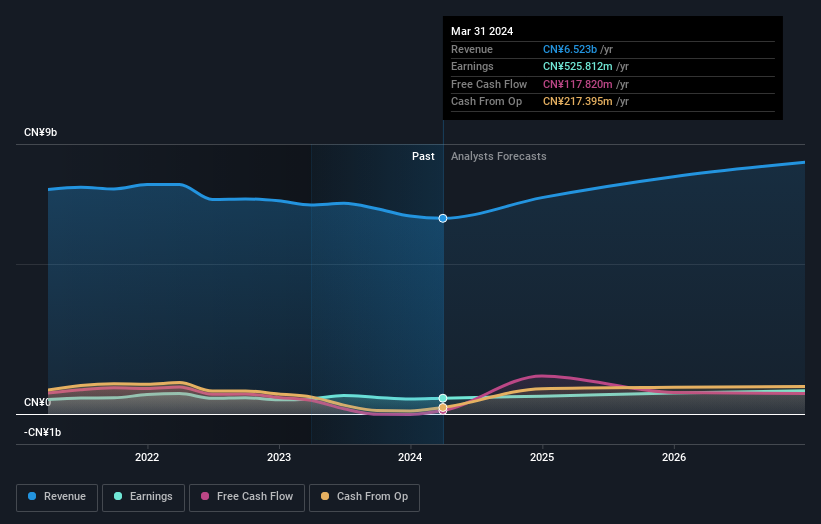

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

Shanghai Jahwa United is a well known stock, with plenty of analyst coverage, suggesting some visibility into future growth. If you are thinking of buying or selling Shanghai Jahwa United stock, you should check out this free report showing analyst consensus estimates for future profits.

A Different Perspective

We regret to report that Shanghai Jahwa United shareholders are down 29% for the year (even including dividends). Unfortunately, that's worse than the broader market decline of 8.2%. However, it could simply be that the share price has been impacted by broader market jitters. It might be worth keeping an eye on the fundamentals, in case there's a good opportunity. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 4% over the last half decade. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. It's always interesting to track share price performance over the longer term. But to understand Shanghai Jahwa United better, we need to consider many other factors. Even so, be aware that Shanghai Jahwa United is showing 1 warning sign in our investment analysis , you should know about...

But note: Shanghai Jahwa United may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Chinese exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600315

Shanghai Jahwa United

Engages in the research and development, production, and sale of skin care, personal care, home cleaning, maternal, and child products in the People’s Republic of China and internationally.

Flawless balance sheet with questionable track record.