- China

- /

- Professional Services

- /

- SZSE:301449

Undiscovered Gems In Asia Featuring Three Promising Small Cap Stocks

Reviewed by Simply Wall St

The Asian markets have been navigating a complex landscape, with Japan's recent interest rate hike marking a significant shift in monetary policy and China's economic indicators reflecting mixed signals of growth. Amidst these developments, small-cap stocks present intriguing opportunities for investors seeking to uncover potential amidst market fluctuations. Identifying promising small-cap stocks often involves looking for companies with strong fundamentals, innovative business models, and the ability to adapt to changing market dynamics—all crucial traits in today's evolving economic environment.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Toho | 64.50% | 7.33% | 58.64% | ★★★★★★ |

| Maxigen Biotech | NA | 10.31% | 23.99% | ★★★★★★ |

| Ruentex Interior Design | NA | 26.71% | 37.25% | ★★★★★★ |

| Jinghua Pharmaceutical Group | NA | 2.42% | 18.34% | ★★★★★★ |

| FALCO HOLDINGS | 4.59% | -1.20% | -5.35% | ★★★★★★ |

| Central Forest Group | NA | 5.20% | 24.71% | ★★★★★★ |

| Shangri-La Hotel | NA | 33.29% | 66.13% | ★★★★★★ |

| Unitech Computer | 48.86% | 2.82% | -0.17% | ★★★★★☆ |

| Lucky Cement | 49.27% | 4.40% | 18.92% | ★★★★☆☆ |

| Kaneko Seeds | 13.52% | 1.53% | -1.31% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

Morimatsu International Holdings (SEHK:2155)

Simply Wall St Value Rating: ★★★★★★

Overview: Morimatsu International Holdings Company Limited specializes in the design, manufacture, installation, operation, and maintenance of core equipment and process systems for industries such as chemical reactions and polymerization, with a market cap of HK$11.94 billion.

Operations: Morimatsu International Holdings generates revenue primarily through the sale of comprehensive pressure equipment, amounting to CN¥6.16 billion. The company's financial performance includes a focus on cost management and profitability, with particular attention to its gross profit margin trends over time.

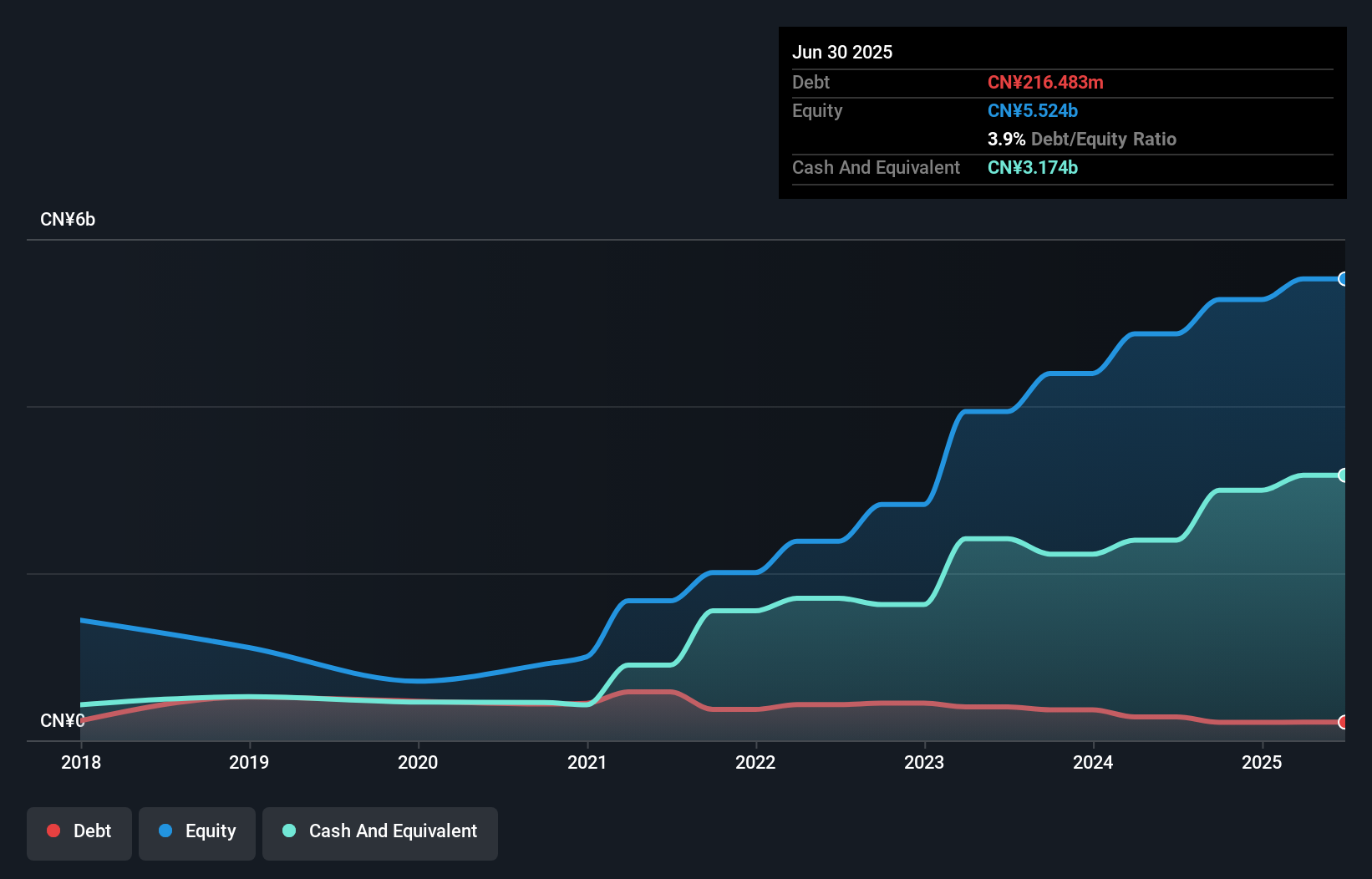

Morimatsu International, a small cap player in the machinery sector, showcases intriguing financial dynamics. The company has high-quality earnings and is trading at 41% below its estimated fair value, suggesting potential undervaluation. Over the past five years, its debt to equity ratio impressively decreased from 52.9% to 3.9%, indicating robust financial management with more cash than total debt. Despite negative earnings growth of -12% last year compared to the industry average of 8%, future prospects seem brighter with forecasted annual earnings growth of over 23%. These factors position Morimatsu as an interesting candidate for further exploration in Asia's market landscape.

- Take a closer look at Morimatsu International Holdings' potential here in our health report.

Understand Morimatsu International Holdings' track record by examining our Past report.

DV8 (SET:DV8)

Simply Wall St Value Rating: ★★★★★★

Overview: DV8 Public Company Limited, along with its subsidiaries, is involved in the production of television satellite programs in Thailand and has a market capitalization of THB9.41 billion.

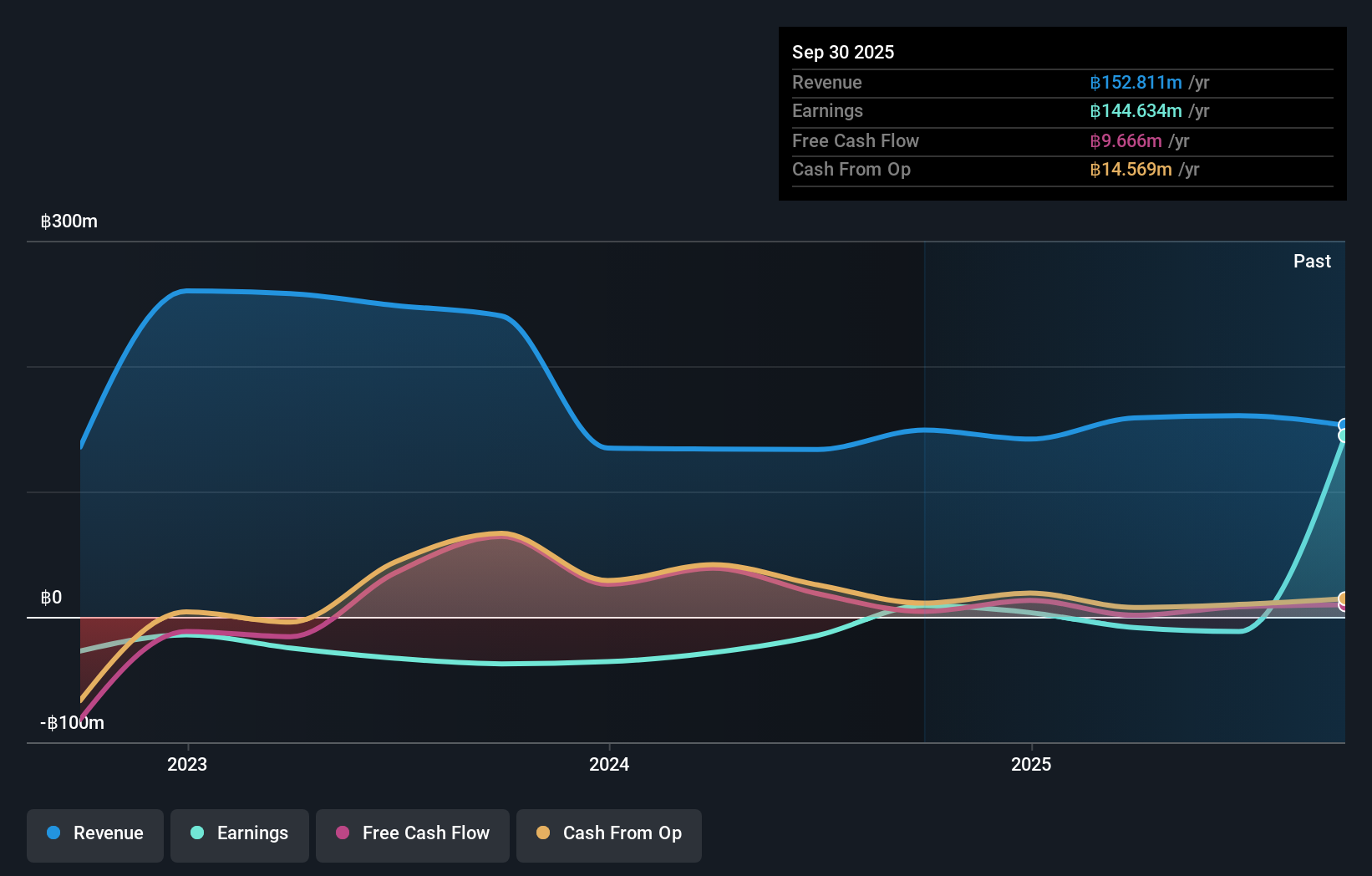

Operations: DV8 generates revenue primarily from its media-advertising segment, amounting to THB152.81 million. The company's financial performance is highlighted by a market capitalization of THB9.41 billion.

DV8, a nimble player in the entertainment sector, has seen its earnings skyrocket by 1514% over the past year, outpacing industry growth of 4.8%. Despite its volatile share price recently, DV8 remains debt-free with no debt compared to five years ago when it had a debt-to-equity ratio of 4.8%. The company reported a net income of THB167M for Q3 2025, significantly up from THB11M last year. However, revenue dipped to THB36M from THB44M in the same period. Recent leadership changes and potential OTCQB listing indicate strategic shifts underway at DV8.

- Click to explore a detailed breakdown of our findings in DV8's health report.

Review our historical performance report to gain insights into DV8's's past performance.

Shenzhen Tiansu Calibration and Testing (SZSE:301449)

Simply Wall St Value Rating: ★★★★★★

Overview: Shenzhen Tiansu Calibration and Testing Co., Ltd. specializes in providing calibration, testing, and certification services with a market capitalization of approximately CN¥1.80 billion.

Operations: The primary revenue stream for Shenzhen Tiansu Calibration and Testing comes from its metrology calibration services, generating CN¥730.04 million, followed by testing services at CN¥138.72 million. Certification services contribute an additional CN¥1.25 million to the company's revenue.

Shenzhen Tiansu has shown promising growth with earnings up by 11.2% over the past year, outpacing its industry peers. The company is debt-free, which eliminates concerns about interest payments and enhances its financial stability. Recent developments include a successful IPO raising CNY 600 million through common stock offerings at CNY 36.8 per share, indicating investor confidence. For the nine months ending September 2025, sales reached CNY 647.9 million with net income of CNY 92.99 million, reflecting solid performance compared to last year's figures of CNY 577.84 million in sales and CNY 83.31 million in net income.

Taking Advantage

- Click here to access our complete index of 2497 Asian Undiscovered Gems With Strong Fundamentals.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:301449

Shenzhen Tiansu Calibration and Testing

Shenzhen Tiansu Calibration and Testing Co., Ltd.

Flawless balance sheet with acceptable track record.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion