Advertisement

- Saudi Arabia

- /

- Healthcare Services

- /

- SASE:9627

Unveiling Three Undiscovered Gems On The None Exchange

Simply Wall St

Reviewed by Simply Wall St

In the current global market landscape, uncertainty surrounding tariffs and mixed economic indicators have contributed to a cautious sentiment among investors, with key indices like the S&P 500 experiencing slight declines. Despite these challenges, small-cap stocks can present unique opportunities for growth as they often remain under the radar amidst broader market fluctuations. Identifying promising small-cap companies requires a keen understanding of their potential for innovation and resilience in navigating complex economic environments.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Industrias del Cobre Sociedad Anónima | NA | 19.08% | 22.33% | ★★★★★★ |

| Aesler Grup Internasional | NA | -17.61% | -40.21% | ★★★★★★ |

| Watt's | 70.56% | 7.69% | -0.53% | ★★★★★☆ |

| Hermes Transportes Blindados | 50.88% | 4.57% | 3.33% | ★★★★★☆ |

| Inverfal PerúA | 31.20% | 10.56% | 17.83% | ★★★★★☆ |

| Compañía Electro Metalúrgica | 71.27% | 12.50% | 19.90% | ★★★★☆☆ |

| Sociedad Eléctrica del Sur Oeste | 42.67% | 8.52% | 4.10% | ★★★★☆☆ |

| BOSQAR d.d | 94.35% | 39.11% | 23.56% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

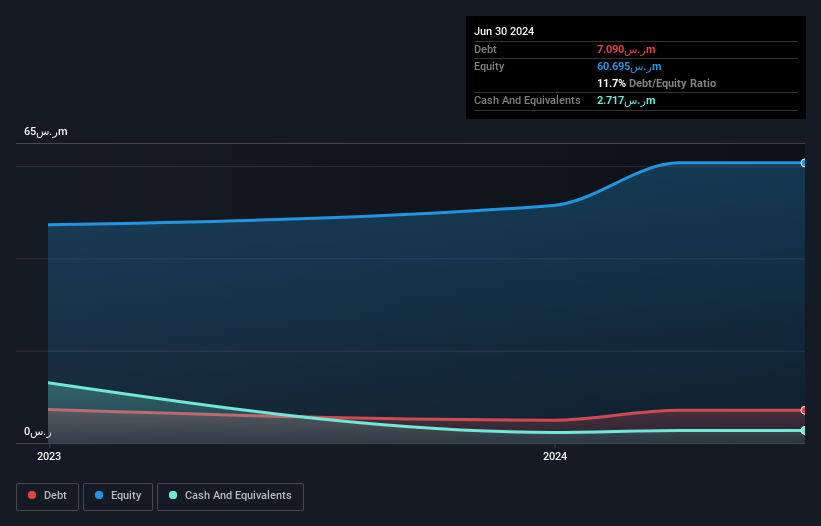

Twareat Medical Care (SASE:9627)

Simply Wall St Value Rating: ★★★★★☆

Overview: Twareat Medical Care Company offers medical care services in remote and industrial areas within the Kingdom of Saudi Arabia and has a market cap of SAR1.08 billion.

Operations: Twareat Medical Care generates revenue primarily through medical care services in remote and industrial areas within Saudi Arabia. The company's net profit margin is 15%, indicating its efficiency in converting revenue into actual profit.

Twareat Medical Care, a small but promising player in the healthcare sector, has shown impressive financial metrics. With earnings growth of 19.7% over the past year, it outpaced the industry average of 13.5%. The company's net debt to equity ratio stands at a satisfactory 7.2%, indicating prudent financial management. Additionally, Twareat's interest payments are well covered by EBIT at a multiple of 43.5x, showcasing strong operational efficiency. Despite its illiquid shares and high level of non-cash earnings, Twareat remains free cash flow positive, suggesting robust underlying business fundamentals that could support future growth initiatives in the sector.

- Dive into the specifics of Twareat Medical Care here with our thorough health report.

Gain insights into Twareat Medical Care's past trends and performance with our Past report.

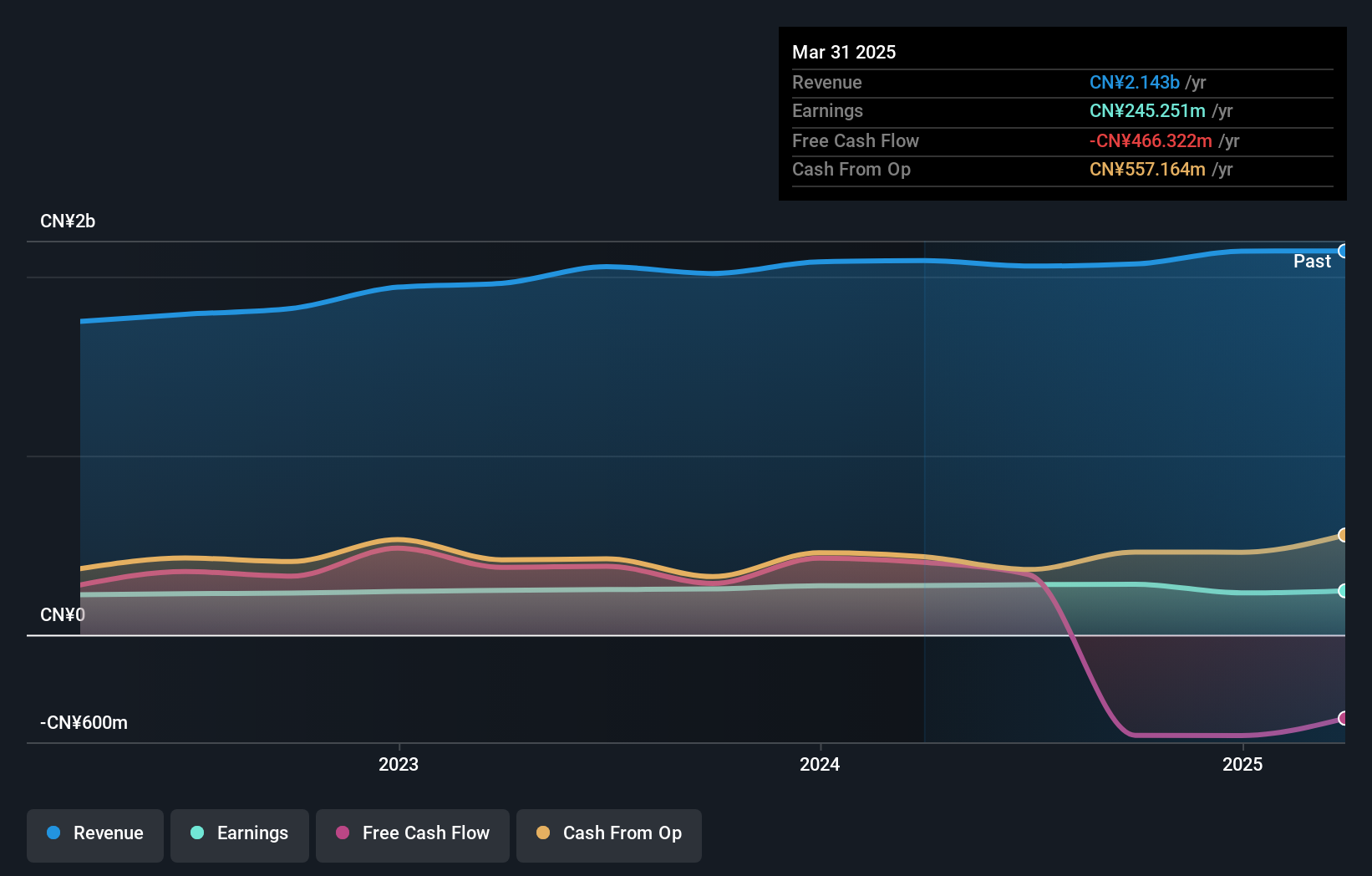

Xinhuanet (SHSE:603888)

Simply Wall St Value Rating: ★★★★★★

Overview: Xinhuanet Co., Ltd. operates a news information service portal in China with a market cap of CN¥12.68 billion.

Operations: Xinhuanet generates revenue primarily from its news information service portal in China. The company's net profit margin has shown notable fluctuations, reflecting changes in operational efficiency and cost management strategies.

Xinhuanet, a smaller player in the media landscape, presents an intriguing profile with its debt-free status over the last five years. This financial freedom is complemented by a Price-To-Earnings ratio of 44.9x, notably below the industry average of 51.4x, hinting at potential undervaluation. The company's earnings growth rate of 10% outpaced the industry's negative trend of -10%, showcasing resilience and adaptability. Despite not being free cash flow positive recently, Xinhuanet's high level of non-cash earnings suggests robust underlying business operations that could support future expansion or strategic initiatives.

- Take a closer look at Xinhuanet's potential here in our health report.

Explore historical data to track Xinhuanet's performance over time in our Past section.

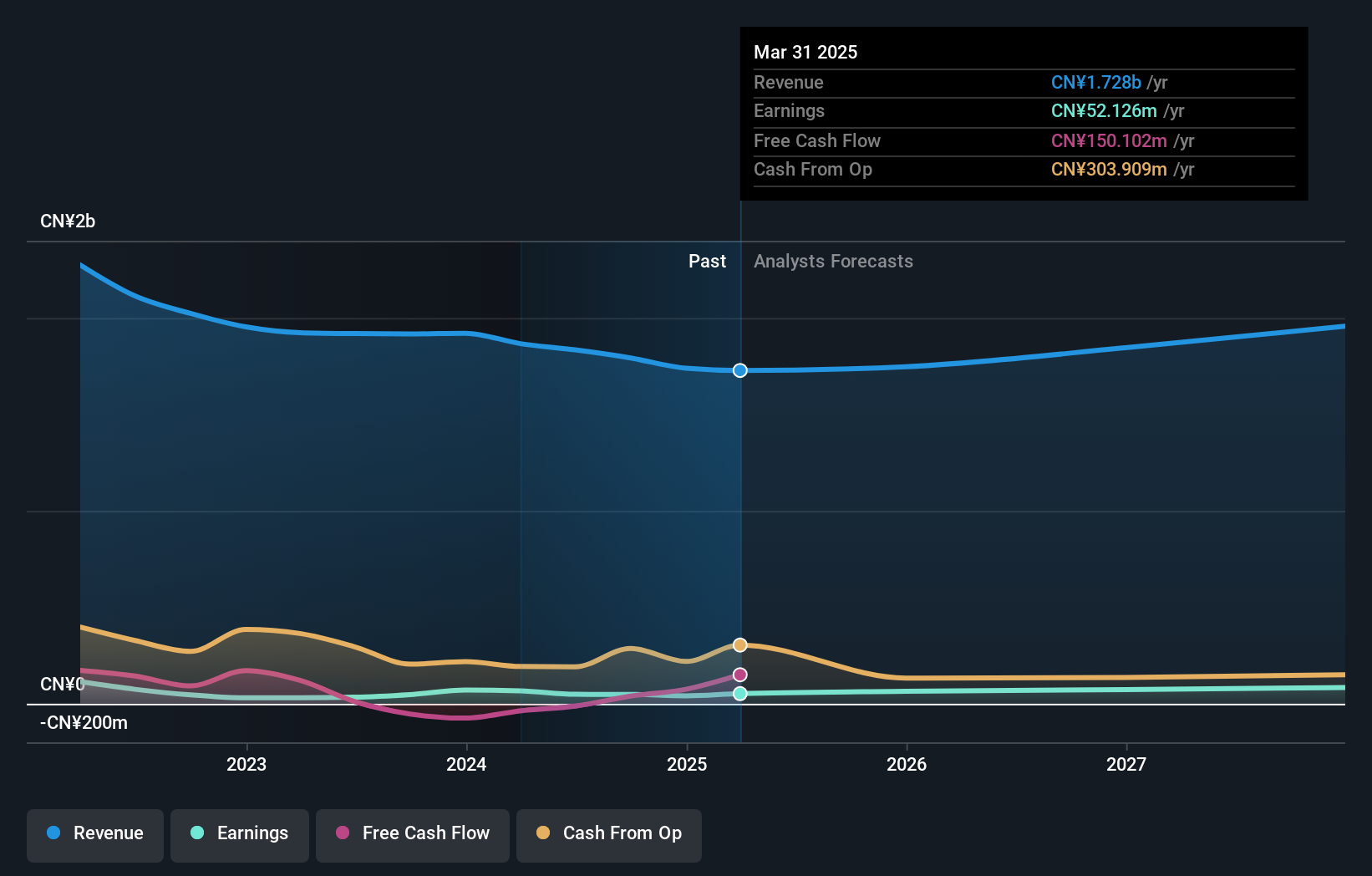

Jiangxi Huangshanghuang Group Food (SZSE:002695)

Simply Wall St Value Rating: ★★★★★★

Overview: Jiangxi Huangshanghuang Group Food Co., Ltd. develops, produces, and sells braised meat products in China with a market cap of CN¥5.19 billion.

Operations: The company generates revenue primarily from the sale of braised meat products. It focuses on cost management to optimize its net profit margin, which has shown fluctuations over recent periods.

Earnings for Jiangxi Huangshanghuang Group Food grew by 2.2% over the past year, outperforming the food industry's -6.3%. Despite this, earnings have seen a significant annual decline of 37.6% over five years. The company is debt-free now, a marked improvement from a debt-to-equity ratio of 4.4% five years ago, eliminating concerns about interest coverage. A notable CN¥24.8M one-off gain has skewed recent financial results, adding complexity to the earnings quality assessment. The stock's price has been highly volatile recently and was removed from the S&P Global BMI Index in December 2024, potentially affecting investor perception and market visibility.

Where To Now?

- Unlock more gems! Our Undiscovered Gems With Strong Fundamentals screener has unearthed 4701 more companies for you to explore.Click here to unveil our expertly curated list of 4704 Undiscovered Gems With Strong Fundamentals.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Twareat Medical Care might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SASE:9627

Twareat Medical Care

Provides medical care services in remote and industrial areas in the Kingdom of Saudi Arabia.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.5% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|30.7% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor