Advertisement

- China

- /

- Commercial Services

- /

- SHSE:600292

Is Spic Yuanda Environmental-ProtectionLtd (SHSE:600292) Using Too Much Debt?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Spic Yuanda Environmental-Protection Co.,Ltd. (SHSE:600292) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Spic Yuanda Environmental-ProtectionLtd

What Is Spic Yuanda Environmental-ProtectionLtd's Debt?

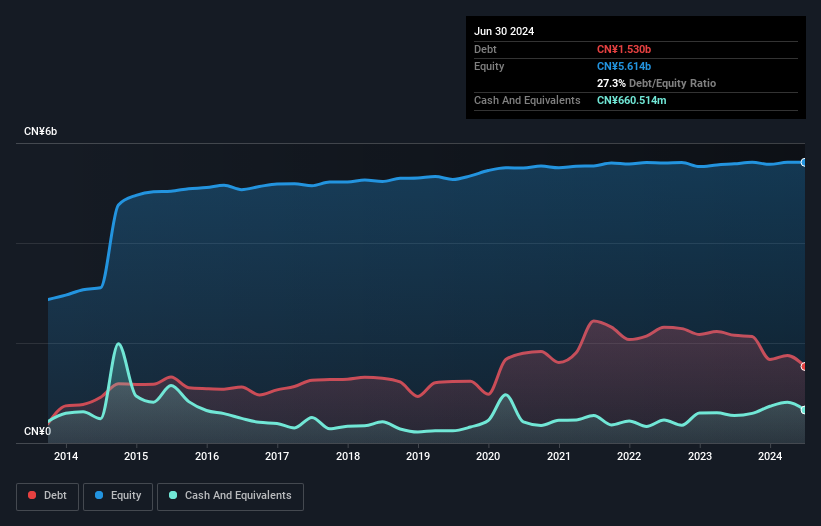

The image below, which you can click on for greater detail, shows that Spic Yuanda Environmental-ProtectionLtd had debt of CN¥1.53b at the end of June 2024, a reduction from CN¥2.15b over a year. However, it does have CN¥660.5m in cash offsetting this, leading to net debt of about CN¥869.9m.

How Strong Is Spic Yuanda Environmental-ProtectionLtd's Balance Sheet?

According to the last reported balance sheet, Spic Yuanda Environmental-ProtectionLtd had liabilities of CN¥2.82b due within 12 months, and liabilities of CN¥1.01b due beyond 12 months. Offsetting this, it had CN¥660.5m in cash and CN¥2.71b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥468.6m.

Of course, Spic Yuanda Environmental-ProtectionLtd has a market capitalization of CN¥4.08b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Spic Yuanda Environmental-ProtectionLtd's net debt to EBITDA ratio of about 1.6 suggests only moderate use of debt. And its strong interest cover of 14.4 times, makes us even more comfortable. In addition to that, we're happy to report that Spic Yuanda Environmental-ProtectionLtd has boosted its EBIT by 39%, thus reducing the spectre of future debt repayments. When analysing debt levels, the balance sheet is the obvious place to start. But it is Spic Yuanda Environmental-ProtectionLtd's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Happily for any shareholders, Spic Yuanda Environmental-ProtectionLtd actually produced more free cash flow than EBIT over the last three years. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

The good news is that Spic Yuanda Environmental-ProtectionLtd's demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And that's just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. Considering this range of factors, it seems to us that Spic Yuanda Environmental-ProtectionLtd is quite prudent with its debt, and the risks seem well managed. So the balance sheet looks pretty healthy, to us. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example - Spic Yuanda Environmental-ProtectionLtd has 1 warning sign we think you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600292

Spic Yuanda Environmental-ProtectionLtd

Spic Yuanda Environmental-Protection Co.,Ltd.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|29.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor