Advertisement

- China

- /

- Electronic Equipment and Components

- /

- SHSE:688205

Spotlight On Asian Growth Stocks With Up To 26% Insider Ownership

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a complex landscape of trade tensions and economic indicators, Asian equities have been capturing attention with their potential for growth amid fluctuating conditions. In this environment, companies with significant insider ownership often stand out as they may reflect confidence in the firm's long-term prospects.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Leapmotor Technology (SEHK:9863) | 15.6% | 59.9% |

| Vuno (KOSDAQ:A338220) | 15.6% | 109.8% |

| Shanghai Huace Navigation Technology (SZSE:300627) | 24.4% | 23.5% |

| Schooinc (TSE:264A) | 30.6% | 68.9% |

| Samyang Foods (KOSE:A003230) | 11.7% | 24.3% |

| NEXTIN (KOSDAQ:A348210) | 12.4% | 33.8% |

| Nanya New Material TechnologyLtd (SHSE:688519) | 11% | 63.3% |

| M31 Technology (TPEX:6643) | 30.8% | 63.4% |

| Laopu Gold (SEHK:6181) | 35.5% | 40.2% |

| Fulin Precision (SZSE:300432) | 13.6% | 43% |

Here we highlight a subset of our preferred stocks from the screener.

Xinyi Solar Holdings (SEHK:968)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Xinyi Solar Holdings Limited is an investment holding company that produces, sells, and trades solar glass products across Mainland China, the rest of Asia, North America, Europe, and other international markets with a market cap of HK$22.79 billion.

Operations: The company's revenue is primarily generated from the sales of solar glass, amounting to CN¥18.82 billion, and its solar farm business, including EPC services, which contributes CN¥3.02 billion.

Insider Ownership: 26.8%

Xinyi Solar Holdings demonstrates strong growth potential, with earnings projected to increase significantly at 32.3% annually, surpassing the Hong Kong market average. Despite a recent decline in profit margins from 15.9% to 4.6%, insider confidence remains high with substantial insider buying and no significant selling over the past three months. The company trades at a good value relative to peers and is currently priced below its estimated fair value, enhancing its appeal as a growth-focused investment.

- Get an in-depth perspective on Xinyi Solar Holdings' performance by reading our analyst estimates report here.

- Upon reviewing our latest valuation report, Xinyi Solar Holdings' share price might be too pessimistic.

Wuxi Taclink Optoelectronics Technology (SHSE:688205)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Wuxi Taclink Optoelectronics Technology Co., Ltd. operates in the optoelectronics industry, focusing on developing and manufacturing advanced optical communication devices, with a market cap of approximately CN¥10.10 billion.

Operations: Wuxi Taclink Optoelectronics Technology Co., Ltd. generates revenue through its development and manufacturing of advanced optical communication devices within the optoelectronics industry.

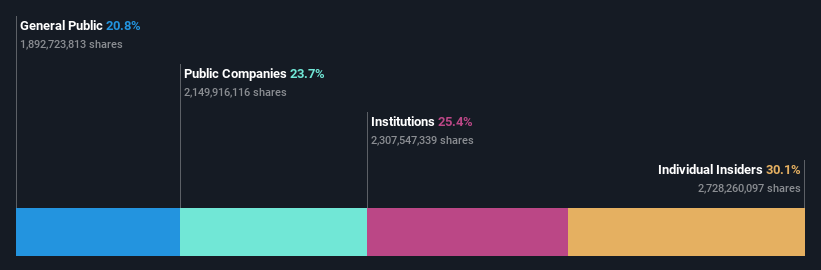

Insider Ownership: 19.8%

Wuxi Taclink Optoelectronics Technology is positioned for robust growth, with revenue expected to increase by 39.1% annually, outpacing the Chinese market. Earnings are forecast to grow significantly at 44.1% per year, although recent quarterly results showed a decline in net income to CNY 14.54 million from CNY 23.01 million year-on-year. Despite high volatility in share price and a modest dividend yield of 0.6%, insider ownership remains substantial without recent trading activity, underscoring potential long-term confidence in its growth trajectory.

- Take a closer look at Wuxi Taclink Optoelectronics Technology's potential here in our earnings growth report.

- Insights from our recent valuation report point to the potential overvaluation of Wuxi Taclink Optoelectronics Technology shares in the market.

Estun Automation (SZSE:002747)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Estun Automation Co., Ltd. is involved in the research, development, production, and sale of intelligent equipment and its control and functional components in China, with a market cap of CN¥17.90 billion.

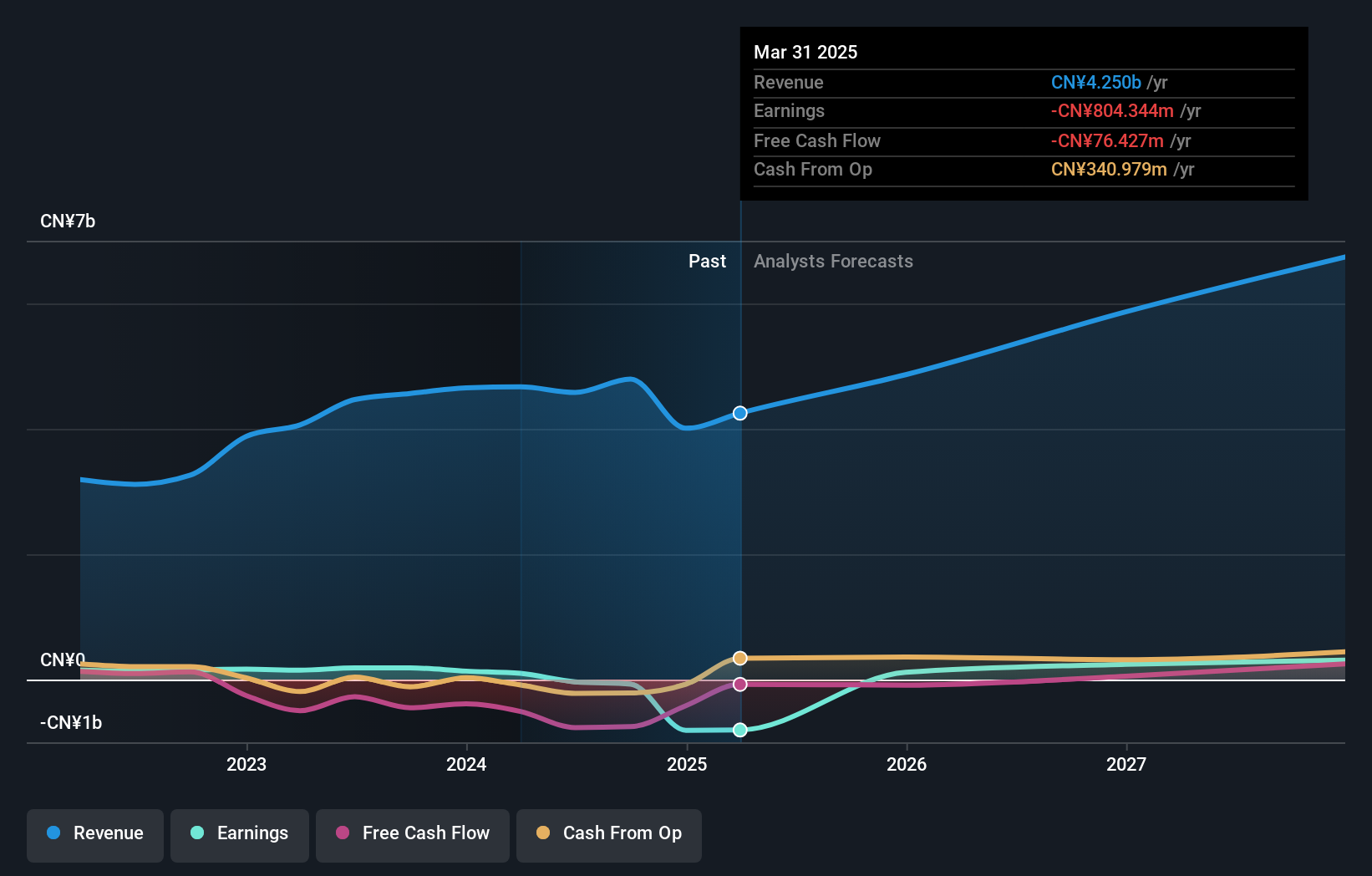

Operations: The company's revenue is primarily derived from its Instrument and Meter Manufacturing segment, which generated CN¥4.25 billion.

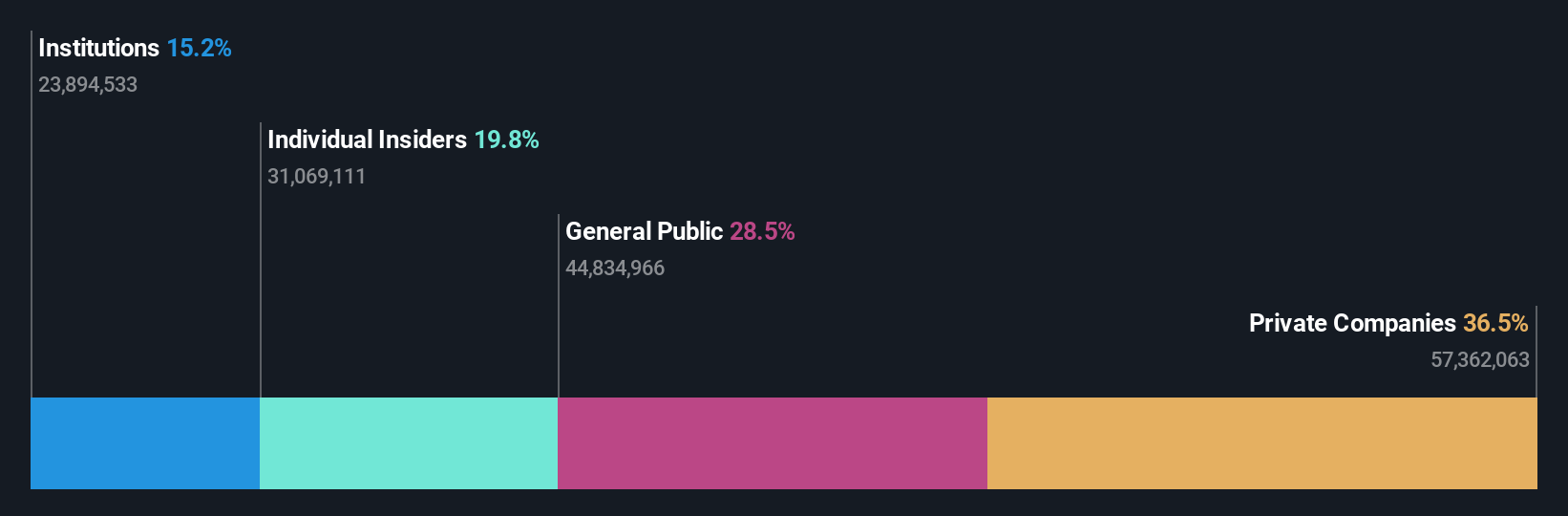

Insider Ownership: 13%

Estun Automation, with significant insider ownership, is poised for growth despite recent challenges. Its Q1 2025 sales rose to CNY 1.24 billion from CNY 1 billion year-on-year, though a net loss of CNY 810.44 million was reported for 2024 due to declining annual sales. The company is expected to achieve profitability within three years, with revenue forecasted to grow at 14.1% annually, surpassing the broader Chinese market's growth rate of 12.4%.

- Dive into the specifics of Estun Automation here with our thorough growth forecast report.

- In light of our recent valuation report, it seems possible that Estun Automation is trading beyond its estimated value.

Where To Now?

- Delve into our full catalog of 615 Fast Growing Asian Companies With High Insider Ownership here.

- Looking For Alternative Opportunities? We've found 16 US stocks that are forecast to pay a dividend yeild of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Wuxi Taclink Optoelectronics Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688205

Wuxi Taclink Optoelectronics Technology

Wuxi Taclink Optoelectronics Technology Co., Ltd.

Flawless balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor