Advertisement

Can Mixed Fundamentals Have A Negative Impact on Zhejiang Taifu Pump Co., Ltd (SZSE:300992) Current Share Price Momentum?

Zhejiang Taifu Pump (SZSE:300992) has had a great run on the share market with its stock up by a significant 60% over the last three months. But the company's key financial indicators appear to be differing across the board and that makes us question whether or not the company's current share price momentum can be maintained. Particularly, we will be paying attention to Zhejiang Taifu Pump's ROE today.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

View our latest analysis for Zhejiang Taifu Pump

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Zhejiang Taifu Pump is:

4.4% = CN¥35m ÷ CN¥791m (Based on the trailing twelve months to September 2024).

The 'return' is the profit over the last twelve months. One way to conceptualize this is that for each CN¥1 of shareholders' capital it has, the company made CN¥0.04 in profit.

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Zhejiang Taifu Pump's Earnings Growth And 4.4% ROE

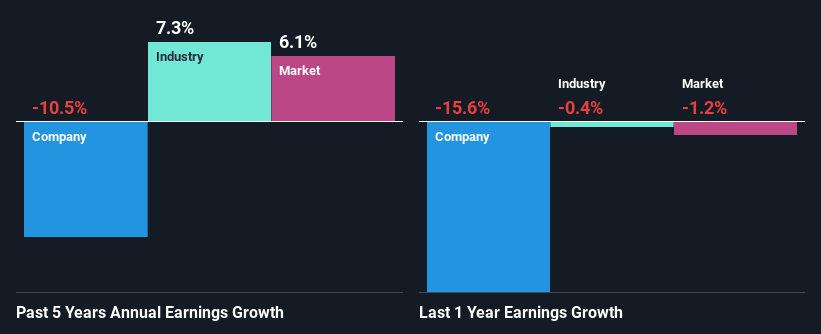

It is hard to argue that Zhejiang Taifu Pump's ROE is much good in and of itself. Not just that, even compared to the industry average of 6.3%, the company's ROE is entirely unremarkable. For this reason, Zhejiang Taifu Pump's five year net income decline of 10% is not surprising given its lower ROE. We believe that there also might be other aspects that are negatively influencing the company's earnings prospects. Such as - low earnings retention or poor allocation of capital.

However, when we compared Zhejiang Taifu Pump's growth with the industry we found that while the company's earnings have been shrinking, the industry has seen an earnings growth of 7.3% in the same period. This is quite worrisome.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is Zhejiang Taifu Pump fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Zhejiang Taifu Pump Making Efficient Use Of Its Profits?

Zhejiang Taifu Pump's low three-year median payout ratio of 11% (implying that it retains the remaining 89% of its profits) comes as a surprise when you pair it with the shrinking earnings. The low payout should mean that the company is retaining most of its earnings and consequently, should see some growth. It looks like there might be some other reasons to explain the lack in that respect. For example, the business could be in decline.

Moreover, Zhejiang Taifu Pump has been paying dividends for three years, which is a considerable amount of time, suggesting that management must have perceived that the shareholders prefer consistent dividends even though earnings have been shrinking.

Summary

Overall, we have mixed feelings about Zhejiang Taifu Pump. While the company does have a high rate of profit retention, its low rate of return is probably hampering its earnings growth. Wrapping up, we would proceed with caution with this company and one way of doing that would be to look at the risk profile of the business. To know the 2 risks we have identified for Zhejiang Taifu Pump visit our risks dashboard for free.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Taifu Pump might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300992

Zhejiang Taifu Pump

Engages in the research and development, production, and sales of various pumps in China and internationally.

Mediocre balance sheet low.

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|59.6% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|20.8% undervalued

ZW

Community Contributor