Advertisement

Risks Still Elevated At These Prices As Hubei Mailyard Share Co.,Ltd (SHSE:600107) Shares Dive 28%

Hubei Mailyard Share Co.,Ltd (SHSE:600107) shareholders that were waiting for something to happen have been dealt a blow with a 28% share price drop in the last month. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 39% in that time.

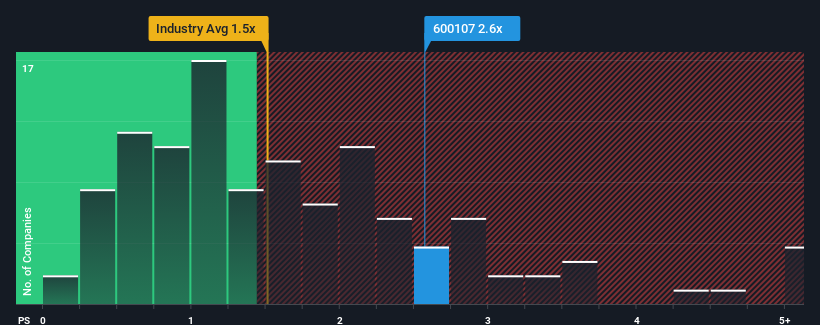

Even after such a large drop in price, when almost half of the companies in China's Luxury industry have price-to-sales ratios (or "P/S") below 1.5x, you may still consider Hubei Mailyard ShareLtd as a stock probably not worth researching with its 2.6x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

Check out our latest analysis for Hubei Mailyard ShareLtd

What Does Hubei Mailyard ShareLtd's P/S Mean For Shareholders?

Revenue has risen firmly for Hubei Mailyard ShareLtd recently, which is pleasing to see. One possibility is that the P/S ratio is high because investors think this respectable revenue growth will be enough to outperform the broader industry in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Hubei Mailyard ShareLtd's earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For Hubei Mailyard ShareLtd?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Hubei Mailyard ShareLtd's to be considered reasonable.

If we review the last year of revenue growth, the company posted a worthy increase of 14%. The solid recent performance means it was also able to grow revenue by 18% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 17% shows it's noticeably less attractive.

With this information, we find it concerning that Hubei Mailyard ShareLtd is trading at a P/S higher than the industry. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

What We Can Learn From Hubei Mailyard ShareLtd's P/S?

There's still some elevation in Hubei Mailyard ShareLtd's P/S, even if the same can't be said for its share price recently. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

The fact that Hubei Mailyard ShareLtd currently trades on a higher P/S relative to the industry is an oddity, since its recent three-year growth is lower than the wider industry forecast. When we observe slower-than-industry revenue growth alongside a high P/S ratio, we assume there to be a significant risk of the share price decreasing, which would result in a lower P/S ratio. If recent medium-term revenue trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

It is also worth noting that we have found 1 warning sign for Hubei Mailyard ShareLtd that you need to take into consideration.

If these risks are making you reconsider your opinion on Hubei Mailyard ShareLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Hubei Mailyard ShareLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600107

Hubei Mailyard ShareLtd

Engages in manufacture, processing, and sale of clothes, apparel, textiles, and accessories in China and internationally.

Flawless balance sheet with very low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor