Advertisement

- China

- /

- Energy Services

- /

- SZSE:002629

What Zhejiang Renzhi Co., Ltd.'s (SZSE:002629) 45% Share Price Gain Is Not Telling You

Zhejiang Renzhi Co., Ltd. (SZSE:002629) shares have continued their recent momentum with a 45% gain in the last month alone. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 45% over that time.

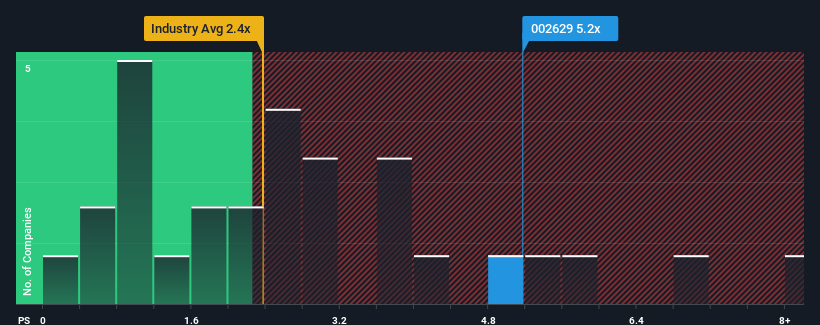

Following the firm bounce in price, you could be forgiven for thinking Zhejiang Renzhi is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 5.2x, considering almost half the companies in China's Energy Services industry have P/S ratios below 2.4x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

View our latest analysis for Zhejiang Renzhi

What Does Zhejiang Renzhi's Recent Performance Look Like?

Zhejiang Renzhi has been doing a decent job lately as it's been growing revenue at a reasonable pace. Perhaps the market believes the recent revenue performance is strong enough to outperform the industry, which has inflated the P/S ratio. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Zhejiang Renzhi will help you shine a light on its historical performance.Is There Enough Revenue Growth Forecasted For Zhejiang Renzhi?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Zhejiang Renzhi's to be considered reasonable.

If we review the last year of revenue growth, the company posted a worthy increase of 3.3%. Pleasingly, revenue has also lifted 50% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenues over that time.

This is in contrast to the rest of the industry, which is expected to grow by 21% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this information, we find it concerning that Zhejiang Renzhi is trading at a P/S higher than the industry. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

What We Can Learn From Zhejiang Renzhi's P/S?

The strong share price surge has lead to Zhejiang Renzhi's P/S soaring as well. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

The fact that Zhejiang Renzhi currently trades on a higher P/S relative to the industry is an oddity, since its recent three-year growth is lower than the wider industry forecast. When we see slower than industry revenue growth but an elevated P/S, there's considerable risk of the share price declining, sending the P/S lower. Unless there is a significant improvement in the company's medium-term performance, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

It is also worth noting that we have found 3 warning signs for Zhejiang Renzhi (1 can't be ignored!) that you need to take into consideration.

If these risks are making you reconsider your opinion on Zhejiang Renzhi, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Renzhi might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002629

Zhejiang Renzhi

Provides professional services in the oil and gas drilling and engineering fields in China.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.1% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor