Advertisement

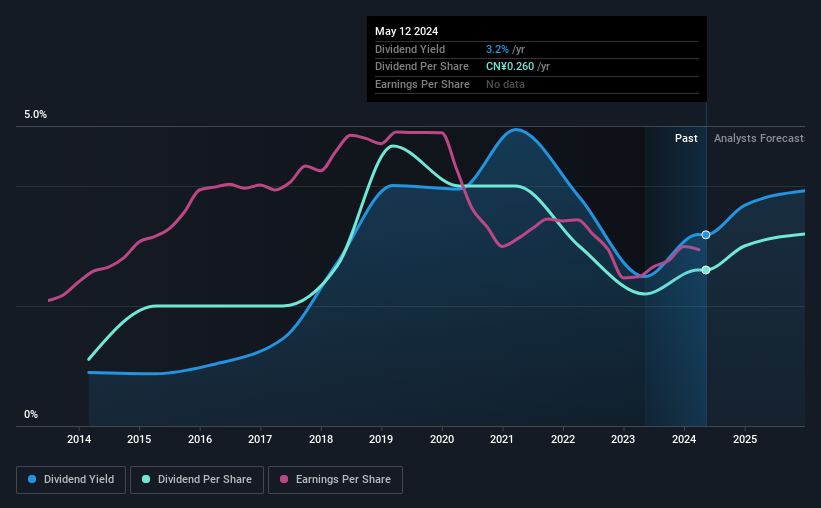

Tungkong Inc.'s (SZSE:002117) dividend will be increasing from last year's payment of the same period to CN¥0.26 on 16th of May. This will take the dividend yield to an attractive 3.2%, providing a nice boost to shareholder returns.

Check out our latest analysis for Tungkong

Tungkong's Dividend Is Well Covered By Earnings

A big dividend yield for a few years doesn't mean much if it can't be sustained. Prior to this announcement, Tungkong's dividend made up quite a large proportion of earnings but only 60% of free cash flows. This leaves plenty of cash for reinvestment into the business.

EPS is set to grow by 12.8% over the next year. If the dividend continues along recent trends, we estimate the payout ratio could reach 82%, which is on the higher side, but certainly still feasible.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. The dividend has gone from an annual total of CN¥0.111 in 2014 to the most recent total annual payment of CN¥0.26. This means that it has been growing its distributions at 8.9% per annum over that time. It's good to see the dividend growing at a decent rate, but the dividend has been cut at least once in the past. Tungkong might have put its house in order since then, but we remain cautious.

Dividend Growth May Be Hard To Come By

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Tungkong has seen earnings per share falling at 9.2% per year over the last five years. If earnings continue declining, the company may have to make the difficult choice of reducing the dividend or even stopping it completely - the opposite of dividend growth. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

Our Thoughts On Tungkong's Dividend

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. We would be a touch cautious of relying on this stock primarily for the dividend income.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. As an example, we've identified 1 warning sign for Tungkong that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Tungkong might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002117

Tungkong

Engages in the printing, lamination, and technical service businesses in the People's Republic of China.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor