Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688591

Undiscovered Gems in Global Markets for December 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape of dovish Federal Reserve signals and fluctuating economic indicators, small-cap stocks have emerged as notable performers, with the Russell 2000 Index advancing significantly. In this environment of shifting consumer confidence and moderated inflation expectations, identifying undiscovered gems in the stock market involves looking for companies that exhibit resilience and potential for growth amidst broader economic trends.

Top 10 Undiscovered Gems With Strong Fundamentals Globally

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Lion Rock Group | 5.00% | 14.21% | 13.26% | ★★★★★★ |

| Mendelson Infrastructures & Industries | 17.65% | 4.48% | 4.46% | ★★★★★★ |

| Baazeem Trading | 10.02% | -1.27% | -1.66% | ★★★★★★ |

| Zhejiang Yayi Metal TechnologyLtd | NA | -8.40% | -44.63% | ★★★★★★ |

| Y.D. More Investments | 50.84% | 28.28% | 35.02% | ★★★★★☆ |

| YuanShengTai Dairy Farm | 15.09% | 11.64% | -31.87% | ★★★★★☆ |

| JB Foods | 113.93% | 31.03% | 41.46% | ★★★★☆☆ |

| Banyan Tree Holdings | 42.74% | 15.33% | 72.59% | ★★★★☆☆ |

| Tibet TourismLtd | 21.50% | 10.05% | 27.69% | ★★★★☆☆ |

| Mirai Semiconductors | 46.15% | 10.52% | 56.25% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

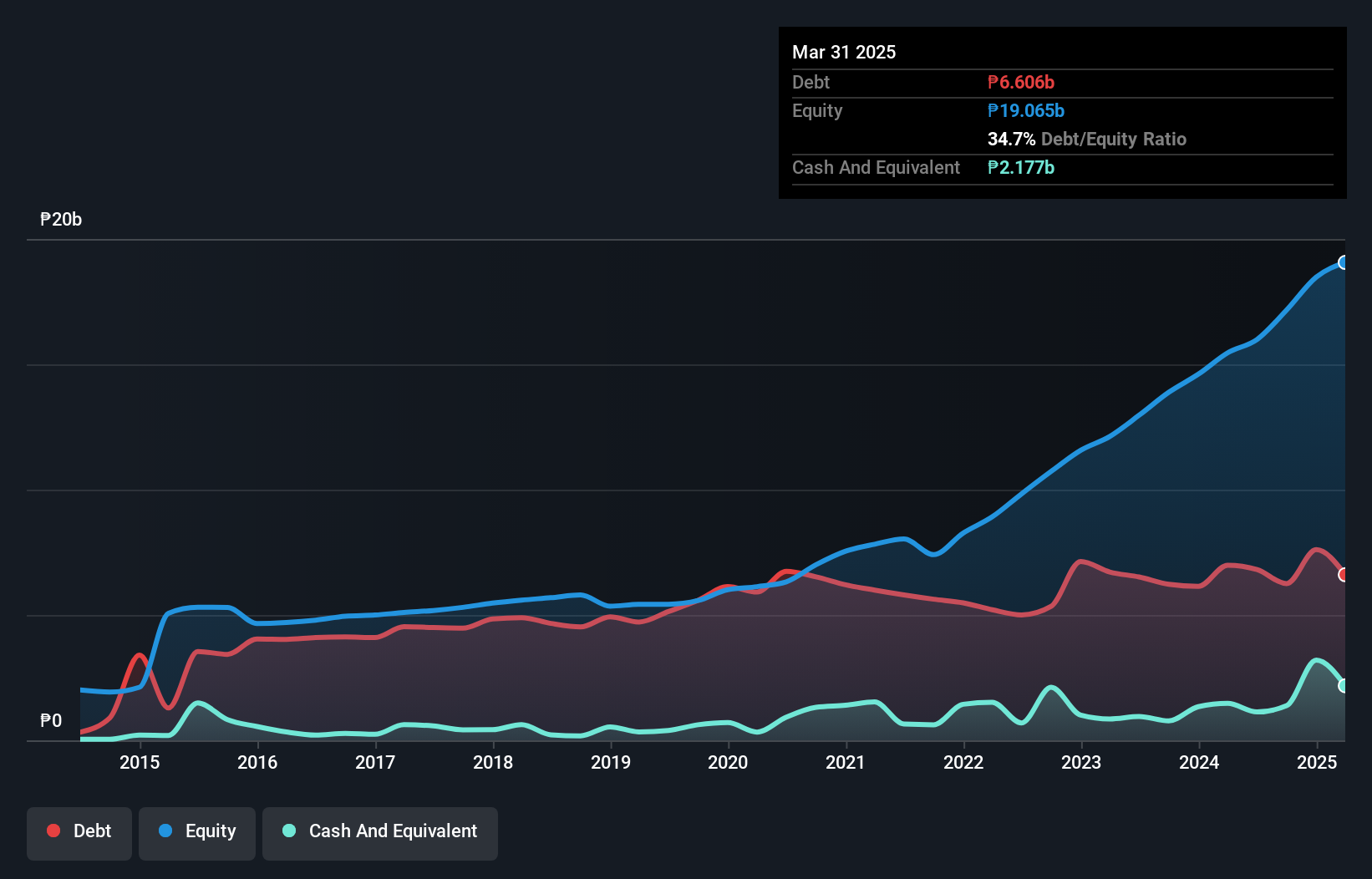

Apex Mining (PSE:APX)

Simply Wall St Value Rating: ★★★★★☆

Overview: Apex Mining Co., Inc. is involved in the exploration and production of metals and minerals in the Philippines, with a market capitalization of ₱60.70 billion.

Operations: Apex Mining generates revenue primarily from the sale of metals and minerals extracted in the Philippines. The company's cost structure is significantly influenced by exploration, extraction, and production expenses. Net profit margin trends provide insight into profitability dynamics over time.

Apex Mining, a promising player in the mining sector, has seen its debt to equity ratio drop significantly from 106.7% to 30.2% over five years, indicating better financial health. Despite a volatile share price recently, the company boasts high-quality earnings and maintains a net debt to equity ratio of 24%, which is satisfactory by industry standards. Earnings have grown at an impressive rate of 33.3% annually over the past five years and are expected to continue growing at 25.15%. However, recent operational halts due to natural events may impact short-term performance until full operations resume upon clearance from authorities.

- Dive into the specifics of Apex Mining here with our thorough health report.

Gain insights into Apex Mining's historical performance by reviewing our past performance report.

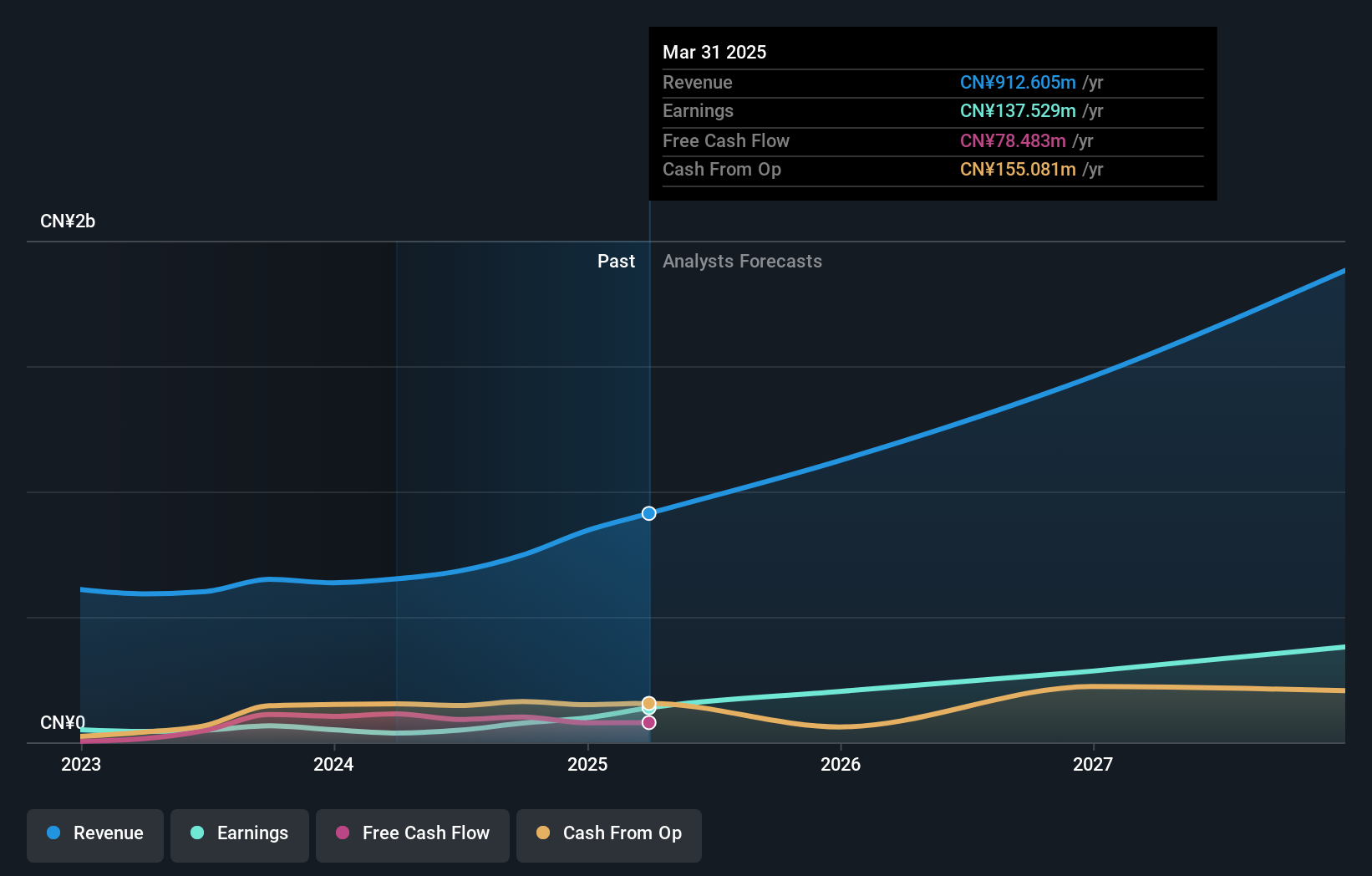

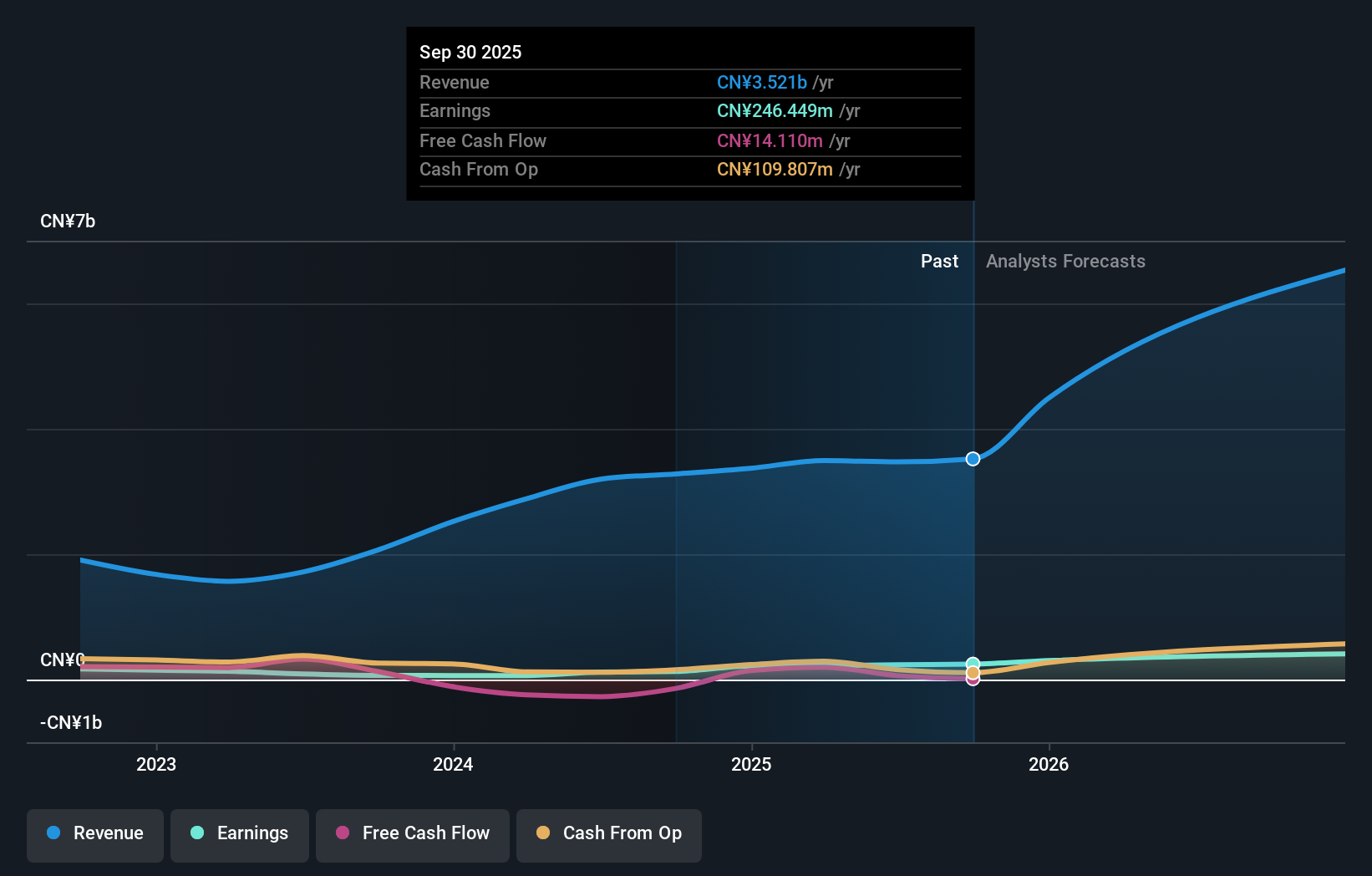

Telink Semiconductor(Shanghai)Co.Ltd (SHSE:688591)

Simply Wall St Value Rating: ★★★★★★

Overview: Telink Semiconductor (Shanghai) Co., Ltd. focuses on the research, development, design, and sales of low-power wireless IoT chips, with a market capitalization of CN¥10.47 billion.

Operations: Telink Semiconductor generates revenue primarily from the sale of semiconductors, amounting to CN¥1.02 billion.

Telink Semiconductor, a nimble player in the semiconductor space, has been making waves with its impressive earnings growth of 126% over the past year, significantly outpacing the industry average of 11.4%. With no debt on its books and a P/E ratio of 62.8x—below the industry average—Telink presents an intriguing value proposition. Recent financials show net income at CNY 139.69 million for nine months ending September 2025, up from CNY 64.27 million previously, reflecting robust performance despite share price volatility in recent months. The company is poised for future growth with forecasted earnings expansion at a rate of 35.41% annually.

- Navigate through the intricacies of Telink Semiconductor(Shanghai)Co.Ltd with our comprehensive health report here.

Understand Telink Semiconductor(Shanghai)Co.Ltd's track record by examining our Past report.

Jiangsu Tongrun Equipment TechnologyLtd (SZSE:002150)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Jiangsu Tongrun Equipment Technology Co., Ltd focuses on the research, development, production, and sales of photovoltaic energy storage equipment, components, and metal products in China with a market capitalization of CN¥7.65 billion.

Operations: The company generates revenue primarily through the sale of photovoltaic energy storage equipment, components, and metal products. Its financial performance is reflected in a market capitalization of CN¥7.65 billion.

Jiangsu Tongrun Equipment Technology has been making waves with its impressive earnings growth of 90.9% over the past year, far outpacing the Consumer Durables industry, which saw a -3.4% change. The company reported sales of CN¥2.59 billion for the nine months ending September 2025, up from CN¥2.44 billion a year earlier, while net income rose to CN¥136.72 million from CN¥107.43 million in the same period last year. With a price-to-earnings ratio of 31.9x below China's market average and interest payments well covered by EBIT at 13.8x, it seems poised for continued performance despite recent share price volatility and significant one-off gains impacting results.

Next Steps

- Unlock more gems! Our Global Undiscovered Gems With Strong Fundamentals screener has unearthed 3017 more companies for you to explore.Click here to unveil our expertly curated list of 3020 Global Undiscovered Gems With Strong Fundamentals.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Telink Semiconductor(Shanghai)Co.Ltd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688591

Telink Semiconductor(Shanghai)Co.Ltd

Engages in research, development, design, and sales of low-power wireless IoT chips.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$28.1829.5% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on Fiverr International ·

Fiverr International will transform the freelance industry with AI-powered growth

Fair Value:US$36.8143.1% undervalued

78 followersusers have followed this narrative

7 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

108 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

936 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

144 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative