Advertisement

- China

- /

- Medical Equipment

- /

- SHSE:688151

Optimistic Investors Push Hubei Huaqiang High-Tech Co., Ltd. (SHSE:688151) Shares Up 29% But Growth Is Lacking

Hubei Huaqiang High-Tech Co., Ltd. (SHSE:688151) shareholders would be excited to see that the share price has had a great month, posting a 29% gain and recovering from prior weakness. The last 30 days bring the annual gain to a very sharp 29%.

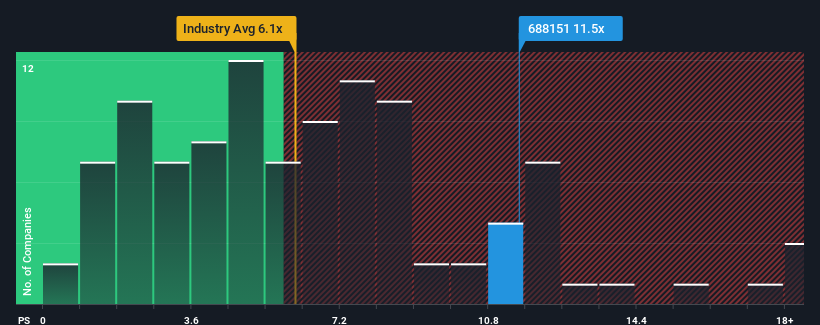

After such a large jump in price, Hubei Huaqiang High-Tech may be sending strong sell signals at present with a price-to-sales (or "P/S") ratio of 11.5x, when you consider almost half of the companies in the Medical Equipment industry in China have P/S ratios under 6.1x and even P/S lower than 3x aren't out of the ordinary. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Hubei Huaqiang High-Tech

What Does Hubei Huaqiang High-Tech's Recent Performance Look Like?

The revenue growth achieved at Hubei Huaqiang High-Tech over the last year would be more than acceptable for most companies. It might be that many expect the respectable revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Hubei Huaqiang High-Tech will help you shine a light on its historical performance.Is There Enough Revenue Growth Forecasted For Hubei Huaqiang High-Tech?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Hubei Huaqiang High-Tech's to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 10% last year. Still, lamentably revenue has fallen 59% in aggregate from three years ago, which is disappointing. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Comparing that to the industry, which is predicted to deliver 24% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

With this in mind, we find it worrying that Hubei Huaqiang High-Tech's P/S exceeds that of its industry peers. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

What Does Hubei Huaqiang High-Tech's P/S Mean For Investors?

The strong share price surge has lead to Hubei Huaqiang High-Tech's P/S soaring as well. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Hubei Huaqiang High-Tech currently trades on a much higher than expected P/S since its recent revenues have been in decline over the medium-term. With a revenue decline on investors' minds, the likelihood of a souring sentiment is quite high which could send the P/S back in line with what we'd expect. If recent medium-term revenue trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

There are also other vital risk factors to consider and we've discovered 2 warning signs for Hubei Huaqiang High-Tech (1 is significant!) that you should be aware of before investing here.

If these risks are making you reconsider your opinion on Hubei Huaqiang High-Tech, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Hubei Huaqiang High-Tech might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688151

Hubei Huaqiang High-Tech

Research, develops, produces, and sells special protective equipment, pharmaceutical packaging, and medical devices in China.

Flawless balance sheet with minimal risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor